London Looks Past Brexit to Eclipse Rivals in Emerging Markets

London Looks Past Brexit to Eclipse Rivals in Emerging Markets

(Bloomberg) -- Britain’s decision to break from the European Union five years ago set off alarms that London would lose its pre-eminence as a global financial center. In the world of emerging markets, it appears to have been quite the opposite.

Far from triggering an exodus of business to rival hubs such as Paris and Frankfurt, the Brexit process has coincided with an increase in the buying and selling of currencies and bonds from developing economies through the U.K. capital. Since Britain voted to leave the EU in June 2016, trading in the Chinese yuan, Indian rupee and Russian ruble has ballooned, according to Bank of England data. And it’s a similar story when it comes to sales and listings of emerging-market debt.

“After Brexit, there has been some shift to European capitals but it is not as dramatic as people feared in 2016,” said Simon Harvey, a senior currency analyst in London at Monex Europe, which as a group handles almost $250 billion in foreign exchange each year. “The rise of Dublin and Frankfurt and the threat from rival hubs New York or Tokyo overtaking London as the world’s premier foreign-exchange hub isn’t a major concern.”

In the past five years, London maintained its lead for trading in emerging-market currencies closest to its timezone. Its share of volumes in the Chinese yuan -- the most-traded developing currency by far -- exceeded those for New York, its main rival, by more than four times. The city also topped its game in bonds with Eurobond listings, exceeding an unprecedented $124 billion last year versus $16 billion in 2016, according to data compiled by Bloomberg. Meanwhile, listings in Frankfurt were little changed over that period.

Global banks, asset managers and financial institutions retain a substantial part of their operations in London. That expected larger outflows didn’t happen will provide comfort to a city that accounts for about a quarter of the nation’s economy, and will help affirm Prime Minister Boris Johnson’s post-Brexit project for a “Global Britain.” A reluctance to disrupt well-established ways of doing business remains a powerful motive for them to stay.

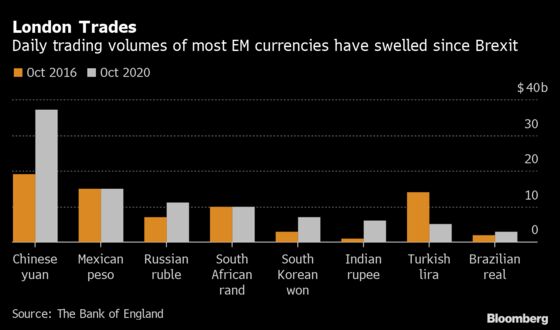

Money Magnet

Even as global banks from Goldman Sachs Group Inc. to JPMorgan Chase & Co. moved jobs and $1.6 trillion of assets to various EU hubs since the June 2016 referendum, developing nations were moving in. Countries including China looked past a fractious parliamentary debate and repeated extensions to transition deadlines to position for a greater presence in post-Brexit London. During a divisive time for Britain, the city was becoming the hub for new global trends such as the internationalization of the yuan to offshore local-currency borrowing by poorer nations.

For the developing world, Brexit may even bring closer trade and financial deals with the U.K. as data show Britain’s exports to outside the EU have performed better than with the 27-nation club. Take currency trading. While London maintained its lead in the currencies of countries in its nearest timezones -- such as Russia’s ruble, Turkey’s lira and South Africa’s rand -- it also grabbed a bigger slice of trading in Indian rupee, Chinese yuan, the South Korean won and the Brazilian real, according to the Bank of England.

“There is a very strong bias” in favor of London, says Luis Costa, a strategist for central and Eastern Europe, the Middle East and Africa at Citigroup Inc. based in London’s Canada Square. “Despite the shock of the changes investors faced on the back of Brexit, it’s extremely difficult to change the dominance of London as a domicile for buy-side firms and, in consequence, for sell-side firms.”

