(Bloomberg Opinion) -- Ever since humans first rode in an elevator more than a century ago we’ve been afraid of getting stuck in one (or worse). The related requirement that these modern marvels are serviced and upgraded regularly is pretty handy for industry leaders Otis, Kone Oyj, Schindler and Thyssenkrupp AG. The companies generate about half their elevator revenues this way, as opposed to the lower-margin sales of original equipment.

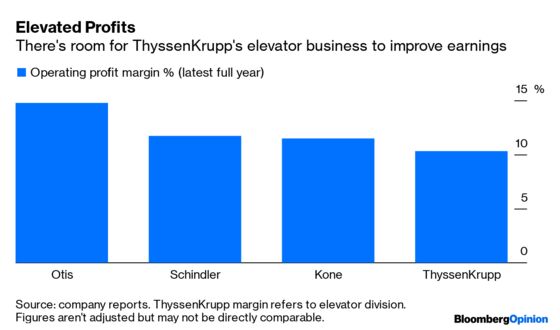

In good years Otis and Kone have achieved an operating return on sales in excess of 14%. That’s decent for the industrial sector, although a competitive Chinese market has made things more difficult lately.

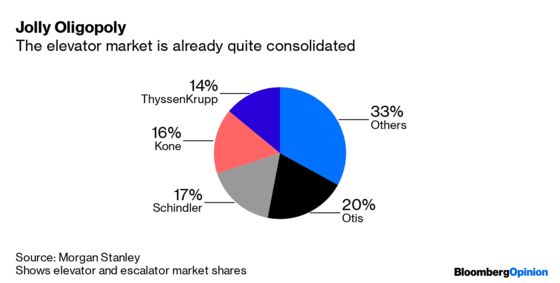

The decent profitability and oligopolistic industry structure are big attractions for would-be acquirers of Thyssenkrupp’s elevator unit, which the German conglomerate has put up for sale. But the big four’s dominance won’t have gone unnoticed by antitrust officials, who could play a central role in determining how any further consolidation plays out.

Depending on the bidder, any political desire to build a European elevator champion may run into resistance from those who fear entrenching the power of already dominant companies (as happened when Germany’s Siemens AG and France’s Alstom SA tried to merge their rail businesses).

Thyssenkrupp isn’t the only active player in the industry. United Technologies Corp.’s move to spin out its Otis elevator unit has triggered speculation that the U.S. manufacturer might also get involved in M&A. Last week, Switzerland’s Schindler denied a report that it had been targeted by its American rival. Finland’s Kone, meanwhile, is open about wanting to buy the Thyssenkrupp business, telling the Handelsblatt newspaper last week that the two companies would be “a perfect fit.”

Combining Kone and the Thyssenkrupp unit would create an industry behemoth with more than 16 billion euros ($17.7 billion) of sales. Though weaker than Kone’s, Thyssenkrupp’s elevator earnings have tended to far outstrip what the unwieldy German conglomerate makes from its other businesses. Its future should be bright too.

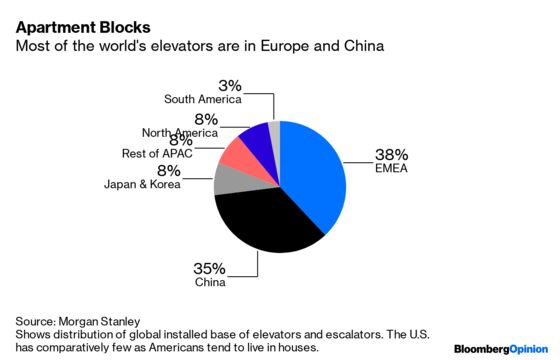

Urbanization, aging populations and more single-person households are all spurring the construction of denser, taller residential buildings, especially in Asia. China accounts for more than 60% of the world’s new elevator installations.

It’s reasonable to think the Thyssenkrupp elevator business would be worth about 15 billion euros if carved out – double the value investors ascribe to the whole conglomerate today. Add a premium for potential synergies and the value could rise further. Kone and Thyssenkrupp would complement each other well: the former is stronger in China while the latter has a bigger U.S. business. And the potential procurement, research and labor force savings from a merger would surely beat any earnings improvements that a private equity buyer could deliver by itself.

The big question is whether antitrust officials would agree to two of the big four elevator firms merging? It’s barely a decade since the European Union smacked the companies with almost 1 billion euros in fines for running a price-fixing cartel in several countries. Company employees rigged bids involving hospitals, the European Commision noted. Hardly a good precedent.

Thyssenkrupp is burning cash and its stock has fallen more than 35% in the past year. It can ill afford to get involved in another protracted and ultimately unsuccessful antitrust review. Earlier this year Brussels blocked an attempt to combine its European steel operations with Tata Steel.

Kone could sell certain assets to ease competition concerns. Still, it’s understandable that Thyssenkrupp is said to favor a partial sale to private equity, according to Bloomberg News’s Aaron Kirchfeld and colleagues. This might not realize the highest price but it’s surely the easier deal to pull off, provided trade unions can be reassured.

Europe has three world-beating elevator makers. Reducing the trio to two has clear benefits for the companies. What’s in it for customers isn’t quite so obvious.

The maintenance business is more fragmented, however.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2019 Bloomberg L.P.