Leveraged-Loan Buyers Clamor for Crumbs in Hot Market

Leveraged-Loan Buyers Clamor for Crumbs as Market Heats Back Up

(Bloomberg) -- When a Credit Suisse Group AG salesman asked investors for their final orders for pieces of a corporate loan this week, his email included an unusual visual goad: a photograph of a few crumbs of cake left on an otherwise empty plate.

The bank received so much demand for the $5.05 billion loan, which is helping to finance KKR & Co.’s leveraged buyout of Envision Healthcare Corp., that it increased the final size by $400 million and is closing down the sales process a week early, according to people with knowledge of the matter. The offering followed two other big loan sales, for Thomson Reuters Corp.’s financial terminal business and for Akzo Nobel’s chemicals unit.

The success of those three debt deals signals that after money managers were able to push back on riskier loans and bonds starting in June, issuers are gaining the upper hand again. The extra yield that loans pay relative to benchmarks could fall going into the end of the year, and protections for investors may weaken, said Lauren Basmadjian, senior portfolio manager at Octagon Credit Investors.

"We’re heating up again," said Basmadjian, whose firm manages more than $20 billion. “In a few weeks, the market could get even hotter."

The image of the cake was included in an email that Credit Suisse circulated this week, according to people who saw it. A spokeswoman for the bank declined to comment.

The demand comes in part from the Federal Reserve’s efforts to bring borrowing costs to more normal levels after cutting them to zero amid the financial crisis. The Fed on Wednesday hiked rates another quarter of a percentage point to their highest level in a decade, the eighth increase since late 2015, and said it expects three hikes next year. Loans, which pay floating rates, allow investors to earn higher yields as the Fed tightens.

High demand from investors for loans is being met by relatively low supply in the more than $1 trillion market. There haven’t been enough leveraged buyouts to keep issuance as high as it’s been. New leveraged loan sales to institutional investors are on track to be around $80 billion in the third quarter, down from $99.5 billion in the second quarter, according to data compiled by Bloomberg.

Read more in the credit brief: Comcast to enter $100 billion debt club

Dealers don’t seem to anticipate that issuance will rise. One Wall Street syndicate desk is forecasting $30 billion or less of loan sales, another said $45 billion to $55 billion, and a third said $70 billion to $80 billion.

That demand has helped push loan yields lower than they would have been otherwise, averaging 6.81 percent on Thursday, according to JPMorgan’s Leveraged Loan index. In early July, it was 6.85 percent. Three-month Libor has risen over that period.

Top Gainers

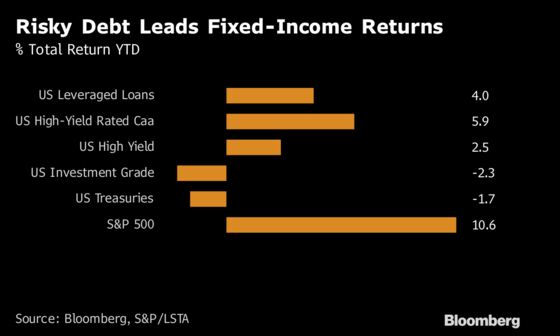

Leveraged loans and bonds from the riskiest junk companies are among the best returning U.S. fixed-income assets in 2018. In a year where Treasuries have lost about 1.7 percent and investment-grade corporate bonds have given up about 2.3 percent, leveraged loans are ahead by around 4 percent, and high-yield bonds in the CCC tier have gained 5.9 percent.

“The leveraged-loan market is nothing earth-shattering in terms of returns,” said Craig Russ, a portfolio manager at Eaton Vance Management. “But it looks better than the rest of the fixed-income market.”

If strong demand allows companies to take on more debt and weaken investor protections, it will represent an about-face for a market that since June has been becoming more disciplined. Moody’s Investors Service said North America bond covenants broadly improved in August from July, to their best level since May 2017.

But the three big loan deals that have priced in September have had weaker terms. KKR’s loan for the Envision buyout featured provisions allowing it to sell a unit and pay itself dividends. In the debt for its acquisition of a majority stake in Thomson Reuters’ financial terminal business, which will be renamed Refinitiv, Blackstone pioneered terms that allow it to take dividends out of the company. It can do so even if the business fails basic tests of earnings strength relative to interest expense. Moody’s gave the unsecured bond’s covenants its weakest possible score.

"This may be one of the most drastic covenant changes we have seen in years," Scott Josefsberg, an analyst at Covenant Review, wrote in a report this week.

With demand outstripping supply, more of these kinds of changes may be on the way, said Krishna Memani, chief investment officer at OppenheimerFunds Inc.

“If you think this is bad, it can certainly get worse,” Memani said.

--With assistance from Lara Wieczezynski and Molly Smith.

To contact the reporters on this story: Lisa Lee in New York at llee299@bloomberg.net;Davide Scigliuzzo in New York at dscigliuzzo2@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, Dan Wilchins

©2018 Bloomberg L.P.