KKR Says Retrenching Banks Boost Direct Lending Demand in Asia

KKR says the Asia’s entrepreneurs are seeking more direct loans as the coronavirus pandemic dries up other avenues of funding.

(Bloomberg) -- KKR & Co., Asia’s largest private equity investor, says the region’s entrepreneurs are seeking more direct loans as the coronavirus pandemic dries up other avenues of funding.

More opportunities to lend are emerging particularly in Southeast Asia, where some governments have fallen short in supporting companies hit by Covid-19, according to Brian Dillard, who oversees credit for Asia Pacific. Under Dillard, KKR has lent north of $1 billion over the past year. The firm is now preparing to raise its first dedicated credit fund for the region, people familiar with the matter said, declining to be identified as discussions aren’t public.

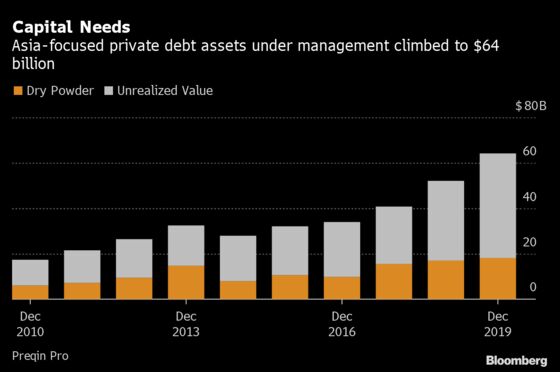

Private credit, which bypasses traditional lending channels, is still nascent in Asia even as it’s ballooned globally into an $850 billion asset class dominated by U.S. deals. Fueled by a thirst for yield, the sector has gained fresh impetus from the pandemic with borrowers looking for speedier access to cash at a time when banks have grown cautious. Asia represents an enormous opportunity, Dillard said, with returns several hundred basis points above what’s on offer in the competitive U.S. and European markets.

“The Covid crisis has caused many traditional lenders to retrench, and we are finding our private credit capital is more relevant to a wider group,” said Dillard, who moved to Hong Kong in 2018 after ramping up KKR’s alternative credit and special situations businesses in New York. “The companies are healthy, the growth opportunities are still there, what they’re missing is the capital.”

| Read more: |

|---|

| Billion Dollar Deals See Private Credit Step Out of the Shadows |

| How Private Credit Soared to Fuel Private Equity Boom: QuickTake |

| Credit Specialists Wanted for Australia Fund’s Push Into Asia |

Vietnam, Malaysia and Indonesia have seen the most activity, Dillard said, with a rising middle class spurring growth for businesses in property, healthcare and other consumer-focused areas. He’s hired former executives at Goldman Sachs Group AG, Credit Suisse Group AG and D.E. Shaw & Co. to expand the firm’s footprint in India, Southeast Asia and Australia.

While much Asia-focused capital has targeted distressed companies, KKR is keen on performing credit, backing acquisitions and helping families take their companies private. The firm seeks a mid-teens internal rate of return, Dillard said.

Despite the opportunities, KKR has suffered setbacks in India, where a long-running shadow banking crisis followed by the devastation of the pandemic has crippled the economy. The firm committed to a $150 million equity infusion to support the local unit and is now weighing a merger with InCred Financial Services Ltd., backed by former Deutsche Bank co-chief executive officer Anshu Jain.

Dillard spoke with Cathy Chan about the opportunities in Asia, the impact of Covid-19 and lessons learned in India. Edited excerpts from the interview follow.

What is driving private credit demand in Asia?

Underlying economic growth, but it’s also a lot of companies can’t get what they need from the bank market. They need more leverage, more flexible terms, more flexible covenant structures, cash-flow lending versus asset-backed lending, subordinated credit versus senior secured asset-backed. A lot of that demand for capital is ultimately provided by equity capital in Asia.

How big is the opportunity?

There’s a very, very large demand for capital. About 7% of all private credit assets under management are dedicated to Asia. The majority of that has been raised in the last five years, focused on distressed and special situations. The amount of capital focused on performing credits is relatively small. The ratio of private equity assets under management to private debt in Asia is like $24 of private equity capital for every dollar of private debt capital. That’s relative to $4 in Europe. So, it’s a hugely under-penetrated market and a big opportunity for the firm.

When we look at how credit is extended in the region, 80 cents of every dollar of credit in Asia is provided by the banks. That’s 60 cents in Europe and less than 10 cents in the U.S.

How has Covid-19 impacted your plans?

We’re seeing a lot of really interesting transaction opportunities, even more post Covid. We focused on three major factors. The first is, you see a lot of capital outflows from Asia. In Asia, for a lot of firms, this is one of the first places for people trying to de-risk when times are more difficult in the core, western markets.

The second piece is that we’re seeing across our businesses, in equity and in credit, banks pulling back, really focusing on their home markets. We also see a broader, risk-off sentiment from the key banks across Asia post-Covid. Both of these factors are limiting bank appetite for new credit.

The third factor is, on the private market side, valuation expectations between buyers and sellers have widened. Sellers still want to think about the value of their business on a pre-Covid basis, and the equity investors want to capture the dislocations. We think credit could be a pretty interesting way to bridge this gap.

What are the major risks in the region?

There are a variety of different cultures and it’s really important that you are local in the markets you’re operating in to understand it. We have been here since 2005, and have the experience to know not only how to structure a deal, but also, who to lend to, and groups to stay away from. One of the challenges in Asia is that a lot of jurisdictions have very different bankruptcy codes. And you’ve got to find ways to protect your investment and protect your decisions outside your formal bankruptcy process.

What lessons have you learned in India?

The country is in the midst of a credit crisis. You’re seeing a lot of capital being pulled out of the credit markets, particularly in the non-bank lending sector. We saw that happening and we stepped in pro-actively with equity commitment.

In the next vintage of transactions, you’re likely to see lower leveraged deals, a bigger focus on managing capital markets risk, and really focusing on new structures that deleverage over time, pay down debt, free cash flow, and serve as a bridge to the bank market for refinancing.

Right now, we’re more focused on playing offence in India than continuing to play defense on our existing portfolio. I am certain that we’ll continue to be active in the credit market. The byproduct of a credit crisis like the one we’re going through in India is there’s more opportunities for non-bank lenders like ourselves.

©2020 Bloomberg L.P.