‘It’s Just Dirt’: Anything Goes in Today’s Muni Bond Market

Muni-Bond Buyers Are Desperate. Risky Borrowers Are Cashing In

(Bloomberg) -- Last month, a risky, new deal hit the municipal-bond market. It came from a small borrower in Colorado that was looking to finance the construction of 1,200 luxury homes in the foothills of the Rocky Mountains.

It was an odd time for such a project. Denver’s decade-long housing boom was beginning to show signs of cooling and, moreover, rival developers had already raised record sums to turn vast tracts of land into new communities. “There’s no houses to see,” said Nicholas Foley, a municipal-bond fund manager at Segall Bryant & Hamill in Denver. “It’s just dirt.”

No matter. The buy orders poured in anyways and, in the end, about $20 million worth of bonds had been sold for yields as low as 4.75% on 30-year maturities -- similar to the rates that investors once only reserved for relatively risk-free market behemoths like California or New York.

The Federal Reserve’s decision to lower benchmark borrowing costs is keeping the U.S. awash in cheap credit. That has fueled a surge in corporate borrowing, bankrolled takeovers of debt-laden companies and, increasingly, sparked concern that some of those leveraged loans have become too risky. That angst has also seeped into the $3.8 trillion market for municipal bonds, a corner of the financial world that traditionally has served as a refuge for individual investors seeking steady, low-risk returns.

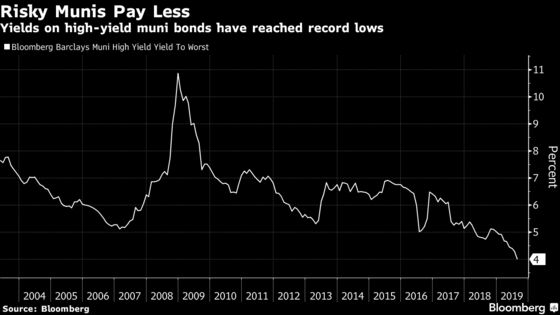

With the steep drop in yields wiping out the tax advantages of some tax-exempt securities, investors are hunting for higher payouts. That’s driven yields on the riskiest tax-exempt securities down to about 4%, the lowest since at least 2003, and in turn spurred an increase in sales from the most default-prone segments of the market. Shopping malls, centers for novel health-care treatments, factories seeking to turn trash into fuel and speculative real-estate developments like the one outside of Denver -- all have recently sold tax-exempt debt through local government agencies.

At the same time, investors are receiving less return for the risk, with the gap between yields on top-rated and junk-grade debt holding near where they stood at the end of 2007.

“There is so much money coming in -- even if 90% of the market rejects it, if 10% wants to buy, they are able to get it done,” said Dan Solender, a partner at Lord, Abbett & Co.

The municipal-debt market remains one of the world’s safest, with only 0.16% of those rated by Moody’s Investors Service defaulting between 2009 and 2018, compared with 6% of corporate bonds. Yet many of the riskiest deals aren’t rated and could leave investors -- including those with stakes in mutual funds -- exposed to potential losses if the economy stalls.

During the 2008 credit crisis set off by the last recession, the municipal junk-bond market was roiled as the slowdown rippled through the economy. More than $8 billion of debt issued through state and local government agencies defaulted that year, the most for any year dating back to 1980, according to Richard Lehmann & Associates. When funds unloaded the riskiest securities, high-yield municipal bonds tumbled, saddling investors with a loss of 27% until the market rebounded in 2009.

The lowest-rated municipal securities have rallied this year, delivering gains of nearly 10%, as plunging yields worldwide leave investors hunting for ways to get higher returns. Mutual funds focused on high-yield tax-exempt debt have pulled in cash every week since early January, with about $384 million added in the week ended Aug. 14, according to Refinitiv’s Lipper US Fund Flows data.

That has increased demand for new issues, driving down the extra yields that the riskiest borrowers pay and allowing some to weaken the protections given to bondholders in the securities contracts.

