Freeze Order on Lebanese Banks Lifted After Less Than 24 Hours

Lebanon Prosecutor Freezes Assets of 20 Banks and Their Chairmen

(Bloomberg) --

The showdown between the Lebanese government and local banks took a new twist when a freeze order on 20 lenders was lifted just hours after it was first imposed.

On Thursday, the financial prosecutor locked down the banks’ assets as well as those of their chairmen amid an investigation into the illegal transfer of billions of dollars and the recent sale of Eurobonds to foreign funds. But by the end of the day, the state prosecutor, Ghassan Oueidat, had suspended the move, pending further investigation.

The week began with financial prosecutor Ali Ibrahim questioning 14 bankers on the transfer of $2.3 billion overseas during October and November. Among the banks targeted are Lebanon’s biggest lenders, including Bank Audi, Fransabank, Blom Bank and the Lebanese unit of Societe General. The prosecutor also questioned the head of the Association of Banks in Lebanon, Salim Sfeir, who is also chairman of Bank of Beirut. The decision still required the approval of central bank Governor Riad Salameh, according to a judiciary official, who declined to be identified.

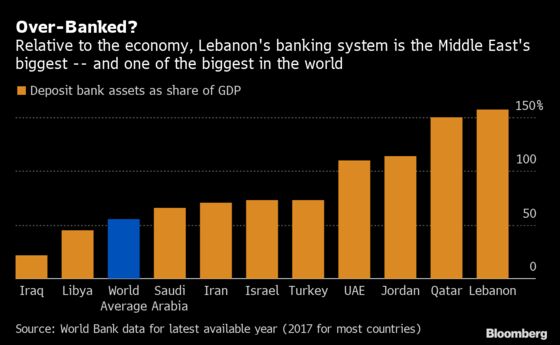

Once central to how the government managed public finances, Lebanon’s banks are now the focus of its ire as the clock runs down to the March 9 deadline for repaying $1.2 billion in Eurobonds.

As the biggest holders of Lebanon’s sovereign debt, banks have been increasingly at odds with the government over the looming repayment. While top officials have argued that the only solution to the country’s debt burden is a restructuring, lenders have come up with alternative options since they stand to lose in the event of a default.

Offloading Debt

The prosecutor questioned the bankers on the recent sale of Eurobonds to foreign funds that the judiciary says disrupted the government’s efforts to restructure its debt. The debt sales mean that foreign creditors now hold a larger proportion of the Eurobond series maturing in 2020, giving them more leverage in any restructuring discussion.

Bankers contend that they sold the notes to get their hands on foreign currency amid a shortage of dollar liquidity in the country. Sfeir said in an interview that banks needed cash to pay outstanding liabilities of almost $9 billion and meet demand for fuel, wheat and medicine suppliers.

Nationwide protests that began in October helped touch off Lebanon’s worst financial crisis in decades, forcing the closure of lenders for nearly two weeks. Some officials have accused bankers of transferring funds belonging to politicians and high-net-worth individuals abroad while informal capital controls were in place.

Banks restricted the movement of capital since the start of anti-government demonstrations, limiting withdrawals and nearly banning transfers abroad. The central bank has also been rationing foreign currency as remittances -- once the country’s main source of financing -- have slowly dried up.

The measures led to the emergence of a black market rate for the local currency much higher than the official peg.

Protesters have frequently turned their anger against the banks, since many people are only able to withdraw as little as $200 a week. They have also trashed bank branches and engaged in violent altercations with employees.

--With assistance from Netty Ismail and Alex Nicholson.

To contact the reporter on this story: Dana Khraiche in Beirut at dkhraiche@bloomberg.net

To contact the editors responsible for this story: Nayla Razzouk at nrazzouk2@bloomberg.net, Paul Abelsky, Mark Williams

©2020 Bloomberg L.P.