(Bloomberg Opinion) -- Lloyd Blankfein, the former head of legendary Wall Street firm Goldman Sachs Group Inc., took to Twitter on Thursday with an observation that at first seemed innocuous but in reality was terrifying. Blankfein tweeted to his more than 140,000 followers that when it comes to finance, what is “most surprising to me” is that investors worldwide continue to lend “a virtually limitless” sum of money to the U.S. at record-low interest rates “despite the trillions” of dollars it’s adding to the budget deficit and national debt.

Given his long career in markets, it’s highly unlikely Blankfein is actually surprised. As my Bloomberg Opinion colleague Karl W. Smith outlined earlier in the day, despite estimates the U.S. budget deficit will quadruple this year to almost $4 trillion and with the national debt having swelled by $1.4 trillion this year already, there is no looming debt crisis. The primary reason is that the dollar is by far the world’s primary reserve currency, with the greenback accounting for 60.9% of global currency reserves, dwarfing the euro’s 20.5%, International Monetary Fund data show. This “exorbitant privilege” means everyone must own dollars, allowing the U.S. to borrow at rates much lower than they might otherwise be given the deteriorating fiscal position. For proof, look no further than the Bloomberg Dollar Spot Index’s 6.44% gain this year, already making 2020 the best for the currency since 2015 with April not yet over. The benefits of a strengthening currency go a long ways toward overcoming the sting of low rates for international investors.

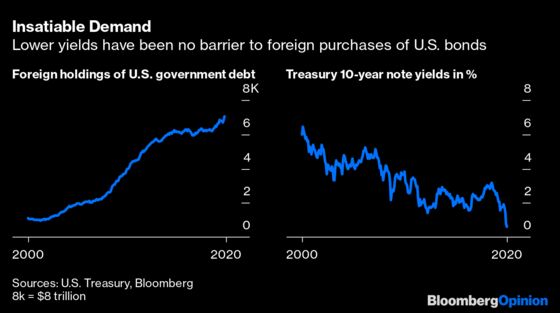

The latest Treasury Department data show that foreign investors scooped up $374.4 billion of U.S. government debt in the first two months of the year. That was by far the most of any two-month period in history, bringing their holdings to $7.07 trillion as fears about the coronavirus began to spread. But, again, Blankfein surely knows all this. He also knows that history shows nothing lasts forever. The British pound was the world’s primary reserve currency for a century and a half before ceding the crown to the dollar in the mid-1900s. This is why Blankfein’s tweet should be seen as more of a warning to U.S. officials to come up with a plan to eventually reverse its growing debt and deficits. Because if the day ever comes when the U.S. can no longer finance its deficits with the help of foreign investors, get ready for extreme turmoil in global financial markets.

STOCKS REBOUND IS MISSING A KEY INGREDIENT

Nobody truly knows what to make of the rebound in stocks over the last month, with the S&P 500 Index up some 25% since plunging on March 23 to its lowest since 2016. Is it a reflection of confidence that the quick responses by the government and Federal Reserve to cushion the economy will prove successful? Or is it just a “dead cat bounce” that soon reverses as stocks tumble to new lows while the U.S. struggles with a deep recession, or even depression? If you believe in the old saying that you can’t have a healthy economy without a healthy banking system, then the truth leans toward the latter scenario. The good news is that the banking sector entered this crisis in good shape, thanks to reforms put in place after the financial crisis just more than a decade ago. Fed data show that deposits at U.S. banking institutions entered 2020 with deposits exceeding loans by about $3 trillion, up from about $250 billion in 2008. The bad news is that banking stocks are acting like this recession will be severe enough to threaten that cushion. In fact, bank stocks are underperforming the broader market by the most since early 2009, according to Bloomberg News’s Andrew Cinko. That’s hardly a vote of confidence in equities.

