(Bloomberg Opinion) -- Kinder Morgan Inc. would like you to know that, even if you’re not impressed, it has caught the eye of other paramours. Bits of it have, anyway.

The midstream giant reported earnings Wednesday evening that were mildly disappointing, missing the consensus estimate by a bit and dialing back expectations for another natural gas pipeline from the Permian Basin. No big drama, though. Which is kind of the problem.

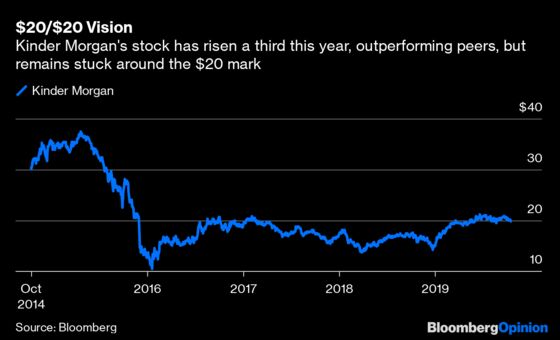

Kinder Morgan’s stock partially recovered from a plunge touched off by a savage dividend cut in late 2015, but has remained capped at about $20. Chairman Rich Kinder has grumbled about the seeming lack of love on several earnings calls — as management is wont to do — and the latest was no exception. This time, though, he noted the attentions of others. Talking about the $1.5 billion sale of the U.S. portion of the company’s Cochin pipeline, announced in August, he emphasized it sold at 13 times 2019 Ebitda estimates. Kinder trades at less than 11 times. So:

I should add that we received expressions of interest in other assets at similar or higher multiples of Ebitda. … All of this just indicates the substantial difference between the valuation of individual assets, and that of the Company as a whole when expressed as a multiple of Ebitda.

As the man himself said, there’s no certainty of any of these expressions of interest resulting in further deals. The subliminal message, though, is reasonably clear: The private market gets how valuable we are, why can’t you lot?

Again, this is a pretty standard argument for any company with a mix of businesses that feels like it’s trading at a discount. While Kinder Morgan’s stock is roughly where it was three years ago, the multiple has dropped 12% since then:

Most companies with a pipeline or two to their name have been squeezed as investors have withdrawn from the sector (see this), so Kinder Morgan isn’t alone. That said, it is remarkable that big increases in dividends beginning in 2018 and stock buybacks haven’t sparked a re-rating.

As I wrote here, part of the issue may be that the company retains some of the trappings of master limited partnerships, such as reporting distributable cash flow, despite ditching the structure five years ago. This seems counterproductive, given what has happened to MLPs since then.

Moreover, despite selling off several assets, net debt plus preferreds has dropped by only about $5 billion since the end of 2015, according to data compiled by Bloomberg. Ebitda, meanwhile, has been flat (partly due to disposals). Hence, leverage has come down but remains at the high end for its peer group, according to CreditSights, which puts that at 4.4 times Ebitda adjusted for the latest disposals.

Meanwhile, there’s the company’s so-called CO2 division, which produces carbon dioxide and uses some of that to produce oil from mature fields. While it accounts for less than 10% of Kinder Morgan’s profits, its exposure to production volume and commodity prices makes it a swing factor that can drag down overall performance — as it did in the latest quarter. There have long been calls for the company to sell it. Having not done so, Kinder Morgan appears content to curb investment in it for now.

Given the current environment for exploration and production stocks — which trade at less than 5 times Ebitda — it’s also unlikely the CO2 unit would fetch a good price. And that gets at an uncomfortable aspect of Kinder Morgan’s nod to higher private market multiples for this or that business. Yes, they can offer a vote of confidence in the value of a company’s underlying assets. The flip side, however, is that they also raise questions about why the remaining portfolio just doesn’t seem to spark the same interest with investors.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.