Morgan Stanley Soared in Currency Derivatives Before Lira Mess

It has more than doubled its activity since 2016 to overtake rivals in bazaar for currency-linked derivatives.

(Bloomberg) -- Morgan Stanley’s drive into a lucrative niche in the foreign-exchange market has hit a major road block.

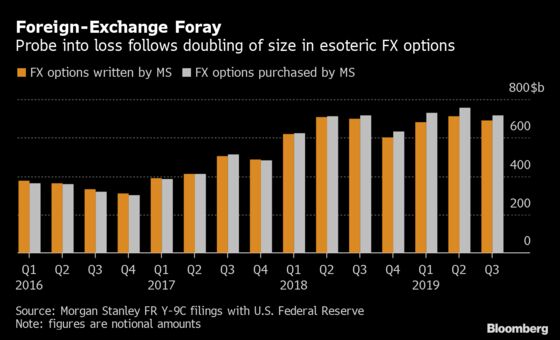

The firm has more than doubled its activity since 2016 to overtake rivals such as Goldman Sachs Group Inc. in the bazaar for currency-linked derivatives known as FX options. Now, Morgan Stanley is probing whether traders improperly valued the esoteric securities, concealing as much as $140 million in losses, Bloomberg reported last week, citing people familiar with the matter.

The world’s biggest stock brokerage adopted a “go big or go home strategy” in the business, said Mark Williams, a finance lecturer at Boston University’s Questrom School of Business. “Doubling their OTC FX option trading book in only three years, given an already sizable market presence, speaks to Morgan Stanley’s aggressive risk appetite.”

While a potential loss would hardly be catastrophic for a broader fixed-income trading business that generated $5 billion in revenue last year, it contrasts with Chief Executive Officer James Gorman’s effort to fashion a steadier, less risky franchise. His approach has allowed Morgan Stanley to close a market-value gap with Goldman Sachs that was more than $50 billion after the financial crisis.

Four years ago, Morgan Stanley’s then-equities chief Ted Pick also took control of the firm’s fixed-income unit with a pledge that it would stop trying to be “all things to all people” and pick spots in the bond and currency markets where it could find adequate returns. The bank had long struggled to compete in the area of interest rates and foreign exchange, known collectively as macro trading, where larger commercial banks benefited from the activity of their corporate clients.

Morgan Stanley tapped Senad Prusac, who had risen up through the FX options unit, to lead global macro trading and find the bank’s niche in that world. Prusac left Morgan Stanley this year and was recently replaced by Jakob Horder, IFRE reported in September. Overseeing the operation was fixed-income head Sam Kellie-Smith, whose LinkedIn profile also cites a background in FX options trading.

The strategy has largely paid off, with Morgan Stanley gaining market share even while it cut headcount and reduced capital dedicated to the fixed-income business. Analysts expect Morgan Stanley to end 2019 with 10% more fixed-income trading revenue than in 2015, while rival Goldman Sachs’s total is set to drop about 20% in the same period.

FX options, a small corner of the $6.6-trillion-per-day currency market, provided some of the growth. In early 2016, Morgan Stanley had fewer of the securities than any other major Wall Street bank, according to a Bloomberg analysis of U.S. Federal Reserve filings. By last year, the firm had eclipsed Goldman Sachs and Bank of America Corp. and trailed only Citigroup Inc. and JPMorgan Chase & Co., the filings show.

FX options can be a flexible and cheap way to speculate on currencies and hedge against losses, according to Beat Nussbaumer, who helped lead foreign-exchange businesses at firms including Commerzbank AG and UniCredit SpA. Daily trading volume has climbed 16% since 2016 to about $294 billion, according to the Bank for International Settlements.

But the instruments can be hard to value and can magnify losses. The trades now in question were tied to the Turkish lira, a currency that whipsawed investors in 2018 and earlier in 2019 amid mounting political tensions, the people said. Those swings roiled a number of firms and Morgan Stanley is grappling with how its losses happened and whether there were efforts to cover them up. At least four traders have been swept up in the probe, including 27-year-old associate Scott Eisner in London, Bloomberg has reported. Morgan Stanley declined to comment on the matter.

Investment banks tailor FX options based on client requests and they’re traded directly between parties, or over-the-counter, rather than through exchanges. While this makes them more opaque, it also makes them more lucrative, according to Nussbaumer.

The biggest investment banks shared about $2.9 billion in revenue from FX options in 2018, a 40% increase from 2017, only to see income fall this year, according to data from Coalition Development Ltd.

Even before the Morgan Stanley episode, sudden moves in currencies have triggered blowups. Citigroup lost more than $150 million in 2015 when the Swiss central bank let the franc trade freely against the euro, Bloomberg reported at the time. In 2016, Taiwanese banks were fined after selling leveraged structured products that bet on a rising Chinese yuan, which saddled clients with losses after the currency plunged.

Morgan Stanley purchased FX option trades with a notional amount of about $718 billion at the end of September, according to the Fed filings. That compares with $512 billion in the same period in 2017 and $320 billion in 2016, the filings show. At the end of the first half of 2019, the firm’s FX options purchased, net of those it sold, was $48 billion, three times that of any other U.S. bank, according to Javier Paz, an analyst with Forex Datasource, an independent consulting firm.

“They’re punching above their weight,” said Paz. “This is the repurposing of their expertise in equity options into currency markets.”

--With assistance from Sridhar Natarajan.

To contact the reporters on this story: Donal Griffin in London at dgriffin10@bloomberg.net;Stefania Spezzati in London at sspezzati@bloomberg.net

To contact the editors responsible for this story: Ambereen Choudhury at achoudhury@bloomberg.net, James Hertling, Michael J. Moore

©2019 Bloomberg L.P.