High-Priced S&P 500 Stumbles on the Brink of Making History

The previously unstoppable S&P 500 is stumbling at history’s door, its momentum stalled at the precipice of an all-time high.

(Bloomberg) -- The previously unstoppable S&P 500 is stumbling at history’s door, its momentum stalled at the precipice of an all-time high. As to what’s slowing its step, the past may offer some clues.

While the benchmark index eked out another positive week, its sixth in seven, there was evidence of a tempering in trader spirits, with the index twice threatening to close at a record high before falling back. Volume in American shares eased noticeably over the five sessions, and the S&P 500 managed to post three down days, which hadn’t happened since June.

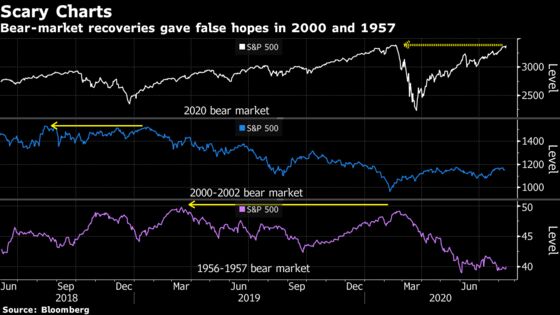

Market history is generally kind to stocks when they’re exiting bear markets -- rallies usually pick up speed at the top and get stronger from there. Two exceptions stand out, though, which may have significance in explaining the recent lethargy: 2000 and 1957. Both years, stocks staged huge comebacks from gut-wrenching losses, amid a backdrop of stretched valuations. Both times, the gains didn’t last.

As anyone watching equities knows, elevated valuations are a calling card of this comeback, too, with the S&P 500 trading north of 26 times annual earnings. Price-earnings ratios that high are unusual at this stage of a bear-market recovery -- and that gives some strategists pause, when pondering the future.

“The fact that S&P 500 valuations are currently so much higher than at any comparable breakout convinced us that this is a higher-risk one to ‘chase’ than any past instance,” Doug Ramsey, Leuthold Group’s chief investment officer, wrote in a note. “Any break above that high will be underwhelming, if not a potentially historic ‘trap.’”

The S&P 500 added 0.6% over five days. It popped above its week Feb. 19 closing twice in the week, though ended 0.4% shy of it. The Nasdaq 100 added 0.2%, while the Russell 2000 Index of smaller companies rose 0.6%. The Dow Jones Industrial Average performed better, climbing 1.8%.

For now, a five-month uptrend in the S&P 500 remained intact. But this week’s price action is a sign gains may get harder to come by now, as they did in the two similar prior examples.

During the 1956-1957 bear market, the S&P 500 initially bounced back to within 1% of its prior peak, only to fall another 20% before the ultimate bottom settled in three months later. When the dot-com crash occurred in 2000, an early decline was followed by a nearly full recovery by early September. Again, that bounce didn’t hold and gave way to a plunge that eventually wiped out half of the market’s total worth.

Of course, those instances differ in significant ways from now, monetary policy in particular. But they also share two key attributes that draw a striking parallel. First, much like today, both followed a powerful rally. Their preceding bull markets were the only ones in history where the the S&P 500’s total returns exceeded 450%.

Second, valuations were stretched. In July 1957, when the S&P 500 was about to break out, its cyclically-adjusted price-earnings ratio was a third above its 50-year average. The premium, at 140% in September 2000, is almost 50% now, according to data compiled by Robert Shiller, a professor at Yale University.

“When the recession is over, I can see the S&P 500 being higher than it is today, but basically I think it’s fully priced at this point,” Byron Wien, the vice chairman of Blackstone Group Inc.’s private wealth solutions business said in an interview on Bloomberg Television and Radio. “We are growing gradually. We are about a quarter of the way back to where we were in 2019. But we have a long way to go.”

By Leuthold’s count, the market is already in uncharted waters. Rather than tracking stocks day in and day out, Leuthold keeps score on a monthly basis. Going by that, the S&P 500 just eclipsed the prior month-end bull market peak while making an all-time high in the process. Such a breakout has occurred 10 other times since 1957; none came with a higher price-earnings multiple than now.

To Michael Shaoul, chief executive officer at Marketfield Asset Management LLC., the swift turnaround and tech’s persistent leadership through this year’s ups and downs showed the March selloff was merely an interruption to the bull market that started in 2009. The urge from global policy makers to fight the pandemic could fuel equity bubbles like the one in Japan during the late 1980s and another during the internet boom roughly 10 years later, he warned.

“Under current circumstances, the odds of central banks being ‘third time lucky’ appear to be remote,” Shaoul said. “We increasingly believe that we are heading for some form of ‘bubble trouble’ along the road.”

Besides valuation, another contour of the recovery rally that is sowing angst among strategists is its lopsidedness, the often-observed fact that a small core of megacap technology stocks is shouldering virtually all of the gains. When so much of the market return amasses in so few shares, it creates pressure on fund managers to own them, raising the threat of what analysts call “concentration risk” should everyone bail at once.

While the timing of unwinding is impossible to predict, the risk is looming large. Bank of America strategists led by Savita Subramanian found that money managers are hugging the S&P 500 more than any time in seven years.

To be sure, stocks can keep rising. And a strategy of buying stocks at the point of a full bear-market recovery has reaped gains in all but one of 12 instances. On average, the S&P 500 advanced 4.5% over the following six months.

But be prepared for turbulence. Consider 2007, when stocks wiped out the 2000-2002 bear market losses in May, only to see a mere 2% upside before another full-blown down cycle began that October. A similarly scary pattern played out in 1989. After making a round trip from the 1987 crash, the S&P 500 settled in volatile range trading. It eventually lost momentum and a new bear market started in July 1990.

Such perilous outcomes pose a dilemma for investors who are tempted to jump in after being left behind by the rally, according to Kevin Caron, portfolio manager for Washington Crossing.

“The challenge comes with somebody who has pulled money out of the market and is now considering if they should get back in,” Caron said. “That’s the most difficult scenario to deal with.”

©2020 Bloomberg L.P.