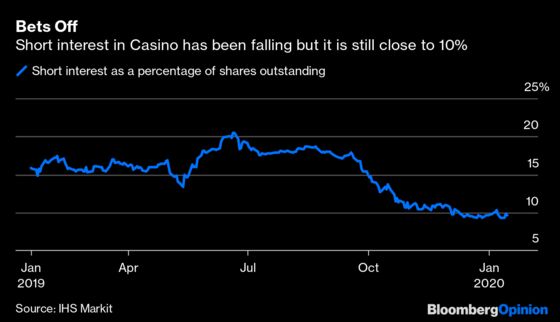

(Bloomberg Opinion) -- French supermarket operator Casino Guichard Perrachon SA has been a favorite plaything for short-selling hedge funds. So for its recovery to take two steps backward is a blow for the group and its chief executive officer, Jean-Charles Naouri.

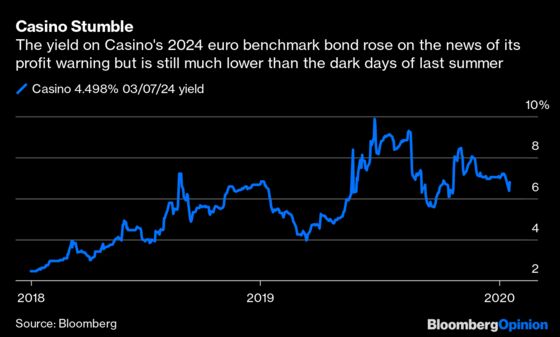

The owner of the Monoprix and Franprix chains looked as if it was gradually getting out of the woods, with Casino making a series of disposals and completing a refinancing, and its parent Rallye SA attempting to work through its 2.9 billion euros ($3.2 billion) of net debt after entering a creditor protection program last year.

But things are never so straight-forward for the two companies, which are inextricably tied. (Rallye is Naouri’s investment vehicle.) Now a profit warning, together with some bondholders rejecting Rallye’s plan to repay 1.6 billion euros of debt over 10 years, throw into question Casino’s nascent recovery.

The retailer on Thursday halved its forecast for the expansion in trading profit in 2019 to 5%, after fourth-quarter retail sales were worse than expected. Strikes in France during the crucial holiday shopping period shaved about 2% off of its fourth-quarter sales. It wasn’t alone. Fnac Darty SA, which sells books, music, electronics and home appliances, also said the unrest over a proposed pension overhaul hurt its revenue. But Casino shares fell as much as 13%, the most in more than a year, indicating that investors weren’t convinced the problems are confined to the disruption.

While both Casino and Rallye were saddled with debt, the underlying French business has been in acceptable shape, with exposure to faster growing segments such as convenience stores. If this stability is now under threat, that is a concern, not just for Casino’s progress, but Rallye’s restructuring too.

Bondholders rejecting Rallye’s plan — with the company failing to win support in four out of five euro-bond classes — is a sign the coast isn’t yet clear on that front either. But the vote isn’t binding on the Paris court that’s set to rule on the plan by the end of March.

However, the profit warning doesn’t make the situation any easier. First, Rallye’s main asset is its 52% holding in Casino, so a weaker share price might make creditors, particularly the banks, feel less comfortable with the plan. Second, the revised profit guidance makes it even more difficult for Casino to generate cash to pay the dividends to Rallye that are necessary for the group to reduce its own borrowings.

Casino has said that it will not make a distribution this year. After that it can make a payment, but its ability to do so will be capped by the terms of its recent refinancing. There could be special dividends from a sale of the Leader Price discount chain to Aldi, which is being discussed, or offloading assets in Latin America, but returning to regular pay-outs looks even more challenging.

Of course the share price decline may have another effect: Making a takeover of Casino more likely. Rivals in France’s highly competitive supermarket industry, such as Carrefour SA, have a duty to a look to see if they can make hay from the retailer’s misery. Casino also has an online partnership with Amazon.com Inc. It’s also worth watching what Czech billionaire Daniel Kretinsky and his partner Patrik Tkac have up their sleeves after they acquired a 4.6% stake in Casino last year.

But until any suitor shows their hand, Casino investors and bondholders face the prospect of a long, drawn out grind toward better times. As for short sellers, they get another spin of the wheel.

--With assistance from Marcus Ashworth.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2020 Bloomberg L.P.