Mortgage Investors Can Take Heart With Fed Buying ‘Here to Stay’

Mortgage Investors Can Take Heart With Fed Buying ‘Here to Stay’

(Bloomberg) -- Mortgage investors can take heart knowing the Federal Reserve considers agency MBS a primary arena through which to conduct monetary policy.

The central bank has purchased agency mortgage bonds at a record pace totaling $719 billion -- just over $12 billion a day on average -- according to data from the New York Fed. While the amount of buying over such a short time frame has been surprising, the banks re-entry into the MBS market was not.

“The Fed has used its power to stabilize markets and inject confidence,” Kevin Jackson, a managing director on the mortgage trading desk at Wells Fargo & Co., said in an interview. “They drew a line in the sand and said they are going to support the larger part of the housing finance market, which is agency MBS.”

Since the central bank’s first foray into mortgage purchases in late 2008, its opinion that doing so is proper “to support the mortgage and housing markets and to foster improved conditions in financial markets more generally” is little challenged. On a practical level, the highly liquid agency MBS market, with its forward settlement of trades, allows for massive injections of central bank credit more readily than other sectors.

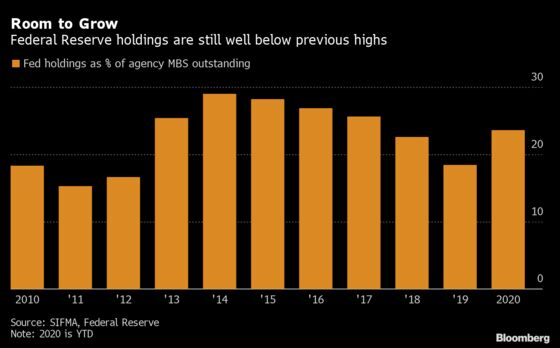

Judging by the Fed’s history, their holdings may grow. The recent buying binge increased the bank’s ownership to about 24% of the market’s total outstanding debt. From 2016 through 2018 that average was about 28%.

“While the current spike is impressive versus last year, going back further puts it in perspective,” said Kirill Krylov, Robert W. Baird & Co. senior portfolio strategist.

Quite the Boost

The tsunami of central bank credit is providing a boost for mortgage bond investors, and has brought about a reversal in the sector’s supply-demand equation. Forecasts saw $490 billion more in supply needing to be absorbed by private investors this year, but after taking into account Fed buying, they may see available supply actually decline by $500 billion, according to JPMorgan Chase & Co.

Buoyed by this good fortune, the Bloomberg Barclays U.S. MBS Index excess return versus Treasuries has rallied 1.73% since QE’s restart on March 16. The UMBS 30-year 2.5% coupon -- the Fed’s main focus and where over 25% of its buying has occurred -- rallied 2.59%.

Lower coupon prices have surged, with the 30-year UMBS 2%, 2.5% and 3% all increasing by at least three points over the same period, according to data compiled by Bloomberg. And as home lending rates are set in the mortgage market the Freddie Mac 30-year mortgage rate dropped to a record low 3.15% on May 28 from a local high of 3.65% on March 19. Lower lending rates have increased concern about that bane of mortgage investors, prepayment speeds.

A key feature of mortgage-backed securities is that the underlying home loans may be prepaid by borrowers at par at any time. With almost the entire MBS universe changing hands at a premium, getting back funds faster than expected can hurt performance. The last three prepayment speed reports have come in above expectations.

“How low can the 30-year mortgage rate go?” said Walt Schmidt, head of mortgage strategies at FHN Financial in Chicago. “That is a concern investors have, as effective yields for MBS in some cases have already gone negative due to higher prices and faster speeds.”

Where’s the Beef?

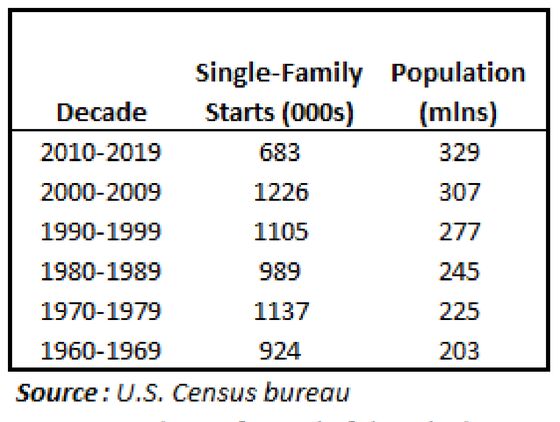

From a historic perspective the Fed’s use of QE “to support the mortgage and housing markets” has been only partly successful. Single-family housing starts during the current era of QE are but a pale shadow of what they once were. Despite an 18% increase in population from 1999 to the end of 2019, single-family housing starts dropped 24% over that span, according to data compiled by Bloomberg News.

In fact, using the average annual single-family home starts seen during each of the last six decades, 2010-2019 saw the lowest level of building since at least the 1950s. It’s little wonder that home prices skyrocketed 49% over the last decade.

As for a return to the pre-QE era when the central bank held nothing but Treasuries, that seems a far-fetched scenario now.

“I do not see the Fed as an outright seller in any reasonable scenario,” Baird’s Krylov said. “The Fed is here to stay.”

- Christopher Maloney is a market strategist and former portfolio manager who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

©2020 Bloomberg L.P.