M&A Glut Too Little Too Late to Save Europe Junk Loans in 2020

M&A Glut Too Little Too Late to Save Europe Junk Loans in 2020

(Bloomberg) -- This year has proved to be grim for European investors hunting for higher-yield loans, and even a recent spate of M&A deals will struggle to turn their fortunes around.

As much as 10 billion euros ($11.8 billion) in new debt could enter the M&A pipeline following the buyout of Asda Group Ltd if other potential deals, such as G4S Plc, William Hill Plc and Ahlstrom-Munksjo Oyj, come to fruition.

But even if all those deals come to pass, the debt raising will be spread across loan and bond investors in Europe and the U.S., and some of these financings might not reach the market until next year. Public-to-private transactions, as most of these are, can have long lead times and may not even materialize.

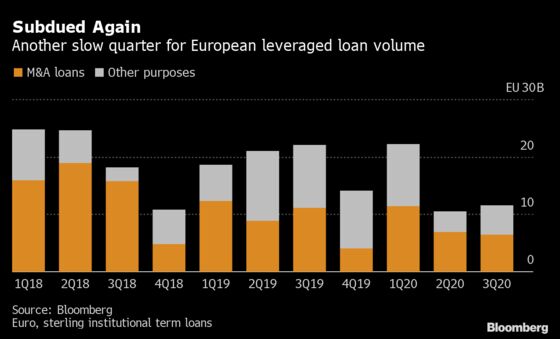

So far in 2020 M&A-linked leveraged loan sales in Europe have slumped to their lowest in four years, to 25 billion euros, data compiled by Bloomberg show. But nearly half of that was sold in January and February, and September was unusually slow compared with the usual rush.

“Although there are several sponsor buyout processes currently underway, the committed loan pipeline in September 2020 was lower compared to prior years,” Joe Bishay, Bank of America’s head of European leveraged finance capital markets, said.

Lumpy, Sluggish

The fourth quarter will bring some deals in front of lenders. Asda’s 4 billion-pounds of debt may be sold down late this year, and nearer at hand banks are preparing to launch loans and bonds for Advevinta ASA’s acquisition of eBay Inc.’s classifieds division this month, according to people familiar with the matter. Ineos Styrolution is also waiting to sell new M&A financing.

But away from these big names, M&A activity is tentative and underwriting banks say buyouts remain scarce.

Many potential deals are delayed into 2021, says Simona Maellare, co-head of UBS’s alternative capital group, adding that the big challenge for private equity firms is deciding how much to pay for a new business. That is making it difficult for many of them to strike new deals while the outlook is so uncertain, she said.

Read more: Lockdowns Put Valuations in Doubt, Holding Back M&A Revival: UBS

Thin supply is a problem for the nearly 60 firms that manage collateralized loan obligations in Europe and that could see their market seize up without new deals to feed into their vehicles.

Loans also attract a range of global pension funds, credit opportunity funds, and other investors that want debt with a first-ranking claim over assets where the yield helps to counter the impact of low and potentially falling interest rates.

Would-be buyers may also be tempted to hold fire if they see companies come under further stress as lockdowns continue to roll out and state support programs fall away.

“There are substantially different forecasts about how much defaults may pick up over the next year, but the withdrawal of government support will boost defaults and likely depress asset prices,” Alexander Batchvarov, international structured finance strategist at Bank of America Global Research.

“Why not wait to pick up these assets on the cheap?”

©2020 Bloomberg L.P.