Libor Transition Gets Unforeseen Gift From Repo-Market Turmoil

Libor Transition Gets Unforeseen Gift From Repo-Market Turmoil

(Bloomberg) -- As last month’s funding-market turbulence spurs questions about the viability of the Secured Overnight Financing Rate, a silver lining is emerging for the Federal Reserve’s preferred replacement for dollar Libor.

SOFR more than doubled to a record 5.25% on Sept. 17, as cash reserves in the market for repurchase agreements that underlie the benchmark got out of alignment with the volume of securities on dealer balance sheets. While the volatility hardly inspired confidence among end-users, the greater risk of shocks inherent to the reference rate is fueling a flurry of trading in nascent swaps and futures tied to the benchmark as investors hedge their exposure.

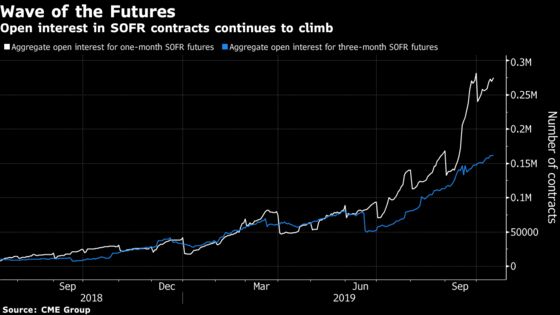

That pickup in activity is good news for the Alternative Reference Rates Committee -- convened by the Fed to spearhead the Libor transition in the U.S. One of the biggest obstacles to broader SOFR adoption cited by market participants has been the lack of a term structure associated with the benchmark. Greater turnover in monthly and quarterly futures introduced last year should facilitate the creation of additional tenors, eventually producing a curve that reflects expectations for where the rate will be in the future.

“As people get familiar and start thinking in terms of SOFR, they’ll start wondering how to protect themselves from interest-rate movements,” said Joseph Abate, a money-market strategist at Barclays Plc in New York.

Aggregate open interest in SOFR futures climbed from 255,000 contracts at the beginning of September to 429,000 contracts at the end of the month, representing more than $1.5 trillion in notional value.

In another potential boost for SOFR, the Federal Housing Finance Agency, which regulates the Federal Home Loan Banks, late last month said that after the first quarter of 2020, the entities shouldn’t issue new financial instruments tied to the London interbank offered rate that mature after December 2021. That’s when regulators in the U.K. will stop compelling banks to submit quotes that inform the beleaguered benchmark.

The Home Loan Banks have more than $221 billion of notes tied to Libor outstanding, and much of that volume is seen shifting to SOFR as a result.

“The FHFA letter could be the first in a series of regulatory actions aimed a speeding the adoption of SOFR,” TD Securities strategists Gennadiy Goldberg and Priya Misra wrote in an Oct. 4 note to clients.

Still, SOFR’s single-day, 282-basis-point surge last month is giving many in the market pause, even as regulators push for quicker adoption.

“When there’s volatility in the rate like this, it doesn’t bode well for confidence in the new reference rate,” said Tom Hunt, the director of Treasury services at the Association for Financial Professionals. “People rightfully have a lot of concerns.”

Tom Wipf, chairman of the ARRC, said in a note to members the day after the benchmark’s surge that its average rate remained stable, and that the committee has always understood that daily rates are volatile, while noting that the increase in the three-month compounded average of SOFR was minimal compared to Libor.

Other catalysts that may spur a pickup in trading of derivatives tied to SOFR include the debut of options trading on futures in January and the potential introduction of a backward-looking term rate by the New York Fed.

The International Swaps and Derivatives Association’s publication of a protocol for users to supplement existing contracts as part of the shift from Libor and the so-called big bang transition to SOFR price alignment and discounting for the swaps market by CME Group Inc. and LCH Ltd. may also fuel greater volume.

“The use of SOFR is a work in progress,” Abate said. “We’ve been watching it. People have historical data. People are trying to get familiar with the rate.”

To contact the reporters on this story: Alexandra Harris in New York at aharris48@bloomberg.net;Allan Lopez in New York at alopez11@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, ;Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Boris Korby, Nick Baker

©2019 Bloomberg L.P.