Lebanon's Bonds Enter Danger Zone as Budget Crisis Drags On

Lebanon Eurobonds Enter Danger Zone as Fiscal Crisis Drags On

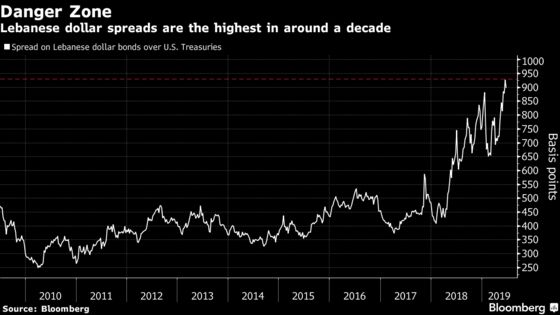

(Bloomberg) -- Lebanon’s Eurobonds have entered distressed territory as a budget delay and rising political tension in the region complicate efforts to tackle the nation’s fiscal crisis.

The average extra yield investors demand to hold the Arab nation’s debt over U.S. Treasuries climbed to a 10-year high of 946 basis points this week. Among emerging markets not in default, only Zambia and Argentina have wider spreads, according to a Bloomberg Barclays index.

Some of Lebanon’s dollar securities, including those maturing in 2022 and 2023, already have spreads above 1,000 basis points.

Investors are losing patience as political squabbles stall economic reforms. A long-delayed budget aims to lower the deficit to 7.6% of gross domestic product this year, which would help unlock billions of dollars in aid. Prime Minister Saad Hariri said last week that lawmakers objected to some items after previously agreeing to them, and he ridiculed suggestions that Lebanon would seek a bailout from the International Monetary Fund.

“The country is running out of time,” said Raffaele Bertoni, the head of debt-capital markets at Gulf Investment Corp. in Kuwait City. “Unpopular decisions are needed to keep the growing fiscal deficit under control. Until then, Lebanese sovereign bonds will continue to trade in distressed territory.”

Inverted Curve

Another sign of stress is the partial inversion in Lebanon’s Eurobond curve, with some shorter-dated notes yielding more than those with longer maturities. That often occurs when countries are near or in default, such as with Venezuela.

The IMF estimates Lebanon’s public debt at about 160% of GDP, one of the highest levels in the world. Lebanon has never defaulted on its debt, which was mostly accumulated after the 1975-1990 civil war.

Nassib Ghobril, the chief economist at Beirut-based Byblos Bank SAL, said Lebanese Eurobonds are stable. Local institutions hold 86% of the nation’s total debt and most of it is denominated in local currency, he said.

Some strategists also say the bonds are too cheap to ignore. Morgan Stanley’s Jaiparan Khurana, who’s based in London, said yields on longer-dated securities have risen to attractive levels. There’s been a “modest improvement” in banking-sector liquidity and reserves are falling more slowly than last year, he said in a note.

Political Tension

Still, Lebanese notes have lost investors 1.3% on average this month, the worst performance after Suriname in the Bloomberg Barclays EM USD Sovereign Bond Index, which includes 75 countries.

The escalation of regional tensions is making investors more concerned, said Carla Slim, Standard Chartered Plc’s Dubai-based economist. Two oil tankers were attacked last week near the Strait of Hormuz, an incident that the U.S. and Saudi Arabia have blamed on Iran.

Iran provides financial support to Hezbollah, a Lebanese militant group designated by the U.S. and U.K. as a terrorist organization. Saudi Arabia backs the Sunni political party headed by Hariri.

As the U.S. ratchets up pressure on Iran, the risk premium on Lebanese debt rises, said Slim.

Budget Implementation

Investors’ main focus now is on whether the government can fix its finances.

“While Lebanon will probably be able to muddle through this year, the key downside risk lies in restoring confidence at both the depositor and investor level,” said Slim, who forecasts a fiscal deficit of 9.5% for this year.

The budget proposes sharp cuts in spending, higher income taxes and a halt in public-sector hiring. It still needs to be passed by parliament, where it may find fierce resistance from lawmakers.

“No party seems willing to cede any of their privileges,” said Alia Moubayed, a researcher in London with Jefferies International Ltd. “The faster the credibility of policy and policymakers erodes, the higher the risk premia and the greater the need for an externally sponsored arrangement that brings discipline and predictability to policy implementation.”

To contact the reporters on this story: Abeer Abu Omar in Dubai at aabuomar@bloomberg.net;Paul Wallace in Lagos at pwallace25@bloomberg.net

To contact the editors responsible for this story: Justin Carrigan at jcarrigan@bloomberg.net, Dana El Baltaji

©2019 Bloomberg L.P.