Lifelines Fray for Companies Close to Brink Before Meltdown

Lifelines Fray for Companies That Were on Brink Before Meltdown

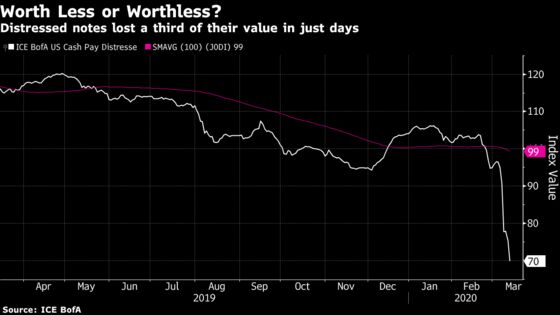

(Bloomberg) -- As credit markets around the world sputter and seize, distressed companies are watching financial lifelines that they were counting upon slip from their grasp.

Rescue deals have been scrapped and restructuring plans shredded as prospective lenders, partners and buyers adjust to a world suddenly dominated by talk of global recession, radically lower valuations and credit markets that treat deeply troubled companies as almost untouchable.

“We could have had meetings two weeks ago with clients telling them the types of financing options that were available. Many of those options are gone now,” said Steve Zelin, the head of the restructuring group at PJT Partners Inc.

Some companies contending with broken deals or a need to restructure have been quick to blame the coronavirus disruption as a central cause. Bankrupt shale oil driller Alta Mesa Resources Corp. on Thursday said the firm that promised to buy some of its assets pulled out of that deal at the eleventh hour, citing the “perfect storm of factors” posed by the pandemic and the oil collapse.

Others seized on the epidemic even though they had been in fundamental trouble for months or years, such as newly bankrupt Pier 1 Imports Inc. and coal miner Foresight Energy LP.

In some cases, companies haven’t been explicit about the demise of their plans, but there’s little doubt about why their deals had to be pulled. Canned food purveyor Del Monte Foods Inc. on Thursday postponed a $575 million debt deal crucial to its turnaround plan, without commenting on the cause.

A handful of other junk-rated issuers have pulled debt deals from the market so far this month, and investors will be watching next week to see if the turmoil affects the biggest restructuring target Frontier Communications Corp., which has been talking with creditors about a bankruptcy plan. Investors will also be watching to see whether deeply distressed energy companies such as Whiting Petroleum Corp. and California Resources Corp. can salvage themselves; both have interest payments coming due on March 15, and the latter has a debt swap expiring three days later.

“For oil and gas companies that are restructuring, the drop in oil prices, if sustained, changes everything,” said Mo Meghji, the founder of restructuring advisory firm M-III Partners. “They will have to start over and recalculate the assumptions and financial projections in their plans.”

When oil crashed in 2015 and early 2016, most companies were able to get their unsecured bondholders to swap their debt for new, longer-dated secured notes in order to stay afloat. But many of those securities started defaulting last year, leading to a surge in bankruptcies.

Price War

The shock is especially severe for energy producers as the pandemic coincides with production ramp-ups in Russia and Saudi Arabia that spurred a plunge in oil prices.

Derek Pitts, head of restructuring at investment bank PJ Solomon, said potential lenders are asking a host of new questions in light of the growing market concerns.

“There’s a number of deals in the pipeline that you worry about because we don’t know how they are going to shake out,” Pitts said. Still, he’s fielded calls from various capital sources who are “actively looking to provide financing to bridge this period of uncertainty.”

Behind the reluctance on the part of buyers and lenders is a desire to keep their options open, said Colin Adams, a managing director at M-III. “The whole story this week is about maintaining and preserving liquidity,” Adams said, and in transactions, as in trading, “bids are scarce.”

Who’s Next?

As they busy themselves seeking backup plans or bankruptcy preparation for clients losing funding, restructuring bankers and advisers are also anticipating a flood of work from healthier companies thrust into distress by the market crack.

“Companies that never considered themselves to be an at-risk credit have woken up three days later and said, okay, this is a whole new landscape,” said Andrew Yearley, managing director in the restructuring group at Lazard Ltd.

“No one can predict when the market will open again, and when it does, where and how risk will be priced,” Yearley said. “All bets are off right now.”

To contact the reporters on this story: Eliza Ronalds-Hannon in New York at eronaldshann@bloomberg.net;Katherine Doherty in New York at kdoherty23@bloomberg.net

To contact the editors responsible for this story: Rick Green at rgreen18@bloomberg.net, Dawn McCarty

©2020 Bloomberg L.P.