Hezbollah Scolds Banks in Lebanon's Latest Brush With Crisis

Lebanon's Latest Brush With Crisis Has Hezbollah Scolding Banks

(Bloomberg) -- From retired soldiers fighting for their pensions to striking central bank staff, few in Lebanon feel they’ll be spared what the government is touting as the most austere budget in their country’s history.

One of the world’s most indebted nations has little time to spare after decades of fiscal overreach and mismanagement of public finances. But the cabinet is only expected to approve a much delayed budget on Monday, according to Industry Minister Wael Abu Faour, the same day that a $650 million Eurobond matures and more than three months after a new government was formed.

As the clock ticks down, widespread public pushback shows that fixing state finances will come at a steep political cost -- and risk further unsettling investors whose support Lebanon will need to repay the debt coming due this month and later this year. Also at stake is $11 billion in funding pledged by international donors who are waiting for evidence that Lebanon is committed to reducing the deficit and combating corruption.

“There is a deep disagreement today on who bears the cost of the austerity,” said Ayham Kamel, head of Middle East and North Africa research at Eurasia Group. “Is it the financial sector, the government and the public sector, or politicians and their related enterprises?”

In the streets and on television, a national obsession with politics has given way to talk of “economic collapse” and panic over looming reforms. With the country swept up in nationwide protests, even the head of Hezbollah -- whose talking points usually include missiles and martyrs -- made an unusual appeal to local lenders to assist the government by lowering the cost of debt servicing.

Meanwhile, inflows of bank deposits, a critical source of hard currency, are largely flat this year, and the central bank’s foreign-exchange assets are shrinking.

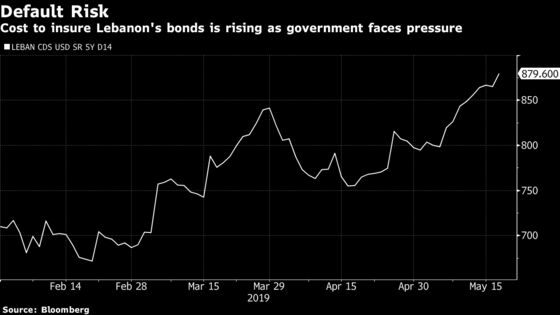

The market’s verdict on Lebanon’s latest drama has been swift. Its five-year credit-default swaps have climbed around 200 basis points since late February, while the yield on Lebanon’s dollar bonds due 2028 is at the highest since January. Option-adjusted spreads on Lebanese bonds over U.S. Treasuries widened the most in emerging markets last week.

“Demonstrations and strikes against proposed austerity measures being considered in the budget have highlighted the difficulties the government is facing in advancing its economic agenda,” Goldman Sachs Group Inc. economists Kevin Daly and Clemens Grafe said in a report. “The critical question is whether progress on reform is enough to alleviate near-term external financing pressures, which are the most immediate threat facing Lebanon today.”

Deficit, Debt

Prime Minister Saad Hariri’s government is seeking to cut nearly 1.2 trillion pounds ($800 million) in spending to reduce a budget deficit that reached 11% of gross domestic product last year. Lebanon’s public debt, estimated at over 160% of GDP this year, is projected to rise to near 180% by 2023, second only to Japan’s, according to the International Monetary Fund.

In their discussions over the past two weeks, ministers approved a series of measures to increase revenue, including raising a levy on interest from deposits to 10% despite repeated objections from local lenders. Other measures range from a higher fine for tax evasion to cuts in state contributions to organizations and health-care benefits to state employees. Also in the draft budget; a plan to cap public sector salaries.

Blame Game

Examples of government waste abound in Lebanon. Although its railroad has been largely out of service since the start of a 15-year civil war in the 1970s, there’s still a handful of paid employees working for the railway authority.

No recent decision looms larger than the government’s 2017 approval of a public-sector wage hike, estimated to have cost $2 billion, in the face of repeated warnings about its fiscal implications. Despite talk of a freeze on hiring in the public sector, hundreds and possibly thousands of jobs were handed out in ministries and other state institutions in the run-up to last year’s elections.

Those employees say however, that it is not their paltry pay checks but corruption in the ruling political class that is threatening to bankrupt the country.

“You want us to believe that our salaries broke the treasury?” said a 59-year-old transport worker who didn’t want to give his name. The person earns $1,000 a month and gets a bonus equivalent to another two months of wages. “Let them hold themselves accountable first.”

Wrecked the Boat

The 2017 wage hike strengthened purchasing power at a time when remittances had slowed and the war in Syria was taking its toll, leading to a historic deficit in the balance of payments. But it is the broader inability of fractious politicians to make the necessary reforms before the country reached the brink, that has shaken public confidence.

That is making it harder for government officials to sell the budget to ordinary Lebanese who say they are not the ones who should be paying the price.

“How can they trust those who wrecked the boat to save it?” said Sami Nader, head of the Beirut-based Levant Institute.

To contact the reporter on this story: Dana Khraiche in Beirut at dkhraiche@bloomberg.net

To contact the editors responsible for this story: Lin Noueihed at lnoueihed@bloomberg.net, Paul Abelsky

©2019 Bloomberg L.P.