Junk Bonds Endure an Awful Day But Live to Tell About It

Junk Bonds Endure an Awful Day But Live to Tell About It

(Bloomberg Opinion) -- Bond traders have a technical name for what just happened to the U.S. high-yield bond market. They call it a “puke.”

The yield spread on junk bonds widened 33 basis points on Thursday, the biggest jump in more than seven years, to 508 basis points, according to Bloomberg Barclays data. As recently as Dec. 14, high-yield investors were holding on to a slight gain for 2018. Now they’re down 2.2 percent, on track for the first annual loss since 2015. Funds tracking U.S. corporate high-yield debt lost $788.5 million in the week ended Dec. 19, the fifth consecutive week of outflows, according to Lipper data. That followed a massive $2.06 billion withdrawal the previous week. And speculative-grade borrowers are steering clear of the meltdown entirely: December is shaping up to be the first month in 10 years with no bond sales.

Total returns in the junk bond market had remained positive for so long that some wondered whether the debt could provide shelter from equity-market volatility. At a certain point on Thursday, investors realized that wouldn’t be the case. Maybe it was because of a perceived misstep by Federal Reserve Chairman Jerome Powell, or the price of oil finally starting to bite, or any number of other reasons. Regardless, trading in the biggest high-yield funds shows exactly when the “puke” happened: Around 11:21 a.m. Here’s Bloomberg News’s Carolina Wilson on what exactly took place.

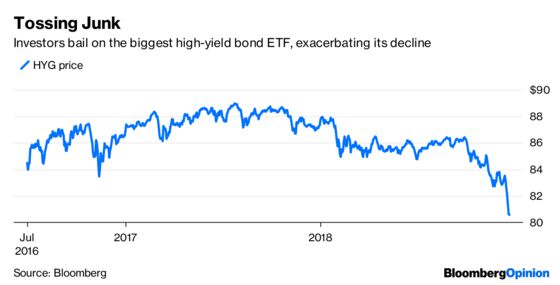

A trader sold close to 4 million shares worth $322 million of the iShares iBoxx High Yield Corporate Bond ETF, ticker HYG, at 11:21 a.m. in New York Thursday. About five minutes later, 8 million shares worth $267 million of the SPDR Bloomberg Barclays High Yield Bond ETF, ticker JNK, were sold. Then, another $350 million worth of HYG was unloaded at 1:39 p.m.

By the time the dust settled, trading volume in HYG soared to an all-time high, and the fund’s discount to its net asset value reached the largest since February. JNK, too, had one of its biggest days ever by both metrics. Both fund prices are the lowest since early 2016, when the market was just starting to bounce back from a collapse in the price of oil to less than $30 a barrel.

The marriage of relatively illiquid junk bonds and the instantaneous nature of exchange-traded funds has always been a dicey subject, with some investors expressing concern about how the products would react in a sharp sell-off. Thursday may have provided an answer: It’s painful, but not apocalyptic. For those who have doubts about how much stress the market is under, consider this: December is on track to the be the first-ever month in which high-yield ETFs experienced net outflows. Usually, enough money comes in, seeing the lower price as an attractive entry point.

One complicating factor, and a reason it might not be the time to dump everything high yield, is that the markets are approaching the end of the year, which means thin trading volume. “Right now, nobody wants to be a hero,” Randall Parrish, a senior portfolio manager at Voya Investment Management, told Bloomberg’s Claire Boston on Dec. 14, when junk bonds still had a positive return for 2018. That wound up being the right call.

Things could get worse, starting first and foremost with energy-sensitive bonds, given crude oil’s slide to $46 a barrel from more than $75 in early October. On the other hand, there’s no shortage of investors who appear ready to go bargain hunting when the calendar turns. It doesn’t hurt that New York Fed President John Williams not so subtly sought to calm financial markets with his comments Friday, potentially alleviating some concerns that the central bank is making a policy mistake.

Markets don’t feel better immediately after puking, but it’s the most violent part of repricing to a better level. Now that junk bonds have gotten that out of their system, expect a calmer ride the rest of the year as investors assess whether to step back in come January.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.