Li Ka-shing’s Husky Bet Has Lost Over 80% In a Decade

Li Ka-shing’s Husky Bet Has Lost Over 80% In a Decade

(Bloomberg) -- Hong Kong billionaire Li Ka-shing’s oil sands investment is hurting -- and some analysts are calling on him to stop the bleeding.

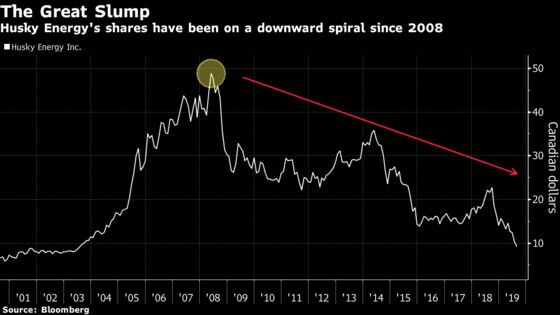

Shares of Calgary-based Husky Energy Inc. have plummeted over 80% since its 2008 peak on a myriad of reasons: a slump in oil prices, a dividend suspension, a production cut due to a close call with an iceberg and a failed C$2.75 billion hostile takeover bid for MEG Energy Corp.

That has led to the majority stake owned by Li losing C$26.5 billion ($20 billion) in value, according to data compiled by Bloomberg. Li and Hutchison Whampoa, now owned by CK Hutchison Holdings Ltd., became Husky’s majority shareholders in 1991, according to Husky Energy’s website. He retired as head of CK Hutchison and CK Asset Holdings Ltd. last year and handed over the reins to his eldest son Victor Li.

The slump in the company’s share price has drawn RBC Capital Markets analysts led by Greg Pardy to contemplate whether the company should consider going private to capture the gap between its market value and its underlying value, and so it can make the right moves without market scrutiny.

“If ever there was a time for Husky to consider going private, we believe it is now,” Pardy said in a research report published Monday.

Easy Task?

While the possibility of taking Husky private, which is about 69%-owned by Li, would make sense, Husky’s lower free cash flow level compared with its peers may not make this a simple task, according to Canoe Financial’s senior portfolio manager Rafi Tahmazian. He added that Asian mogul Li would have to fork out cash over the next few years to meet capital commitments should he decide to take the company private.

Husky is a part of the growing list of energy companies that analysts are pitching the idea of going private. Citigroup Inc. said last month that pipeline owner SemGroup Corp. should considering going private because it’s undervalued and may need a few years to address investors’ concerns. In late June, Seaport Global Securities LLC said shale driller Continental Resources Inc. could be a go-private candidate because its management feels like public markets aren’t rewarding “positive behavior in the E&P space.”

Husky’s integrated operations including refining makes the company more resilient to commodity price differential movements and Tahmazian doesn’t see the idea of Husky going private being specific to the company’s woes.

“It is the sign of the times that we see these suggestions,” he said.

--With assistance from Pei Yi Mak and Kevin Orland.

To contact the reporter on this story: Michael Bellusci in Toronto at mbellusci2@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Divya Balji, Cormac Mullen

©2019 Bloomberg L.P.