JPMorgan Strategist Sees Early Signs of Credit-Market Stress

JPMorgan Sees ‘Early Signs’ of Stress on Credit and Funding

(Bloomberg) -- Fallout from the spreading coronavirus may be starting to affect credit and funding markets, according to JPMorgan Chase & Co.

Supply-chain disruptions and a demand shock caused by the virus could already be causing cash-flow problems for businesses, JPMorgan strategist Nikolaos Panigirtzoglou wrote in a note Friday. That’s probably even more true for smaller companies and those in sectors like travel and lodging, he said.

“If these shifts in credit and funding markets are sustained over the coming weeks and months, especially in the issuance space, credit channels might start amplifying the economic fallout from the Covid-19 crisis,” Panigirtzoglou wrote in the report. Unless “credit support by central banks and/or governments is broad, fast and direct, we note credit markets are facing an increased risk of the cycle turning with a lot more downgrades or even defaults over the coming months.”

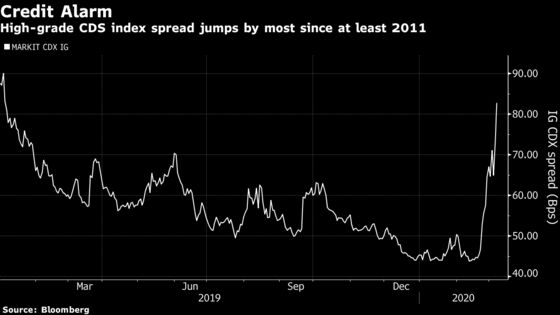

Credit markets suffered their worst day in a decade on Friday amid fears that coronavirus will hurt corporate income and stymie some companies’ ability to repay their debt. A derivatives index that measures the perceived risk of corporate credit surged by the most since at least 2011 and in Europe the cost of insuring senior financial debt skyrocketed.

Travel- and leisure-related companies were among those hit Friday, while energy-company bonds and loans fell further into distress as crude prices tumbled. News that Saudi Arabia plans to boost oil output, risking a global price war, may add to pressure on credit markets, according to Nordea Bank Abp.

“One of the most important issues facing authorities currently is arguably to try to keep the credit cycle alive and kicking,” strategists Andreas Steno Larsen, Martin Enlund and Joachim Bernhardsen wrote in a research report. The landslide in oil prices, “which will likely continue next week now that the Saudis have declared a full-blown price-race to the bottom, is another risk for the U.S. credit cycle,” they wrote.

Vulnerable Companies

Market concerns about ratings downgrades and companies dropping to junk status are justified by a look at credit fundamentals, the JPMorgan report said. The median net-debt-to-Ebitda ratio for companies in JPMorgan’s high-grade and high-yield companies in the U.S. and Europe has risen steeply in the past decade and is now higher than in the previous two cycles in 2007/2008 and 2001/2002, it said.

“Companies are currently much more vulnerable to a decline in incomes and/or a rise in corporate bond spreads and yields than in the previous two recessions,” Panigirtzoglou wrote. “This is especially true for U.S. credit and for Euro high yield given the absence there of the backstop from the European Central Bank’s corporate bond program that solely benefits Euro high grade.”

There are some signs of stress in Yankee issuance as well, the report said, noting it tends to be more sensitive to funding concerns because non-U.S. companies can find it harder to raise dollar funding relative to domestic U.S. companies in periods of stress.

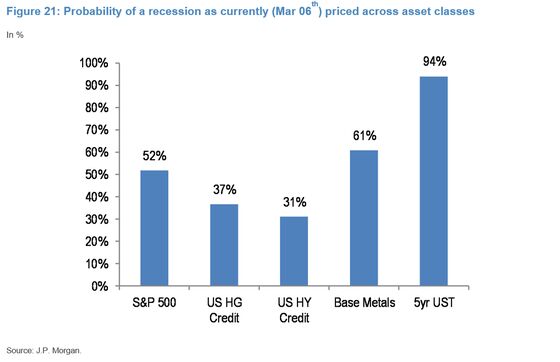

It’s also the case that credit appears most vulnerable to an economic downturn, according to the note, using an analysis which looks at the historical behavior of various asset classes around past U.S. recessions, particularly the move from the pre-recession peak to the trough during the event.

“Rate markets are now implying that something that looks like a U.S. recession is almost a certainty and have become even more disconnected from risky asset classes,” Panigirtzoglou wrote. “U.S. credit seems to be still most vulnerable to U.S. recession risks followed by U.S. equities.”

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Vivianne Rodrigues

©2020 Bloomberg L.P.