JPMorgan Sees Repo-Rate Spikes as Short-Lived, No Breakdown

JPMorgan Says Repo-Rate Spikes a Short Disruption, Not Breakdown

(Bloomberg) -- There’s little evidence of a breakdown in repo markets, and signs of stress in some indicators should be short-term issues, according to JPMorgan Chase & Co.

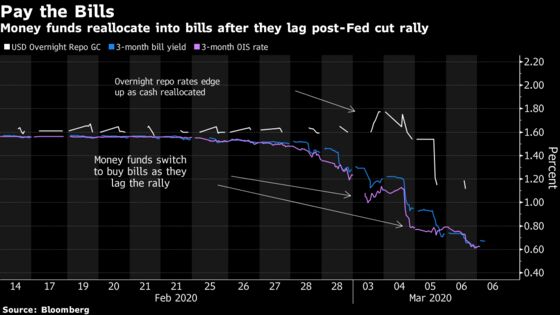

Repo rates across the triparty and bilateral parts of the market jumped to the widest levels since November after the Federal Reserve cut rates by 50 basis points earlier this week. But this was a sign of short-term money-market fund reallocations rather than the beginning of “something more sinister,” strategist Joshua Younger in New York wrote in a note Thursday.

After the Fed’s emergency cut, Treasury bills failed to match the pace of the rally in three-month Fed Funds expectations. Money-market funds, which tend to allocate cash between funding and Treasury bill markets, probably used the opportunity to pull cash out of repo markets and buy bills, pushing up repo rates as a result, Younger said.

Treasury bills have now fully caught up and as a result repo markets are also normalizing.

“This is not, in our view, the beginning of a breakdown, but rather a temporary and likely very short-lived disruption,” Younger wrote. “While SOFR/IOER in double-digits is understandably concerning we would expect that spread to normalize in the next few days” and “Fed liquidity operations should remain effective at controlling turn pricing.”

In September, concern about the repo market swelled after overnight rates jumped and the effective federal funds rate rose above the upper limit of the Fed’s target range. The central bank responded by injecting billions in cash to quell the surge. In recent months though, the Fed has been reducing liquidity injections faster than expected amid relative calm in the market.

That was before the coronavirus-induced market turbulence, and the Fed’s 50 basis-point rate cut. Lowering rates without allowing for the provision of extra liquidity would lead to new funding strains, Credit Suisse Group AG strategist Zoltan Pozsar said this week.

But Younger sees these moves as a technical disruption that’s already started to work itself out. The spike in rates was mostly due to bills lagging behind the move in OIS after the Fed cut, which led to some money-market fund allocation away from the repo market, he said.

--With assistance from Stephen Spratt.

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Nicholas Reynolds, Brendan Walsh

©2020 Bloomberg L.P.