Mortgage Chaos Threatens to Worsen Once It’s Time for Repayments

Mortgage Chaos Threatens to Worsen Once It’s Time for Repayments

(Bloomberg) -- The mortgage market has been disrupted by millions of borrowers postponing payments because of coronavirus. But lenders and veterans of the 2008 financial crisis warn the real chaos won’t start until the pandemic passes.

The problem is confusion over what will happen when borrowers have to make up those payments. Federal agencies that back most of the market have introduced policies, some of which could require documentation that overwhelms servicers, leading to lengthy wait times and, in extreme cases, foreclosures.

Industry executives say Fannie Mae, Freddie Mac and their regulator are attempting to unveil a program in coming weeks that could alleviate many of the problems. Mortgage lenders say they hope the companies and their watchdog come up with a plan that prevents a repeat of the turmoil that followed the 2008 financial crisis, when confusion and delays hindered borrowers in trying to resume payments.

But unless there are dramatic changes, Americans should “expect even more chaos when forbearance ends,” said Michael Stegman, who served as a senior housing adviser during the Obama administration.

A Fannie spokesman referred a request for comment to the regulator, the Federal Housing Finance Agency. An FHFA spokesman didn’t comment on whether there is a fix in the works. A Freddie spokesman didn’t respond to requests for comment.

The $2.2 trillion stimulus package passed by Congress last month requires mortgage companies to let borrowers delay payments for at least six months if they have been hurt by the pandemic. Because the government wanted to provide help quickly, borrowers merely need to say they face a hardship to receive aid.

Bailout programs during the 2008 crisis did require documentation, and borrowers often struggled to get help as servicers repeatedly lost paperwork and took weeks or even months to approve loan modifications.

Because no documentation is required this time, homeowners won’t face problems initially. But servicers say they’re unsure what will happen when their call centers are flooded in a few months by people ready to resume paying.

Some borrowers have said lenders told them the back payments would be due in a lump sum, which is an option but not a requirement for most people. Housing advocates said they suspect some servicers were knowingly trying to dissuade borrowers from seeking forbearance.

“Borrowers are receiving deceptive information,” said Nikitra Bailey, executive vice president at the Center for Responsible Lending. “The purpose of that information had been designed to scare them.”

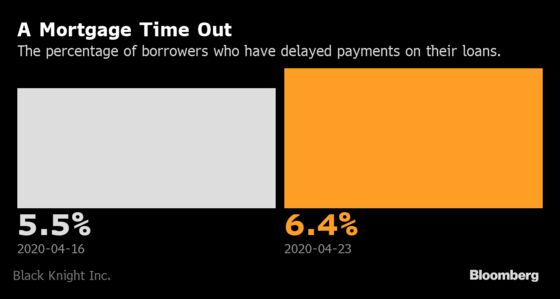

Mortgage information service Black Knight Inc. said last week that 6.4% of borrowers have entered forbearance plans. That included 5.6% of those with loans backed by Fannie and Freddie and 8.9% of loans backed by Ginnie Mae.

Adding to the confusion is the fact that policies for borrowers differ depending on whether their loan is backed by Fannie, Freddie, Ginnie or owned by a private investor.

The Federal Housing Administration, which insures loans backed by Ginnie Mae, has said it will let skipped payments be added to the home as a second lien. That lien won’t need to be paid off until the mortgage is refinanced or the home is sold.

Fannie and Freddie have released an array of more-complicated options. Borrowers can choose to repay the forbearance in as long as 12 months, but if they can’t, they have to apply for a loan modification, which servicers say could trigger delays and documentation issues like those that occurred after the 2008 crisis.

An FHFA spokesman said Fannie and Freddie forbearance repayment options “allow servicers to work with borrowers to find a repayment option that works best for all parties.” He noted an FHFA announcement on Monday that made clear borrowers won’t be forced to repay forbearance in a lump sum.

MBS Prices

A high number of modifications would also put strains on Fannie and Freddie, which typically must buy modified loans out of their mortgage-backed securities. That process can hurt MBS prices, as mortgages are prepaid faster than expected.

Mat Ishbia, chief executive officer of United Wholesale Mortgage, said call volumes to servicers have jumped by 10 times since the coronavirus outbreak. He predicted the crush will be even more intense once borrowers start seeking modifications.

“No one’s ever seen anything like this. Servicers are definitely being strained,” Ishbia said. He said his company has moved some employees to servicing from less-active departments to help manage borrowers.

Mortgage firm Mr. Cooper Group Inc. has increased the staffing in its servicing centers by about 40% from before the pandemic to handle the influx of borrowers requesting forbearance or other help, said Chief Credit Officer Kurt Johnson. Those people would also help borrowers when it’s time to begin repaying, he said.

“We want to make sure that our customers understand that they do have options,” Johnson said.

Getting Current

Bob Broeksmit, chief executive officer of the Mortgage Bankers Association, said Fannie, Freddie and the FHFA are working with lenders to make it easier for borrowers to get current on their loans.

Fannie and Freddie executives have told the MBA that they plan to soon announce a repayment plan similar to the one already offered by the FHA, Broeksmit said. He said the plan, which would essentially let borrowers make up for missed payments when they sell or refinance the home, would ease burdens for borrowers and lighten the processing load for servicers.

Broeksmit said he expects the new option, which could be announced in the next two weeks, to be a top choice for borrowers.

“Hopefully this new option will not be overly complex and can work for a lot of borrowers,” he said.

©2020 Bloomberg L.P.