Lost Faith in Politics? Take Another Look at Macro: Taking Stock

Lost Faith in Politics? Take Another Look at Macro: Taking Stock

(Bloomberg) -- Want the lowdown on European markets? In your inbox before the open, every day. Sign up here.

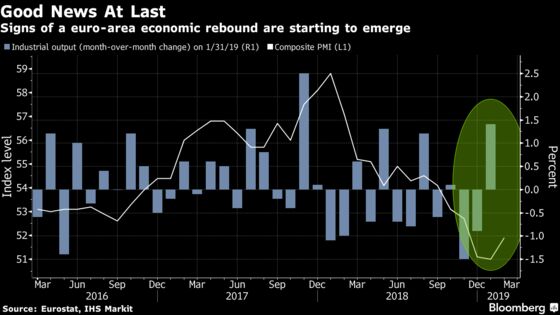

European stocks seem range-bound in a consolidation phase as they await their next catalyst and uncertainty over Brexit lingers. A delay seems pretty much certain now that a no-deal is off the table. No matter, investors can turn to macro signals to see what lies ahead. And the recent figures look better than what people had feared.

Industrial output in the region was surprisingly strong at the start of the year, driven by France, Italy and Spain. Purchasing Managers’ Index data are also bottoming out, which could suggest the return of positive momentum for the economy.

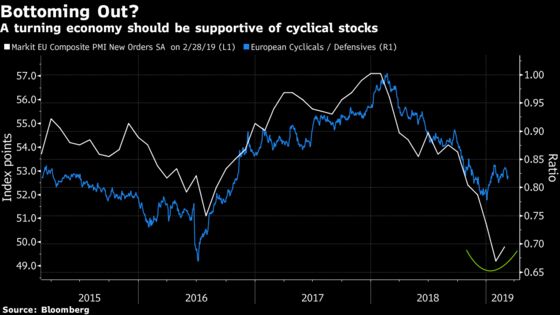

Bouncing economic activity in Europe is helpful for stocks while bond yields are likely to start rising again, which should be good for cyclicals in particular, according to Barclays.

Bank of America Merrill Lynch quantitative strategists have also noticed some flags for growth in Europe. Their proprietary macro signal stopped falling for the first time in a year, the 10-year bund yield is near a bottom, while European leading indicators have improved. The pause in central banks’ policy normalization is another boost to shares, they write.

For the strategists, it might be time to brave the extreme levels at which European markets are trading. That idea is backed by a yield gap between European stocks and bonds, which BofAML says is at its widest in nearly 100 years, while relative trading levels are at a 50-year low in dollar terms.

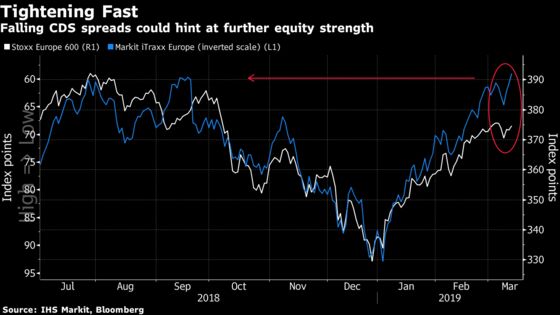

Looking at credit spreads, it also seems the risk premium keeps falling. The iTraxx Europe has broken the 60 level, its tightest since September, hinting that the general sentiment for equities is turning increasingly positive. This looks like a key signal to watch.

Ahead of the open this morning, Euro Stoxx 50 futures are little changed.

- Watch the pound and U.K. stocks after U.K. lawmakers decided they don’t want the nation to leave the European Union without some sort of divorce deal. It’s not legally binding though. There will be more voting tonight when Parliament decides whether the U.K. should request an extension to Brexit.

- Watch U.K. homebuilders after the Royal Institution of Chartered Surveyors headline price index dropped in February to the lowest level since 2011, its fifth straight monthly decline.

- Watch oil and oil producers as OPEC publishes its monthly update on demand forecasts and production data today. Last month the group reduced its estimate for the amount of crude the world needs it to pump this year, due to thriving U.S. production and faltering demand. Futures have gained this week on the back of Saudi Arabia pressing on with planned curbs, the Venezuela crisis and Iran sanctions.

- Watch trade-sensitive sectors as China’s economic slowdown deepened in the first two months of 2019, with unemployment sharply higher, industrial output posting its worst start to a year since 2009, and retail sales expanding at the slowest pace since at least 2012. On the plus side, fixed-asset investment picked up, allaying concern that the ongoing trade war could start to hinder a recovery that began last summer.

COMMENT:

- “Given the expected macroeconomic slowdown, we think U.S. and European earnings will grow 5 percent this year,” BNP Paribas strategists write in their second-quarter 2019 global outlook. “After an 11 percent recovery this year, global equities are no longer pricing in a significant risk of recession, in our view. A demand-driven shock to earnings could send equities into a new bear market.”

