Junk Bonds Are Getting Hammered by Trump's Trade Wars

Junk Bonds Are Getting Hammered by Trump's Trade Wars

(Bloomberg) -- U.S. junk bonds are getting caught in trade-war crossfire.

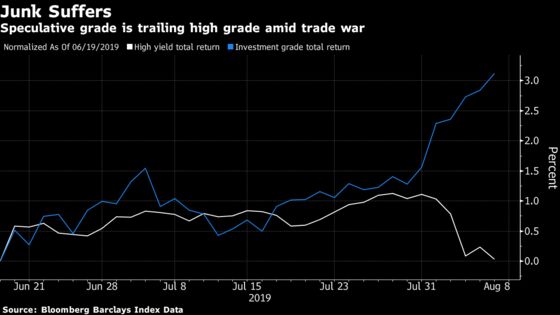

The securities slumped by more than 1% from the start of last week through Wednesday even as investment-grade company bonds rallied, according to Bloomberg Barclays index data for price and interest returns. The safest high-yield bonds reached their weakest level relative to high-grade corporate securities since 2016 by one measure. A fear gauge for the speculative-grade market soared the most on Monday since March.

Investors fret that squabbles over trade could do more than just hit corporate profits -- they may push some U.S. companies out of business entirely. Excluding the energy sector, by the middle of next year, around 3.2% of borrowers will have defaulted over the prior 12 months, compared with 2.5% now, UBS strategists forecast this week. That change is largely because of intensifying trade wars.

“The longer this goes on, the more pain is going to be felt on both sides and junk-bond prices could fall to reflect the potential for higher default rates,” said Brian Kennedy, a portfolio manager at Loomis Sayles & Co., which managed about $280 billion at the end of June.

Not every junk bond is getting hit, and some companies are still finding solid demand for their securities. Clear Channel Outdoor Holdings is expected to sell a $1.26 billion debt offering this week with yields toward the bottom end of original expectations. There is almost $15 trillion of negative yielding debt globally, forcing money managers to seek higher returns in the U.S.

But fears about tariffs and currency moves have been enough to counter the market’s exuberance about Federal Reserve interest-rate cuts, which can reduce borrowing costs for companies. Average junk-bond yields have risen more than 0.6 percentage point since June 20 to around 6.3%, according to Bloomberg Barclays index data through August 7. Investors yanked $4.07 billion from junk-bond funds in the week ended Wednesday, the most since October.

Read more in this week’s Credit Brief: Trade War Casualties; Shrinking BB Market

That jump came even as the Fed last week lowered rates for the first time in a decade, which brought benchmark 10-year Treasury yields to their lowest levels since 2016. High-yield market conditions were bad enough to spur US Farathane LLC, which supplies plastic parts to the auto industry, to pull a high-yield bond offering this week, according to people with knowledge of the matter. Sirius Minerals Plc, a mining company, suspended a bond sale as well.

The story is different for investment-grade company bonds, where yields fell below 3% for the first time since 2016. Risk premiums on the securities, the extra yield above Treasuries that investors get for holding the bonds, had widened from the end of July through Wednesday, but were still below levels seen in early June.

Escalating War

Risk premiums, or spreads, are high for junk bonds relative to investment-grade securities. One way to compare those two figures is to look at spreads for the safest high yield bonds, those rated in the BB tier, and the lowest quality high-grade bonds, rated in the BBB tier. Over the preceding two weeks, the difference in risk premiums widened by 0.43 percentage point to 2.31 percentage points, the biggest gap since the U.S. presidential elections in November 2016, according to strategists at JPMorgan on Wednesday. They adjusted their figures for duration.

U.S. President Donald Trump last week abruptly ramped up his trade war with China, announcing a 10% tariff on another $300 billion of imports from the nation. Beijing responded by letting its currency weaken, a move that makes the nation’s goods cheaper for Americans, and by asking state-owned enterprises to suspend purchases of U.S. agricultural products. On Thursday, the People’s Bank of China was seen as trying to stabilize the currency, and U.S. markets broadly rallied.

‘Incremental Cost’

Trump’s latest round of tariffs could hurt the U.S. tech sector, because it includes a broader range of tech products than prior duties, including Apple iPhones and Dell servers, according to a report from S&P Global Ratings. Economists at UBS forecast the levies could reduce U.S. gross domestic product by 0.25 percentage point, and lower China’s as well. Other areas that are exposed include retail and energy and mining, UBS said.

“There’s an incremental cost to every company that gets caught in the cross-hairs,” said Lale Topcuoglu, senior fund manager and head of credit at J O Hambro Capital Management.

Companies exposed to trade wars are already cutting their expectations for future earnings. For example, Rayonier Advanced Materials Inc., which makes paper, lumber, and other wood-based products, said this week it was cutting its full-year forecasts for a measure of results.

The lowest rated bonds, those graded in the CCC tier, have been hit hardest. They’ve gained just 5.1% this year through Wednesday, compared with the overall high-yield market’s 9.4%, and have fallen the most of any junk ratings group since the start of last week.

With risks rising and bond yields broadly falling, performance among different parts of the high-yield market is varying more, said Andrew Feltus, portfolio manager at Amundi Pioneer Asset Management, which managed about $84 billion as of June 30. Picking the right securities is even more important than it usually is.

“We haven’t panicked yet, but we’ve been a lot more sensitive to where valuations are,” Feltus said.

To contact the reporters on this story: Katrina Lewis in New York at klewis128@bloomberg.net;Caleb Mutua in New York at dmutua@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins

©2019 Bloomberg L.P.