Last Bastion of Credit Under Fire as Guggenheim Sees ‘More Pain’

Last Bastion of Credit Under Fire as Guggenheim Sees ‘More Pain’

(Bloomberg) -- Investors could be about to lose one of the last ports in the credit storm.

After a relentless eight-week retreat, America’s riskiest high-yield debt is now on the cusp of erasing its gains for the year. And if Wall Street bears are right, the recent pain is just a taste of what’s to come.

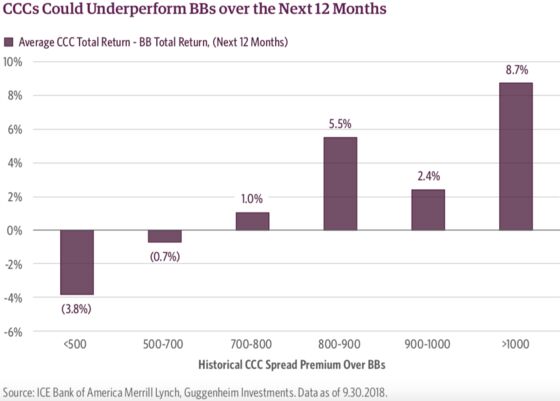

Guggenheim Chief Investment Officer Scott Minerd says the asset manager has already reduced corporate credit exposure to “the lowest levels since the financial crisis.’’ Now CCC rated debt is poised for significant underperformance over the next year, according to the firm’s analysts.

The catalyst for such doom and gloom? The “reach for yield” attitude that characterized the quantitative easing era is now reversing, and it’s stirring concern across corporate debt markets. With short-term bonds now offering a positive real return, there’s less need for investors to go up the risk spectrum. The pockets of the market most vulnerable to downgrades or defaults are in focus as investors contemplate a turn in the business cycle.

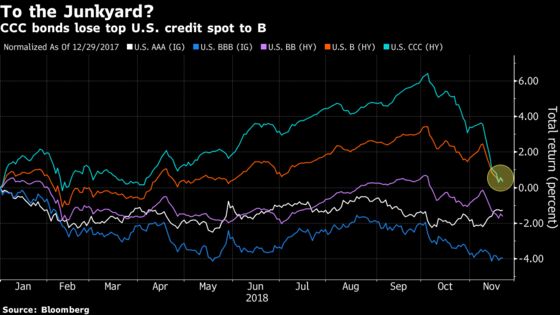

Beneath the Angels

Until now, BBB rated debt -- a group which includes embattled General Electric -- has been at the center of the storm.

This $2.5-trillion portion of the market is composed of companies on the last rung of the investment-grade ladder. If downgraded to junk, these so-called “fallen angels” would face higher refinancing costs as well as a drop-off in demand for existing issues.

But strategists are growing increasingly concerned about the least-creditworthy debt.

The Bloomberg Barclays CCC Index has declined more than 5 percent over the past eight weeks, the longest losing streak since 2015. In the process, CCC debt surrendered its crown for best U.S. credit performance this year. Higher-quality, B rated bonds have now provided a better return.

U.S. speculative-grade companies face a slew of challenges including rising rates, a slowing global economy, and domestic expansion getting ever longer in the tooth. Tumbling crude prices can also have a big impact on this segment -- energy companies comprise about 16.5 percent of the Bloomberg Barclays U.S. CCC Index by debt outstanding, slightly more than for the U.S. high-yield market as a whole.

“There is more pain to be felt in CCCs,’’ write Guggenheim’s Thomas Hauser and Rich de Wet.

The pair notes that the extra yield garnered from investing in CCCs relative to BBs is paltry by historical standards, which “does not bode well for potential returns.’’ Underperformance of nearly 400 basis points tends to follow such a deviation from the norm, they reckon.

It seems the market is finally starting to apply a quality filter to corporate debt amid the deepening rout in risk assets, heeding warnings from earlier this year.

In May, Goldman Sachs analysts led by Lotfi Karoui said that CCCs were the most “mispriced” since 2007, with a low premium even in the event that defaults failed to rise to levels consistent with a recession over the next five years. Since U.S. stocks closed at records on Sept. 20, CCC debt has proceeded to underperform the highest-quality AAA corporate bonds by more than 5 percentage points.

“De-emphasizing lower quality has been an ongoing trade theme all year,” said Geof Marshall, who oversees C$40 billion ($30 billion) of assets at CI Investments’ Signature Global Asset Management in Toronto. It was good to see the “upgrade” trade into high-rated issues “finally working in October and November,” he added.

And there’s a silver lining for investors worried about deepening damage in the CCC space: debt outstanding totals just $162.4 billion, less than 15 percent of the U.S. high yield market. But the fear is that any deterioration in junk bond fundamentals, and subsequent pressure on spreads and returns, won’t be confined to the category.

“CCCs have been the last sector to outperform in a dismal year like this,’’ said Ben Emons, chef economist and head of credit portfolio management at Intellectus Partners LLC. “Now that a correction seems underway, it is a broader signal that credit in general will begin to normalize in risk premiums as defaults in CCCs pick up and spread slowly through the B and BB complex.’’

--With assistance from Kelsey Butler.

To contact the reporters on this story: Luke Kawa in New York at lkawa@bloomberg.net;Cecile Gutscher in London at cgutscher@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Samuel Potter, Sid Verma

©2018 Bloomberg L.P.