(Bloomberg Opinion) -- Global investors seem to be balking at the idea of handing Masayoshi Son another $100 billion to play with.

Some money managers, from sovereign wealth funds to pension funds, plan to make limited or no contributions to the SoftBank Vision Fund II, the Wall Street Journal reported, citing people familiar with the matter. The investment vehicle is the successor to the SoftBank Vision Fund, a $100 billion investment vehicle started by Son’s SoftBank Group Corp.

Even the largest backer of Son’s initial fund, the Saudi Arabian Public Investment Fund, doesn’t appear keen to sign on for a second time. Investors see better choices out there, with many of the biggest funds already having established programs to invest directly in late-stage startups, according to the Journal.

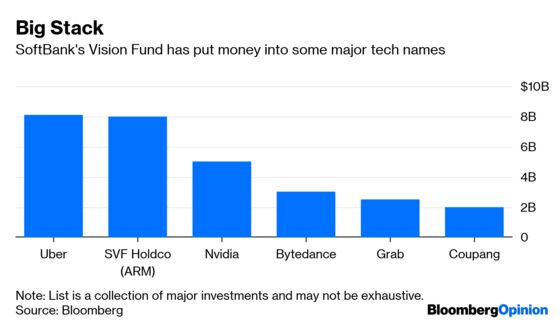

There’s a growing sense not only that the Vision Fund may be a one-hit wonder, but that the days when larger bets meant more lucrative payoffs are behind us. SoftBank founder Son muscled his way into some of the world’s biggest unicorns with his checkbook, becoming the most fearsome weapon in startup land. The result has been fabulous returns for the fund, even if most of the companies it has invested in have never spun a profit (and may not for many years to come).

Son seems to be learning that his new fund will need a new approach. Signing up the Saudi fund as the main backer doesn’t seem likely. If he continues with the same unicorn-hunting strategy, then other sovereign wealth funds, such as those in Norway or Singapore, would be obvious targets. Yet they might be deterred by the Vision Fund's lack of transparency, and don't necessarily need Son's star power to open doors. And they have their own vehicles for startup investing. Singapore for example, has Vertex, which itself is bringing in outside money.

Pension funds, on the other hand, need stability of cash flow. While they may be able to wire a few billion dollars to Son in a heartbeat, their managers want to know when to expect that cash back. And the fund’s continued relationship with Saudi Arabia will be of concern, following the murder of Jamal Khashoggi by Saudi agents in Turkey last year.

That means the new fund will probably need to scrounge from dozens of rich individuals and family offices to cobble together the same pool of money. One upside is that no single investor will be able to call the shots – for the first Vision Fund, the Saudi fund and Abu Dhabi’s Mubadala Investment Co. both have veto rights on deals over a certain size.

But getting one $45 billion check from an authoritarian government with a questionable human-rights record is much easier than chasing down 45 checks for $1 billion from wealthy individuals, each of whom will have an opinion on how Son should make them even richer.

The final question Son faces is what exactly his fund will invest in. It’s not mere cynicism to suggest that this doesn’t matter. After all, as my colleague Shuli Ren pointed out recently, Son’s management team gets to make money just from management fees. Revenue from alternative investing has grown to surpass the money made from managing active equity or debt funds, according to Bernstein Research.

Instead of continuing to hunt for the next Uber Technologies Inc., it’s possible Vision Fund II will find itself cutting checks in the realms of private equity and debt, where there’s plenty of possibilities and which serve as a great place to funnel piles of cash. That’s not as sexy as funding the world’s biggest unicorn, but it pays the bills. And above all else, Son’s next fund will be all about paying the bills.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2019 Bloomberg L.P.