WOE CANADA

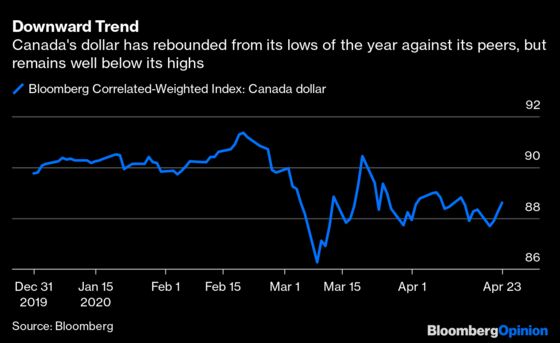

The ranks of major economies with AAA credit ratings from S&P Global Ratings, Moody’s Investors Service and Fitch Ratings has rapidly shrunk since the financial crisis as government ramped up borrowing to support their economies. Not even the U.S. is a member of that club, having been downgraded to AA+ by S&P. Data compiled by Bloomberg show that only nine countries have the highest ratings from all three firms: Germany, the Netherlands, Denmark, Norway, Singapore, Sweden, Switzerland, Australia and Canada. And this select group may be poised to shrink even further. Speculation is growing that Canada may be the next to get downgraded as the oil crash and recession force the country to borrow to support is provinces, according to Bloomberg News’s Esteban Duarte. Going into the pandemic, Canada’s provincial governments had C$853 billion ($602 billion) of debt securities outstanding, more than the national government. They also shoulder most of the cost for health care and education. Several of them rely on energy revenues that are evaporating, with oil-rich Alberta releasing a budget in February based on West Texas Intermediate prices at $58 a barrel. “There is a very good chance that the need for more massive federal assistance for the provinces, for households, for the business sector, will trigger a downgrade at some point” for Canada, said David Rosenberg, founder of Rosenberg Research and Associates. If true, then the Canadian dollar could come under severe pressure.

FOOD WORRIES ARE STARTING TO GROW

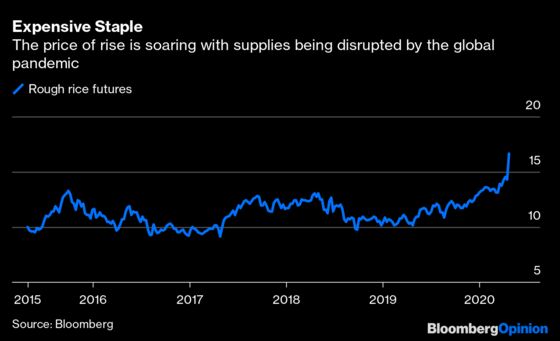

Rice is known as the most important food in the world, directly feeding more people than any other crop, including almost half of world’s population. So, it’s concerning to see the cost of rice start to shoot higher, reaching the highest since 2008 on Thursday. Much of this, like most everything else these days, is tied to the pandemic and growing anxiety about disruptions to the global supply of food. In Vietnam, which is the world’s third-biggest rice exporter, the government last month decided to restrict shipments on concerns that global demand will spike as the coronavirus upends supply chains. As a result, hundreds of thousands of tons of rice is spoiling at the country’s ports, Bloomberg News reports. In India, labor shortages due to the lockdown there may push farmers in the nation’s second-biggest rice growing region to switch to cotton, according to Bloomberg News. Beyond the potential for a supply disruption, there’s another brewing problem with rice, and that is the potential for the staple to become less nutritious as carbon dioxide levels increase worldwide, according to a study in the publication Science Advances. "Declines of protein and minerals essential for humans, including iron and zinc, have been reported for crops in response to rising atmospheric carbon dioxide concentration," according to an abstract of the study.

TEA LEAVES

Every Friday afternoon in the U.S., just after markets close, the Fed releases data on various bank metrics. This report has taken on greater importance as more and more companies have tapped their credit lines and loaded up on cash to help offset the loss of revenue from the coronavirus pandemic. This dash for cash has been swift and severe. Commercial and industrial loans outstanding have surged by about $510 billion, or 22%, since early March to $2.87 trillion. To put that increase in perspective, consider that the previous record increase for a full year was just $235.1 billion in 2007. The old saying goes that banks only want to lend money when people don’t need it. But now, everybody needs money, and that can’t be good for banks.

DON’T MISS

U.S. Government Is Not Facing a Looming Debt Crisis: Karl Smith

Emerging Markets May Lead the Coronavirus Rebound: John Authers

Think Oil Price Volatility Is Over? Think Again: David Fickling

Fed Denies Active Bond Managers a Star Turn: Nir Kaissar

Diamonds Need Some New Best Friends: Clara Ferreira Marques

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the Executive Editor for Bloomberg Opinion. He is the former global Executive Editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2020 Bloomberg L.P.