(Bloomberg Opinion) -- Who’d ever think the maker of a $2 million sports car would offer a lesson on austerity?

The global auto market faces its share of challenges these days: the trade war, China’s slowdown and Brexit, not to mention disruptive technologies, the threat of new regulation and rising costs. McLaren Automotive Ltd. has navigated this bumpy terrain by carefully managing costs.

The company started selling its latest series in 2011, in a market still struggling to rebound after the global financial crisis. Lessons from that period are fresh for Chief Executive Officer Mike Flewitt, who spent almost a decade at Ford Motor Co.

The company, which released its iconic F1 model in 1992, appeals to a (very) thin slice of the market, with just around 4,800 units made globally last year. Its strategy won't be the same as the likes of General Motors Co. or Honda Motor Co. Still, McLaren’s disciplined approach is a reminder to rivals that have tried to crank up production or stretch into new products and markets at any expense.

In recent years, the likes of Ford, Jaguar Land Rover Automotive Plc., Honda and GM have expanded rapidly. But that strategy can backfire if you don’t gauge demand correctly. For many, volumes have risen and margins have thinned. Each on that list has had to announce painful cost cuts recently – and even those are unlikely to go far enough.

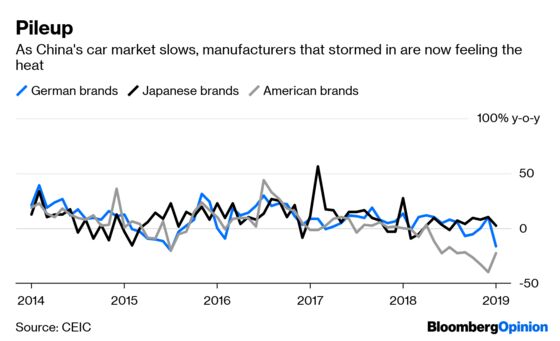

That failure is nowhere more apparent than in China. There, global carmakers took a kitchen-sink approach: Throw everything in and hope something sticks. Too few (read: the Americans) looked for long-term profit streams and strategies that would leave them nimble. So while mainland sales grew to account for as much as 40 percent to 50 percent of global net income last year for some manufacturers, margins are shrinking fast and cars aren’t selling. This will only become more pernicious as the market matures.

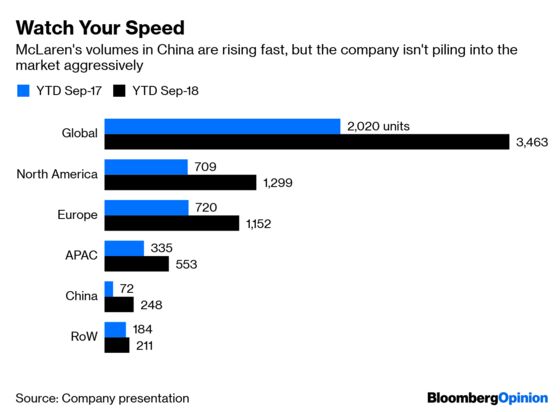

China is one of McLaren’s fastest-growing markets – consumers there still covet exclusivity – but it’s far from the company’s largest. The automaker sold around 400 units there in 2018, a sliver of a market that moves more than 20 million cars a year.

That small scale gives McLaren some flexibility. Deciding how much to sink into the country can come from more qualitative assessments, such as exclusive dinner conversations with high-net-worth buyers and dealers. There, executives might assess how flush customers feel by asking about the stock market, or suss out whether it's socially acceptable to be seen driving a McLaren these days. (Some buyers have been known to stockpile cars in London garages during periods of excessive scrutiny.)

McLaren has also taken care to spread its risk across markets and keeps a close eye on costs. The company, for instance, doesn't have any plans to follow competitors Aston Martin Lagonda Global Holdings Plc and Automobili Lamborghini SpA into sports utility vehicles just for the sake of competition. That would require an investment of at least $500 million, Flewitt said in an interview.

The executive also notes that the company maintains its cost base at a break-even level, managing fixed costs versus variable ones. The auto unit of privately held Mclaren Holdings Ltd. brought down costs as a percentage of sales for the better part of the last decade – to 57 percent compared with the industry average of 80 percent. Usually, as fixed costs grow, companies need higher revenue to break even.

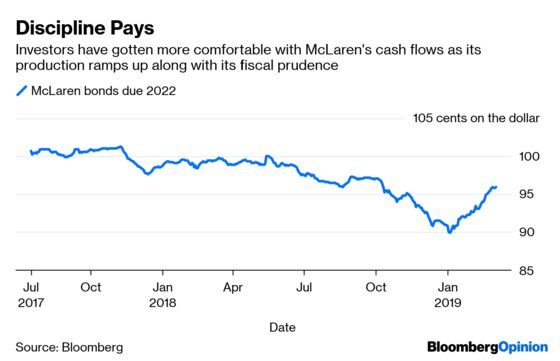

The business of race cars is expensive, though, and McLaren’s fine financial and operational balance has its share of pressure points. While the company’s leverage has come down slightly in recent months it remains elevated. Cash flows also remain tightly managed.

Still, McLaren’s business plan is fully funded through 2025 – spending around 1 billion pounds ($1.31 billion) over the next seven years. A public offering isn’t an option for now, the executive says.

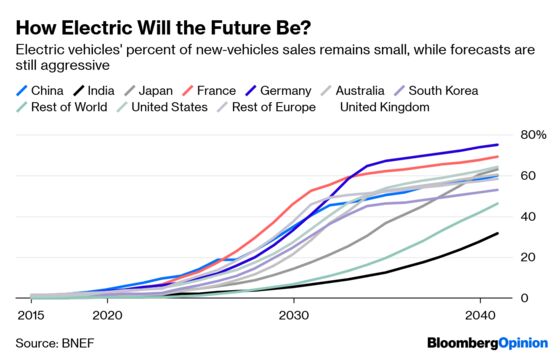

Other carmakers that threw themselves into electric vehicles and autonomous driving might do well to take a page from McLaren's book. Flewitt is pretty grounded about the inevitable transition to electric cars: “It’s going to be a lot slower than people think it is.” As of December, electric vehicles accounted for 0.2 percent to 3 percent of new vehicle sales, depending on the region.

We've already seen some of the wreckage after too many companies sped into the future without a clear game plan. Sometimes the scenic route can be the most direct.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.