CEO’s Plan to Save Sears Would Hand His Hedge Fund $1 Billion

CEO’s Plan to Save Sears Would Hand His Hedge Fund $1 Billion

(Bloomberg) -- Eddie Lampert’s hedge fund has a new plan for cutting Sears debt. The main beneficiary would be Eddie Lampert’s hedge fund.

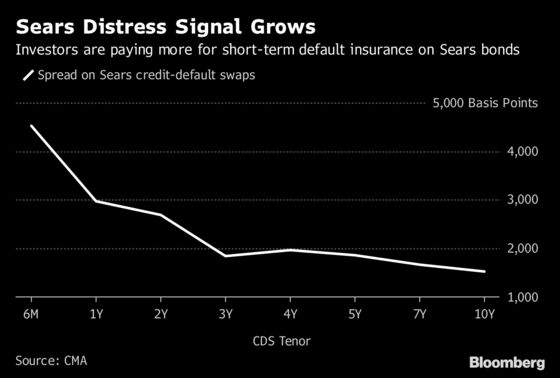

Lampert, Sears Holdings Corp.’s chief executive officer, called this week for the underperforming retailer to stanch the bleeding by paying off certain loans -- many of them owned by his hedge fund -- while swapping other debt for notes that convert to equity. This comes at a time when Sears stock is hovering just above $1 a share, an 87 percent dive in the past year.

“To have debt that’s convertible into equity when the equity is worthless doesn’t appear to be a very attractive proposal at all,’’ said Elliot Lutzker, chairman of the corporate law practice at Davidoff Hutcher & Citron LLP.

Lampert’s hedge fund, ESL Investments Inc., is the retail chain’s biggest shareholder. Because it owns about $2.5 billion in Sears debt concentrated in the category earmarked for repayment, ESL could recoup more than $1 billion under its own proposed plan.

Sinking Ship

Lampert has been struggling for years to plug the holes in the sinking ship. He’s shuttered hundreds of money-losing stores and promised to close an additional 150 this year, cut more than $1 billion in annual expenses, spun off units such as Craftsman tools and loaned the company his own money. Since 2012, losses have topped $11 billion. ESL’s restructuring plan, announced Monday, is the latest attempt at managing what some investors see as an end game.

“We will now be working aggressively to execute liability management transactions so that we can extend our runway and continue executing on our transformation strategy,’’ Sears said in a Tuesday internal message to employees seen by Bloomberg. “At the same time, we’ll continue to move forward with our other planned liquidity and cost measures.’’

“It is in the best interest of all stakeholders to accomplish this as a going concern, rather than alternatives that would substantially reduce, if not eliminate, value for stakeholders,” ESL said in its restructuring proposal.

Smaller Creditors

Given the downward trajectory of Sears, Lampert has done well for himself. When the retailer spun off Lands’ End Inc. in 2014, Lampert became the clothing manufacturer’s biggest shareholder. Sears has sold properties to a real estate investment trust called Seritage Growth Properties, and Seritage has leased the properties back to Sears. Seritage’s biggest unit holder is ESL.

“The Land’s End and Seritage transactions were carried out on transparent terms that delivered value to all Sears shareholders,” said an ESL spokesman. “Every shareholder had the same opportunity to participate in the offerings.”

ESL’s proposal would have Sears repurchase about $1.5 billion in debt backed by real estate assets, and Sears’s most recent regulatory filing shows that ESL owns most of it. Among the real estate-backed debt, Lampert’s fund holds over $1 billion in secured loans and $463 million in mezzanine debt, most of which would be redeemed at full value under its plan.

ESL proposed that Sears sell the real estate of about 200 stores in order to finance the debt redemptions.

While the upside for ESL in the restructuring is money in the bank, the plan’s appeal for smaller creditors is less clear. The retailer’s revenue is shrinking, to $4.4 billion in the second quarter of 2018 from $5.7 billion a year ago and $6.2 billion in the same three months of 2016.

‘Monstrous Investigation’

Hoffman Estates, Illinois-based Sears is working with Wachtell Lipton Rosen & Katz as counsel and Lazard Ltd. as investment banker, according to people familiar with the matter who were not authorized to speak publicly. Lazard declined to comment. Wachtell didn’t immediately return a request for comment.

“Sears must act immediately” on a debt plan, ESL said Monday, and should prioritize a solution that avoids bankruptcy court.

A bankruptcy process could deliver substantial fees to advisers at the expense of creditors. That’s been the case in recent retail restructurings that have ended in liquidations.

In Chapter 11, related-party transactions would expose Lampert to lengthy discovery processes and potential creditor claims, said Jeff Marwil, a partner and co-head of the restructuring and bankruptcy group at law firm Proskauer Rose LLP.

“He opens himself up to monstrous investigation” if Sears ends up in bankruptcy court, Marwil said. “From Lampert’s perspective, as an insider, the CEO, the largest shareholder, the biggest lender, and having done hundreds of millions if not billions of dollars in transactions to the potential detriment of Sears creditors, he’s at a huge risk in a Chapter 11 proceeding.”

Fairness Standard

In court, disparate creditor groups could examine Lampert’s past transactions and weigh their merit, and the deals would be judged by the fairness standard, Marwil said.

The fairness standard is a test for determining the validity of conflicted corporate transactions. It requires a company’s directors to show that the transactions were objectively fair.

The ESL proposal does little to fix the retailer’s underlying issues, Noel Hebert of Bloomberg Intelligence wrote in a note Tuesday.

“Few stand to benefit’’ from ESL’s proposed transformation plan beyond the lenders secured by Sears real estate assets, Hebert wrote. Trimming Sears debt, “stretching the maturity schedule and substantially reducing cash interest obligations still haven’t fixed a business that remains under-invested in and has generated negative free cash of about $1.8 billion in the last 12 months.’’

--With assistance from Katherine Burton and Claire Boston.

To contact the reporters on this story: Katherine Doherty in New York at kdoherty23@bloomberg.net;Eliza Ronalds-Hannon in New York at eronaldshann@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Bob Ivry

©2018 Bloomberg L.P.