COMPANY NEWS AND M&A:

- Casino Plans to Sell Another $1.1 Billion of Assets to Cut Debt

- Lufthansa Cuts Growth Plans After Slump in Annual Earnings

- Austrian Post FullYear Ebit Meets Estimates

- Lenzing Full-Year Net Income Misses Lowest Estimate

- Lanxess ’18 Adj. Ebitda Matches Ests, Sees Similar Level in ’19

- K+S Sees ‘Significantly Higher’ Earnings as 2018 Beats Estimates

- RWE to Raise 2019 Dividend in Challenging Year for Fossil Power

- Carrefour Lures West Africa Shoppers From Markets Into Malls

- Sports Direct’s Debenhams Loan Offer Includes Naming Ashley CEO

- Generali Full-Year Profit Increases on Disposals, Life Insurance

- Sixt Leasing Cuts Operating Rev. and EBT Target For 2021

- VW Move to Pull Europe’s Largest IPO Casts Shadow on 2019 Market

- Elliott Wins More Support in Telecom Italia Fight With Vivendi

- Vifor Pharma Sees 2020 Net Sales Exceeding CHF2B

NOTES FROM THE SELL SIDE:

- Morgan Stanley upgraded TUI to overweight, citing dividend and balance sheet secure, valuation attractive and possible help from a softer or delayed Brexit. The bank sees share price reaction YTD as overdone, with investors still concerned about possibilities of further downgrades, dividend and balance sheet.

- Bankhaus Lampe upgraded Kloeckner to hold, removing the stock’s last negative rating among analysts tracked by Bloomberg, with co.’s 2019 Ebitda seen benefiting from changes in IFRS 16 accounting rules for leasing.

- Erste Group is raised to overweight at Morgan Stanley, which bases the upgrade on reasons including potential for cost efficiencies looking underappreciated and a stable capital outlook. Estimates top-line growth at 3.5% 2018-21 CAGR vs Eurozone banks at 2%.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 379.9 (23.6% Fibo); 383 (trend line)

- Support at 369.4 (200-DMA); 365.1 (38.2% Fibo)

- RSI: 64.8

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,340 (March high); 3,360 (trend line);

- Support at 3,315 (38.2% Fibo); 3,282 (200-DMA)

- RSI: 66.5

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Aryzta upgraded to buy at Baader Helvea; PT 1.60 Francs

- Erste upgraded to overweight at Morgan Stanley; PT 40 Euros

- Kloeckner upgraded to hold at Bankhaus Lampe

- Quilter upgraded to overweight at JPMorgan; PT 1.80 Pounds

- TUI upgraded to overweight at Morgan Stanley; PT 12.50 Pounds

- Ultra Electronics upgraded to buy at Berenberg

DOWNGRADES:

- Adidas cut to hold at Baader Helvea; Price Target 220 Euros

- Eurofins Scientific downgraded to reduce at HSBC; PT 347 Euros

- Schindler downgraded to hold at SocGen; PT 230 Francs

- Systemair downgraded to hold at Kepler Cheuvreux; PT 108 Kronor

INITIATIONS:

- Bushveld Minerals rated new outperform at Macquarie; PT 47 Pence

- Energean Oil & Gas Rated New Buy at Peel Hunt; PT 8.50 Pounds

- Generix Group SADIR rated new buy at IDMidcaps; PT 5 Euros

- On The Beach rated new buy at Citi; PT 5.10 Pounds

MARKETS:

- MSCI Asia Pacific down 0.4%, Nikkei 225 little changed

- S&P 500 up 0.7%, Dow up 0.6%, Nasdaq up 0.7%

- Euro down 0.07% at $1.1319

- Dollar Index up 0.11% at 96.66

- Yen down 0.37% at 111.58

- Brent up 0.3% at $67.8/bbl, WTI up 0.2% to $58.4/bbl

- LME 3m Copper down 0.4% at $6448/MT

- Gold spot down 0.4% at $1303.7/oz

- US 10Yr yield up 1bps at 2.63%

MAIN MACRO DATA (all times CET):

- 8:45am: (FR) Feb. CPI EU Harmonized MoM, est. 0.1%, prior 0.1%

- 8:45am: (FR) Feb. CPI EU Harmonized YoY, est. 1.5%, prior 1.5%

- 8:45am: (FR) Feb. CPI MoM, est. 0.0%, prior 0.0%

- 8:45am: (FR) Feb. CPI YoY, est. 1.3%, prior 1.3%

- 8:45am: (FR) Feb. CPI Ex-Tobacco Index, est. 102.68, prior 102.67

- 9am: (SP) Jan. House transactions YoY, prior 3.8%

--With assistance from Joe Easton and Carolynn Look.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.