AMG Vanadium LLC sold $307 million of debt through an Ohio agency to build a factory that will turn waste into a product that’s used in the production of steel. The company, which is responsible for paying on the debt, didn’t give bondholders a mortgage on its property in the event it defaults, as is commonly done. The sale was oversubscribed anyway, allowing the underwriter to price the 30-year securities for a yield of 4.28%. The bonds continued to climb after they were sold.

Investors bought up $1.75 billion in unrated municipal bonds for Virgin Trains USA’s private rail project in Florida. A California factory seeking to create a wood alternative has tapped the market more than once. The new sales-tax-backed debt issued this year by Puerto Rico has gained, pushing the price above full face value, even though the island was rocked by protests that forced the resignation of the governor and has yet to emerge from a record bankruptcy.

“It is a very aggressive market -- but to say that it is frothy means that this is the end of it, and I don’t know,” said Matt Fabian, a partner with Municipal Market Analytics, an independent research firm. “A year from now, we might be yearning for the discipline of 2019.”

Some money managers have started to pull back. Vanguard Group Inc. has cautioned against taking too much risk as the economy’s record-long expansion makes a recession look overdue. Goldman Sachs Group Inc. earlier this year shifted a record amount of its high-yield municipal fund into investment grade debt, anticipating that some of the projects financed by the securities may run into distress.

Through July, about 33 municipal bond issues defaulted, the fastest pace since 2015 and up from 21 during the same period in 2018, according to Fabian’s firm. Such lapses include a California plant that converts medical waste into hot gases, recyclable metals and glass, just years after issuing the unrated debt in 2016 and 2017.

But with the market still delivering outsize gains, mutual funds have a powerful incentive to stay put, given that they’re judged by the performance relative to their peers.

Guy Davidson, chief investment officer of municipal investments at AllianceBernstein, said he’s grappled with the performance of the company’s so-called high-income municipal fund. It’s up 9.7% this year, beating nearly 90% of its peers. “You go, gosh, is it time to take money off the table?” he said.

He hasn’t, anticipating that the high-yield market will be supported by the still-growing U.S. economy. “A bubble implies it’s supposed to pop,” he said. “Fundamentally, it doesn’t feel like there’s things that are going to make it pop.”

Foley, the Denver-based portfolio manager, was once a big buyer of tax-exempt bonds issued to build new housing developments in his booming state, but he has since stopped amid signs that the market has gotten frothy.

Last year, such Colorado land districts sold $1.3 billion in bonds, the most since at least 2005. The securities, which are typically unrated, are repaid by assessments levied on homeowners and offer few protections to investors if the housing market goes south. In the case of the Castle Rock, Colorado development, even if the district skips interest or principal payments, it won’t count as a default, limiting bondholders’ legal power to recoup some of what they’re owed.

Real-estate backed bonds were hit hard by the housing bust over a decade ago, when a wave of them defaulted in Florida. That also happened in California in the 1990s and in Colorado the decade before.

Colorado’s real estate market has boomed over the past decade, leaving Denver’s higher above their pre-recession peak than any other major metropolitan area, according to ATTOM Data Solutions. But there have been some signs that the frenzy is slowing down, as it has elsewhere: in June, only about 12% of homes had competing offers, down from half a year earlier, according to Redfin. And the number of homes on the market rose 28%, according to a local realtors report.

The Castle Rock debt used a limited-tax structure, meaning that failing to levy the property tax pledged to the bonds triggers an event of default.

That security pledge helps ensure that investors eventually get paid on their investments, said Sam Sharp, a managing director at D.A. Davidson & Co., which underwrites the majority of Colorado dirt bonds. The use of surplus funds also provides protections, he added.

“The structuring we do is mindful of how cyclical the real estate market can be,” he said.

Foley said it helps that his firm doesn’t run a high-yield municipal-bond fund and can instead move in and out of securities when they reach “irrational” points.

“If you make a real call against the high-yield market, you’re making a big call that can cost you your job if it doesn’t go right,” Foley said. “The easy thing to do is keep buying more and more high-yield.”

--With assistance from Nic Querolo and Danielle Moran.

To contact the reporter on this story: Amanda Albright in New York at aalbright4@bloomberg.net

To contact the editors responsible for this story: Elizabeth Campbell at ecampbell14@bloomberg.net, William Selway

©2019 Bloomberg L.P.