Pemex Feels Incoming President’s Heat as Investors Dump Bonds

Pemex Feels Incoming President’s Heat as Investors Dump Bonds

(Bloomberg) -- For a peek at how worried investors are about Mexico’s incoming president, look no further than Petroleos Mexicanos, the state-owned oil giant. Its 30-year debt slumped to about 82 cents on the dollar in just three weeks -- and it’s the company Andres Manuel Lopez Obrador pledged to save.

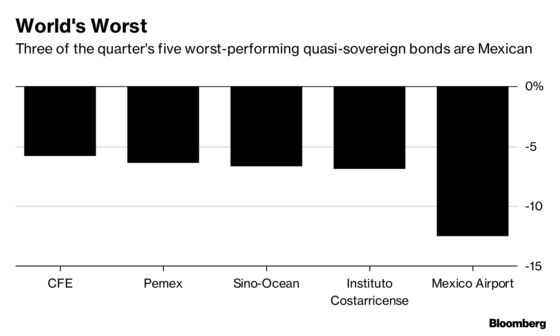

Pemex is hardly alone. Debt sold to finance a now-scrapped airport are the world’s worst-performing quasi-sovereign bonds this quarter, and those issued by Comision Federal de Electricidad, the state electricity company, have also tumbled. Yet Pemex dwarfs both: Its debt now stands at more than $106 billion.

It’s a remarkably graphic representation of just how much AMLO, as Mexico’s new leader is known, has managed to rattle financial markets since he began ramping up populist rhetoric almost three months after his resounding July 1 electoral victory. Pemex has another reason for anxiety, too: Crude oil prices have fallen 7.7 percent this year.

"Pemex is the most vulnerable credit in Mexico right now," said Shamaila Khan, director of emerging-market debt at AllianceBernstein in New York. "Pemex has a very large capital structure, it has one rating that’s on the fringe of below investment grade, and AMLO’s policies are very uncertain with respect to energy reform."

The president-elect’s decision in late October to cancel the $13 billion Mexico City airport, after holding a referendum, hammered bonds and raised concern that other government projects could be at risk. Pemex, which under the current administration of Enrique Pena Nieto embarked on a path to open up to international markets, is seen as particularly at risk. Lopez Obrador’s promise to cut salaries for public employees has also raised fears of mass exit from the company.

“It’s a perfect storm between the advancement of the concept of referendums in Mexico combined with the capital requirements of Pemex,” said William Perry, a portfolio manager at Stone Harbor Investment Partners in New York. “After seeing what happened to the Mexico airport and ultimately to the airport bonds, investors are particularly wary about what’s next.”

What’s most surprising about the pressure on the company is that during his campaign, Lopez Obrador vowed to resurrect the embattled firm. Now, that plan is in doubt. AMLO wants to increase spending, potentially adding to debt that already tops any other Latin American corporate borrower and reversing its strategy of reducing new borrowing.

While Lopez Obrador pledged to reverse an almost 14-year stretch of oil production declines at Pemex, promising 75 billion pesos ($3.7 billion) to help boost oil output by 600,000 daily barrels during the next two years, investors aren’t convinced. For one thing, Pemex’s next chief executive officer, Octavio Romero, lacks an oil background, and senior staff who could help steer the ship are instead jumping off amid concern Lopez Obrador’s administration could cut salaries through a new law.

Moreover, the new government aims to dial back 2014 oil reforms that were designed to attract private investment and allow Pemex to receive financial and technical support from partners. The leftist leader has said that he would suspend new oil auctions and will review the 107 exploration and production contracts already awarded through previous tenders.

Adding to problems on the horizon, the global crude rout threatens to reverse a much-needed oil price recovery for Pemex, which was forced to let go about 16 percent of staff since 2015 and suspend new projects to cut costs. Oil prices hit a new low for the year on Tuesday, falling more than 6 percent in New York and London, raising doubts about OPEC’s commitment to production cuts and escalating trade tension.

Some analysts fear that rather than focusing on how to address the crude conundrum, the new government is eyeing instead a new, several-billion-dollar refinery that will drain resources and detract from Pemex’s core business. Lopez Obrador has said that he will eventually stop oil exports in favor of feeding crude to Mexico’s six ailing refineries, which are operating at 37 percent of capacity, about the lowest in a quarter century. He has pledged 50 billion pesos to raise refining capacity and another 50 billion pesos next year for a new plant in his home state of Tabasco, should Mexicans vote for it in a nationwide referendum planned this Sunday.

"Such a project would have challenging economics as it would compete with the U.S., the world’s most efficient refined products market,” said Pablo Medina, vice president of Welligence Energy Analytics, a research firm based in Houston.

To contact the reporters on this story: Justin Villamil in Mexico City at jvillamil18@bloomberg.net;Amy Stillman in Mexico City at astillman7@bloomberg.net

To contact the editors responsible for this story: Rita Nazareth at rnazareth@bloomberg.net, ;Carlos Manuel Rodriguez at carlosmr@bloomberg.net, Alec D.B. McCabe

©2018 Bloomberg L.P.