China to the Rescue

Volumes in yuan versus the U.S. dollar doubled to a monthly volume of $818 billion last year from $407 billion in 2016, the Bank of England says in its October survey, or more than quadruple the yuan trading volumes recorded by the Federal Reserve Bank of New York. The next two most popular currencies -- the Mexican peso and the Russian ruble -- also eclipsed transactions in the U.S. hub.

The yuan’s trading volume has even exceeded those of the Swiss franc, Australian and Canadian dollars, the data show.

As the share of developing-nation currencies in the $6.6 trillion-a-day foreign-exchange market increased 25% between 2016 and 2019, the trading activity going through the U.K. accelerated more than its peers, the Bank for International Settlements said in its triennial report on Sept. 16, 2019.

“London was one of the first cities to embrace trading in the renminbi, and it was involved in pretty much every stage of the development of the local debt capital markets in China, and it has been able access the core system and develop channels with all the important counterparts,” said Gustavo Medeiros, deputy head of research at Ashmore Group in London.

Talent Spotting

As well as attracting money, asset managers are hiring for senior emerging-market positions in London. This month, Swiss private bank Union Bancaire Privee has hired Geneva-based Philippe Lespinard for a London-based role that includes overseeing emerging market fixed income. Toronto-based Manulife Financial Corp. promoted Endre Pedersen to the new position of chief investment officer for global emerging-market fixed income in London and HSBC Asset Management expanded its EM desk.

Chicago-based William Blair Investment Management hired Marcelo Assalin -- among 11 fund managers from the Hague-based NN Investment Partners -- to head its London-based EM debt team in 2019. Itau Unibanco Holding SA’s asset-management unit, the second-biggest money manager in Brazil, is considering a portfolio-management hub in London to “connect with people from different places, from Europe to Asia.”

Reality Check

Still, the outflows that London has suffered following Brexit can’t be overlooked. Some GBP2.3 trillion ($3.3 trillion) in the trading of derivatives in euros, pounds and dollars has disappeared after the EU limited access, according to an estimate by Deloitte and IHS Markit Ltd. London trading venues’ share of the euro interest-rate swap market slipped to 10% in January from nearly 40% in July, with business fleeing to both the EU and Wall Street and thousands of jobs at banks and institutions from JPMorgan Chase & Co. to Goldman Sachs Group Inc. The city of Amsterdam, meantime, has toppled London as Europe’s biggest share-trading center.

Then there’s the argument that the benefit London is getting from emerging markets may be only temporary, as the fallout from the Covid-19 pandemic fuels debt sales by developing nations looking to tap demand from yield-starved investors at a time when borrowing costs are at all-time lows.

“Issues such as very low interest rates and a weaker U.S. dollar are forcing people to look at emerging markets for higher yield,” said Niki Beattie, the founder and chief executive officer of Market Structure Partners, a London-based independent adviser on capital-markets structure. “Some people also think we’re in a massive bubble in western markets and emerging markets offer an alternative.”

Another area where action has subsided is the market for initial public offerings. Just one company from the developing economies -- Moscow-based retailer Fix Price Group Ltd -- has sold shares in London this year, compared with as many as eight in 2017, according to data from Dealogic. But that may also have to do with countries nurturing their local stock markets.

Hard-currency bond sales by emerging markets have increased 8% since the start of 2017 versus the preceding period that began in the previous year, according to data compiled by Bloomberg. Of these, transactions in London jumped 38% as listings grew by more than seven times in the four years through 2020.

By contrast, listings in Hong Kong and New York barely changed. Some of the biggest deals were Saudi Aramco’s $8 billion dollar-debt sale on Nov. 17 and $2.5 billion dollar-bond sale by Pakistan on March 30.

Even if its competitors and new emerging market centers take more business from London, there are some advantages the U.K. hub will always enjoy, says Citigroup’s Costa.

“It has to do with credit law, the language, with more flexibility in labor markets compared to Scandinavia, France or Germany,” he said. “I believe over time you will see a bit more dispersion, but because of all this legacy, it is very difficult to imagine London dropping in the rankings.”

©2021 Bloomberg L.P.