Korea's 123-Year Old Conglomerate Plunges Almost 10%

Korea's 123-Year Old Conglomerate Plunges Almost 10%

(Bloomberg) -- Shares in a key firm in South Korea’s oldest conglomerate plunged, highlighting how a weak economy is hurting the nation’s biggest companies.

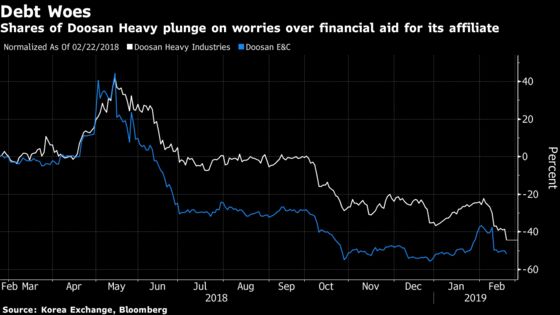

Doosan Heavy Industries & Construction Co.’s stock slid as much as 9.9 percent after the Seoul-based firm announced a new share sale partly to improve finances, and said it would buy 300 billion won ($267 million) worth of new equities of a troubled engineering affiliate. Its share price touched the lowest since August 2004.

Market concerns about Doosan Group’s outlook have been growing. Shares of Doosan Heavy and holding company Doosan Corp. were the biggest decliners on the Kospi 200 Index in the past month. Analysts in Seoul slashed price targets on Doosan Heavy, saying the new share sale plan was larger than expected. Rating firms have warned of cutting the debt ratings for Doosan Heavy, Doosan Corp. and Doosan Engineering & Construction Co.

South Korean companies have struggled as falling global demand hurt exports and domestic economic growth has slowed. But Doosan Group has been hit especially hard. Its engineering unit, whose shares Doosan Heavy is buying, is highly reliant on Korean business outside of Seoul that’s performing even worse than in the capital city. Doosan Heavy itself is losing money and the government’s policy of phasing out nuclear power has also taken away a key profit-driver from it.

The group increased debt from big acquisitions in the past including the $5.1 billion purchase of U.S. construction equipment maker Bobcat in 2007.

“I’ve sold all of my shares of Doosan units,” said Yoon Joon-won, a fund manager at HDC Asset Management. “Financial risks are running high at the group and I don’t see any business with positive outlook.”

Doosan Heavy shares closed down 8.8 percent on Friday, while Doosan E&C fell 3.3 percent and Doosan Corp. lost 0.7 percent. The Kospi index rose 0.1 percent.

Read more on what analysts had to say about Doosan’s share sale

Doosan E&C may need to repay 145 billion won in debt on March 21 and 70 billion won in November, while it also has 428 billion won of asset-backed debt that needs to be rolled over about every three months, according to a rating firm NICE Investors Service.

While the share sale plans would somewhat alleviate Doosan E&C’s liquidity risk, there are still uncertainties about its operating performance outlook given an unfavorable industry environment, the ratings firm said in a statement Friday.

Korean Miracle

The need to support Doosan E&C is weighing on the conglomerate as a whole, which got its start in 1896 as a linen store and was known as a symbol of South Korea’s economic miracle.

Doosan E&C plans to issue 420 billion won of new shares to secure cash after suffering a massive loss last year. Doosan Heavy aims to raise about 958 billion won in total by issuing new shares and selling assets. The proceeds would provide financial support to the construction unit.

Most investors will not subscribe for Doosan E&C’s new stock sale, says Park Sung-shin, a fund manager at KTB Asset Management. “Doosan Heavy is not in a good situation in terms of free cash flow. Maybe I need to be cautious on the stock for a while.”

Overcoming Difficulty

Not all of the Doosan group companies have seen their earnings worsen.

Doosan Infracore Co. and its overseas unit Doosan Bobcat Inc. saw their operating performance improving after overcoming difficult times amid a slowdown in global construction, according to Kim Sang-man, a credit analyst at Hana Financial Investment. The companies have become the group’s cash cow, he said.

“We expect Doosan E&C to slash its debt and interest expenses” after the share plan, Doosan Heavy said in an emailed statement on Thursday.

Doosan E&C’s debt-to-equity ratio surged to 553 percent at end-2018, from 195 percent a year earlier, according to rating firm NICE. Doosan Heavy will continue to face a high debt burden considering its limited cash generating ability, NICE said. It had 4.4 trillion won of total debt at the end of last year, compared with 377 billion won of earnings before interest, taxes, depreciation and amortization.

“Investors are worried that this might not be the end of the risks facing Doosan Heavy,” said Dong-heon Lee, an analyst at Daishin Securities Co. in Seoul.

--With assistance from Peter Pae.

To contact the reporters on this story: Heejin Kim in Seoul at hkim579@bloomberg.net;Kyungji Cho in Seoul at kcho54@bloomberg.net

To contact the editors responsible for this story: Divya Balji at dbalji1@bloomberg.net, ;Andrew Monahan at amonahan@bloomberg.net, Ken McCallum

©2019 Bloomberg L.P.