Late to Fintech Boom, Nigerian Banks Turn to Regulators for Help

Late to Fintech Boom, Nigerian Banks Turn to Regulators for Help

Nigerian banks’ dominance of their home turf is virtually unparalleled.

Largely protected by regulators from foreign competition, Nigerian lenders control 94% of their domestic market, by assets, the world’s largest share of local ownership after Israel, according to a report published before Covid-19 hit in 2020 by Chris Ogbechie and Lilac Nachum, scholars at Lagos Business School.

But the threat is now homegrown. Nigerian banks are only now starting to counter the emerging financial-technology firms riding the online wave spurred by the pandemic. As they set out their mobile-money ambitions, they’re deploying their political muscle with regulators to bolster the moat around their franchises.

“Some might claim there is pushback from traditional banks and their regulatory ally to restrict financial innovation by fintechs,” says Abubakar Idris, analyst at Stears Business, a Lagos-based consultancy for financial and technology companies. “If the largest telcos get a banking license, they could undercut the banks.”

The simmering conflict broke into the open this month when lenders kicked MTN Group, Africa’s largest mobile-phone company, off of their shared platform, protesting a cut by the telecom provider on commissions charged on banking channels by almost half to 2.5%. Regulators intervened to reconnect MTN customers, while reinstating the 4.5% commission for the purchase of airtime bought via the banks.

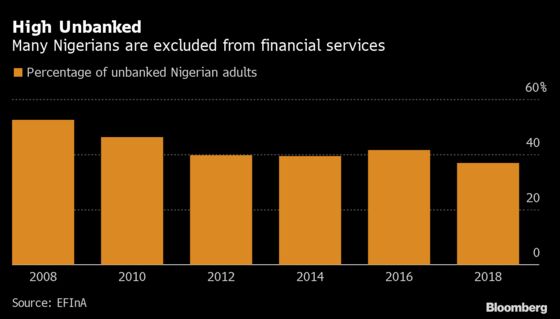

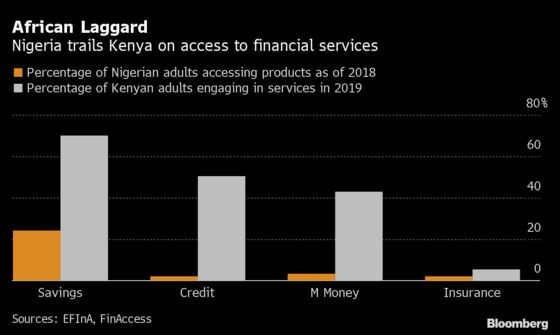

The sparring means the 60 million people in Africa’s largest economy who lack access to any banking services risk missing out on all the benefits of the financial-technology boom that has put much of Africa at the cutting edge of the revolution in mobile money.

Anticipating the underserved entering the market, foreign investors have jumped in. Flutterwave, based in Lagos and San Francisco, raised $170 million this year. That made it Nigeria’s second fintech startup with a valuation above $1 billion, after Interswitch. Jumia Technologies AD, a Berlin-based e-commerce platform that started in Lagos, has almost tripled since it sold shares in New York in 2019, giving it a market value of $3.4 billion.

The investment in Flutterwave by U.S. hedge fund Tiger Global Management LLC and New York private-equity firm Avenir is more than double the 26 billion naira ($64 million) spending on information technology by Nigeria’s two biggest banks in 2020. The two lenders spent 13.7 billion naira in the year earlier.

That helps explain why lenders including Guaranty Trust Bank Plc and Access Bank Plc, the country’s two biggest, could use some help from regulators. They’re planning to start payments units this year, more than a decade after counterparts in Kenya and South Africa.

While the government has opened up the industry to telecom companies to increase access to banking services, the Central Bank of Nigeria has yet to approve payment-service licenses to MTN Nigeria Communications Plc and Airtel Africa Plc; it’s been about two years since they applied for the permits, which allow them to provide most banking functions except lending and taking foreign-currency deposits.

The central bank has been “lethargic” when it comes to allowing telcos to become “very important players” in the payment system, Yele Okeremi, chief executive officer of Precise Financial System, a Lagos fintech, said by phone.

Central bank spokesman Osita Nwanisobi didn’t respond to messages seeking comment while calls to his mobile phone didn’t connect. An MTN spokesman said it’s still in talks with regulators and the banks to resolve the commission dispute.

Payments Market

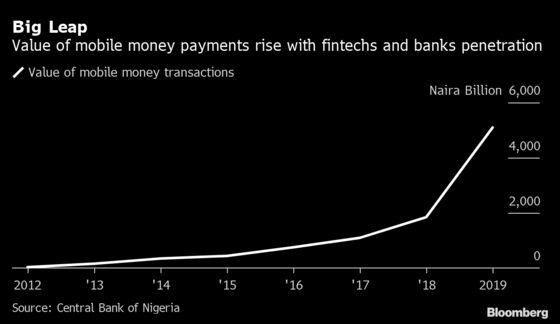

Even so, legacy banks are losing their grip on the market for electronic payments, which rose by a half last year to 158 trillion naira. Bank apps accounted for just 43% of such transactions in 2020, while non-banks, led by MTN, had 35%, according to the Nigerian Interbank Settlement System.

Regulators have also had to mediate a conflict between the banks and fintechs over pricing of USSD transactions -- the type made over phones -- fixing a flat fee of 6.98 naira per transaction, with banks collecting the charges. Banks are pressing regulators to require fintechs to charge customers separately through end-user billing, a move they’ve resisted.

“Ultimately we are going to go with end-user billing,” Segun Agbaje, managing director for Guaranty Trust Bank, the nation’s biggest lender, predicted an investor call last month. “You are going to see more of a migration from USSD to mobile banking because USSD will become an expensive channel.”

With their core lending businesses stagnant and investment flooding into fintech startups, the need for banks to move is increasingly urgent.

“Banking generally is shrinking rapidly that every traditional bank out there is thinking about how it can keep up,” said Idris, the consultant.

Guaranty Trust CEO Segun Agbaje, 56, is in the final stage of obtaining regulatory approval for a fintech unit, which he plans to start in the second half. He is pushing to create a separate payments business with a mobile wallet in Nigeria and three African countries, including Ghana and Cote d’Ivoire.

While banks have rolled out digital products mainly by partnering with technology firms, they want a separate license to control the payment infrastructure.

Access Bank is emphasizing payments, “which is in line with our corporate strategic plan,” Chief Executive Herbert Wigwe said on an investor call. “Payments and remittances are critical, and making sure you have full control over the infrastructure,“ Wigwe said.

For its part, Flutterwave doesn’t see itself as a threat to legacy lenders.

“Fintechs build bank-level features like loan, savings or investment apps off collaborations with banks,” CEO Olugbenga Agboola said. “We started Flutterwave because we realized that there were lots of efficient niche payment methods that we needed to connect into one reliable infrastructure.”

©2021 Bloomberg L.P.