Lloyds Tests U.K. Utility Industry Exposure as Corbyn Risk Looms

Lloyds Tests U.K. Utility Industry Exposure as Corbyn Risk Looms

(Bloomberg) -- The last time Labour politicians governed Britain, they took a swathe of the banking industry into public ownership to avoid its collapse. More than a decade later, banks are growing worried about the party’s latest promise to nationalize utility firms -- a policy that could trigger a fresh set of multibillion pound losses.

Lloyds Banking Group Plc, one of the country’s largest business lenders, has multiple exposures to the utility sector through swaps, derivatives and revolving credit facilities, according to people with knowledge of the matter.

While Jeremy Corbyn’s Labour has promised to honor the debts of any businesses it takes into public hands, executives at Lloyds have worked on scenarios under which a future government nationalizes the utilities at less than market value, said the people, who asked not to be named. Representatives at the bank declined to comment.

“Banks have historically seen utility lending as pretty safe,” said Nigel Hawkins, utilities sector analyst at Hardman & Co in London. Utilities have been “pretty good borrowers on the whole and most of them have had very big capital expenditure and had to gear up, which the banks were financing.”

Quantifying the overall risk to the banks in a nationalization is difficult. In the last 10 years, Lloyds, Barclays Plc, HSBC Holdings Plc and Royal Bank of Scotland Group Plc have lent out nearly $50 billion to the British utilities companies, according to data compiled by Bloomberg. However, these loans include some firms that would not be affected by Labour’s policy, while the banks’ swaps and revolving credit facilities would not be included in the public total.

At Lloyds, senior staff have discussed the matter with the relevant companies, while the bank’s non-executive directors have questioned leaders including Chief Executive Officer Antonio Horta-Osorio and Chief Financial Officer George Culmer over the bank’s plans if the government changes, the people said.

“Unprecedented”

The next election isn’t scheduled until 2022, yet the resignation of Theresa May as prime minister last week stirred more uncertainty in the country, which is stuck in a draining Brexit gridlock that could require an election to resolve.

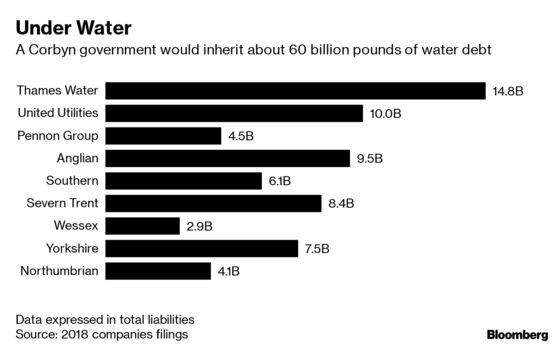

The water companies would be the first to be nationalized under Labour’s plans to take control of utilities, rail and postal services. The opposition party has said it would compensate equity investors with bonds issued by the U.K. Treasury at a value decided by the Parliament. However, there is little clarity on the consequences for lenders who finance those firms, with Labour vowing to refinance “over a period of time so that the costs of debts are reduced.”

Having Parliament decide the fair value of utility firms would create “a lot of uncertainty for investors. There could be a big discussion about what fair value means,” said Andrew Rose, chief executive of the Global Infrastructure Investor Association, a trade body. “It’s an issue for the owners but also for the reputation of the U.K. government. There is a lot of domestic and international capital sitting there.”

“Labour have been clear that existing debts of the operating companies will be carried over and honored in full,” said a spokesman for John McDonnell, the party’s shadow chancellor.

Utility providers use several methods to tap markets for their large maintenance and upgrade costs. As well as issuing shares and bonds, these firms agree revolving credit facilities to help manage their cash needs. Much of their funding would be almost entirely private and through swaps, one person said.

“It would be extreme and unprecedented for the British government to cause a default on those swaps and incredibly damaging for the U.K. as whole,’’ Dan Neidle, partner at Clifford Chance LLP, said in an interview.

In its annual report, Thames Water, the U.K.’s largest water company, said it has derivative financial instruments worth a nominal 5.5 billion pounds ($7 billion) in 2018, resulting in a net liability of 762 million pounds. In a sign that its lenders are increasingly worried about nationalization, Thames added a clause to its bonds to guarantee holders would be repaid immediately if the government takes over, Reuters reported in April. A spokesman at Thames Water declined to comment.

Still Safe?

Nationalizing these firms would not be cheap. The Centre for Policy Studies, a research group set up by the former Conservative Prime Minister Margaret Thatcher, last year gave an estimated cost of 55.4 billion pounds to buy National Grid Plc and other energy distribution networks -- as Labour have pledged -- with the total rising to 185 billion pounds to take over the entire energy industry, including the Big Six companies that both produce power and sell it to consumers. It said buying the water industry would cost anywhere from 14.3 billion pounds to 100 billion pounds.

A Labour government would have wider implications for the British banks. Corbyn, who took over as a leader in 2015, has pledged to “transform” the financial system with reforms including “a new approach” to state-controlled RBS that could see it broken up into new local public banks, according to the 2017 election manifesto. However, a shadow minister told Reuters earlier this year any state involvement in the bank would depend on its willingness to increase lending to Britain’s regions and small businesses.

During a meeting between RBS’s top executives and Labour Party representatives last year, the bank’s officials made the point that RBS is the country’s biggest lender to small- and medium-sized businesses and that breaking up a bank has costs, according to one person who attended the meeting. A spokesman for RBS declined to comment.

“There are a lot of headwinds for the U.K. banks. Chances for them to come up with good news are very low,” said Eric Moore, a fund manager at Miton Group in London who owns shares of U.K. lenders including Lloyds. “Under a Corbyn government, you can not rely on market value. It’s going to be very challenging for banks to quantify their risk.”

--With assistance from Jeremy Hodges.

To contact the reporters on this story: Stefania Spezzati in London at sspezzati@bloomberg.net;Harry Wilson in London at hwilson57@bloomberg.net

To contact the editors responsible for this story: Ambereen Choudhury at achoudhury@bloomberg.net, Marion Dakers

©2019 Bloomberg L.P.