Australia’s Central Bank Is Reviewing Three Key Issues on Policy Easing

Australia’s Central Bank Is Reviewing Three Key Issues on Policy Easing

(Bloomberg) --

Australia’s central bank chief Philip Lowe said his board is assessing whether buying longer-dated bonds would help spur hiring, sending the currency and yields lower on bets of additional monetary easing.

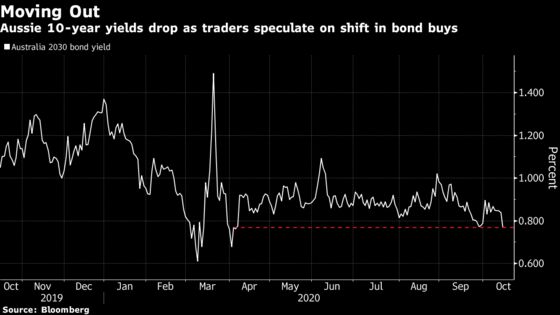

In response to a question after an address in Sydney, the governor noted that Australia’s 10-year yields are higher than “almost everywhere in the world.” The bank is trying to understand whether that’s because, after buying longer-dated securities in March, it had since stopped, he said.

“If we buy government bonds in the 5-10 year range, is that going to create more jobs? How would it create more jobs?” he said ahead of data that showed unemployment climbed in September to 6.9%. “We’re taking our time to work through that issue, it’s a very important issue but also quite complex. But that’s what we’re discussing at every one of our meetings.”

The Australian dollar dropped and bond yields declined across the curve, led by the 10-year, which fell as much as nine basis points to 0.75%, its lowest since April. Traders dialed up expectations that the Reserve Bank of Australia would aim to bring down the 10-year yield in addition to holding down the three-year via its yield curve control.

“The QE question is more live following these comments,” said Andrew Ticehurst, a rates strategist at Nomura Holdings Inc. in Sydney. “We suspect QE is still not fully priced, so delivery of this on Nov. 3 - the most likely timing for the next move in our view - would likely see a further decline in long-end yields.”

In the speech, Lowe had said he’s working through how much potential traction any further easing will gain, the potential effect on financial stability of such a move, and what international counterparts are doing before taking any new policy steps.

“We have been considering what more we can do to support jobs, incomes and businesses in Australia to help build that important road to the recovery,” Lowe said in the speech to a Citigroup Inc. conference. “The board has not yet made any decisions.”

The RBA has taken on a support role during the pandemic crisis due to limited conventional ammunition, undertaking a bond-buying program to lower borrowing costs and allow the government to deploy a vast fiscal stimulus program. The RBA in March, at the height of Covid uncertainty, cut its cash rate to 0.25% and set the same target for the three-year yield as a sign to firms and households that rates will stay low.

What Bloomberg’s Economists Say

“Our takeaway from RBA Governor Lowe’s speech is that monetary policy is going to be on hold for as long as it takes, and longer than implied by the RBA’s decision to choose a 3-year yield target. The speech, and October board statement, elevated the importance of the labor market, which the government’s fiscal projections do not expect to deliver enough wage pressure to achieve the RBA’s 2-3% inflation target at any stage over the next 4 years. Rates are on hold for longer, and if the RBA believes they can boost growth with further policy easing, they will.”

James McIntyre, economist

Australia’s early lifting of restrictions and reopening of the economy was dented by a renewed outbreak in the southeastern state of Victoria. The economy has since tipped into recession and Treasury estimates unemployment will peak at 8% this quarter.

“In terms of unemployment, we want to see more than just ‘progress toward full employment,’” Lowe said in his speech. “We want to see a return to labor market conditions that are consistent with inflation being sustainably within the 2% to 3% target range.”

In an address last month, RBA No. 2 Guy Debelle laid out the following potential policy options:

- Buying bonds further out along the curve, supplementing the three-year yield target

- Currency intervention, though he noted that “with the Australian dollar broadly aligned with its fundamentals, it is not clear this would be effective in the current circumstances”

- Lowering the current structure of rates in the economy a little more, without going negative; and

- Going negative. Debelle said the evidence is “mixed” on this policy and restated some of the advantages and pitfalls

Lowe, responding to another question, noted that cutting rates to 0.10% or buying longer-dated bonds “realistically” wasn’t going to help drive inflation back to its 2-3% target.

“So a longer-term question we’re also considering is how does the inflation targeting framework sit in this world that we’re currently in,” he said. “We’ve had some difficulty over recent years of averaging inflation at 2% and the pandemic is going to make that much more difficult. So what role does that have and that role has to evolve over time.”

©2020 Bloomberg L.P.