Mining’s Dirty Secret Won’t Survive a Changing Climate

(Bloomberg Opinion) -- Can mining be green?

That’s certainly the ambition of some of the biggest companies in the sector. Rio Tinto Group last year became the first major miner to stop digging up coal altogether. Glencore Plc, historically one of the commodity’s most vocal boosters, has promised to cap production at current levels.

“We have a portfolio free of coal and oil and gas,” Rio’s Chief Executive Officer Jean-Sebastian Jacques told investors after annual results last month. “We are well-positioned to thrive in the world that values sustainability more and more.”

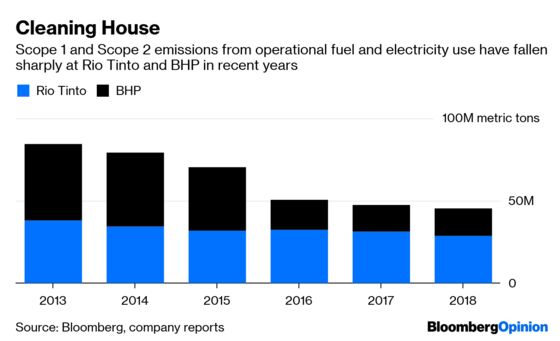

Well, up to a point. Miners have certainly been working to reduce the impact of their own operations. Partly thanks to asset sales and spinoffs, carbon pollution from on-site fuel and electricity – so-called Scope 1 and Scope 2 emissions – has fallen by almost half in the past five years at the two biggest players, Rio Tinto and BHP Group.

Still, judging mining companies on the basis of their operational emissions is a bit like judging tobacco companies on the basis of their record on labor rights and board diversity. It’s interesting and worthy, but ultimately misses the big picture.

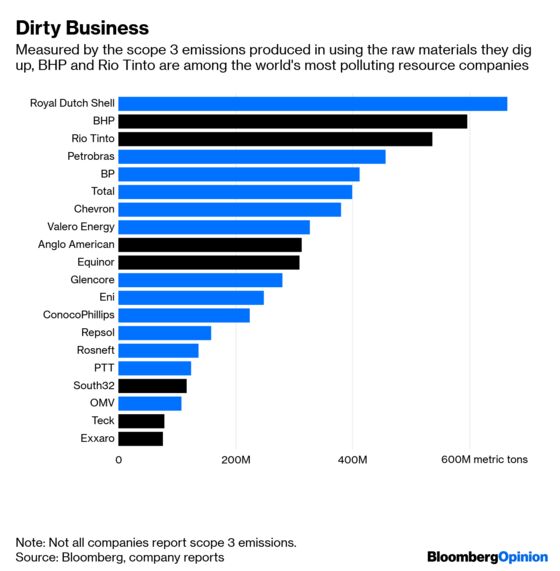

Take a look instead at Scope 3 emissions – those that result when the products are consumed – and a very different picture emerges:

On that measure, of resources companies for which Bloomberg has data only Royal Dutch Shell Plc is a bigger emitter than Rio and BHP, both of which feature on S&P Global Inc.’s Dow Jones Sustainability Indexes. Soot-stained coal dinosaurs like Glencore, and Exxaro Resources Ltd. come in well down the ranking.

How to account for the difference? It’s ultimately about steel.

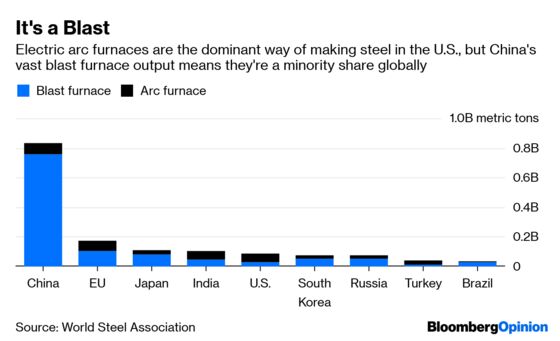

Producing a single metric ton of steel in a blast furnace typically releases around 2.3 tons of carbon dioxide into the atmosphere, not much less than you’d get from burning a ton of thermal coal for energy. Moreover, the commodity portfolios of the two biggest miners and Vale SA are dominated by the key blast furnace feedstocks of iron ore and (in the case of BHP) coking coal.

The fact that steel raw materials have escaped the image problem suffered by thermal coal isn’t so much that they’re cleaner, as that they appear to be harder to replace. As we’ve argued, the plummeting costs of renewables and gas mean that you don’t even need a price on emissions to undermine thermal coal on a purely financial basis – something even Glencore is starting to recognize.

The same hasn’t been true with steel. Despite the rise of electric arc furnaces – which recycle steel scrap and generate a fifth or less of the carbon emissions associated with blast furnaces – traditional technology remains dominant because the metal it produces tends to have fewer impurities, and the world simply lacks sufficient scrap to supply a demand boom like the one China experienced over the past two decades. Profit margins tend to be better, too, although the high capital outlays involved in building blast furnaces reduce that advantage.

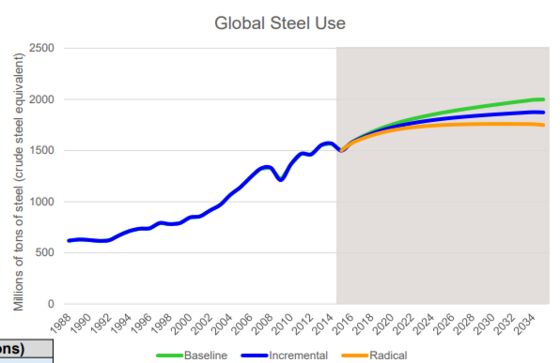

The future could look very different. China’s steel consumption peaked last year, according to the Australian government. Other emerging countries might be expected to make up for that decline, but there’s no guarantee they’ll industrialize at the same extraordinarily steel-intensive pace. Should consumers switch to more frugal habits, current demand levels of around 1.7 billion tons a year may already have hit a long-run plateau, according to one 2017 study for the Organization for Economic Co-operation and Development:

That might seem at least to guarantee big miners a steady-state continuation of current profitable conditions, but the growing wave of worn-out material may change that calculus. Scrap supply will grow to 1 billion tons by 2030 from about 750 million tons at present, according to the World Steel Association, and climb further to 1.3 billion tons in 2050. If all of that is used in mini-mills and total demand peaks at current levels, production via the blast-furnace route could fall by around two-thirds.

As with thermal coal producers 10 years ago, the continuing business model of steel raw material suppliers depends upon the world deciding that tackling the pollution from the products they sell is simply too hard. It’s ultimately a bet that the relatively slight economic advantages of conventional technology over greener alternatives won’t be eaten away by better technology, regulation, or a price on carbon emissions.

A shift toward the pattern that now exists in North America or India – where blast furnaces are used mostly for specialty high-quality steel, with direct reduced iron playing a bigger role to dilute out scrap impurities in mini-mills – would be devastating for all those long-life assets that big miners like to boast about.

Still, with steel and iron accounting for about 8 percent of global emissions, it’s what’s needed if the world is to avoid disastrous climate change. Miners currently touting their environmental credentials should watch out. That shiny green image could turn rusty surprisingly quickly.

Not all companies publish estimates of Scope 3 emissions, so Exxon Mobil Inc., Vedanta Resources Plc, and almost the entire Asian mining and energy industry don't show up in the rankings.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.