JPMorgan Gets One More Boost Off Rate Hikes Before Fed Pause

The biggest U.S. bank is still reaping benefits from higher interest rates.

(Bloomberg) -- The Fed may have stopped raising borrowing costs for now, but the biggest U.S. bank is still reaping benefits from higher interest rates.

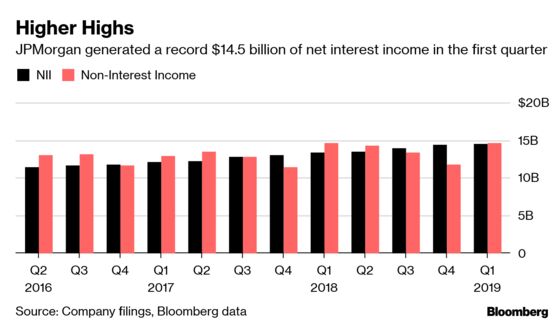

JPMorgan Chase & Co. said net interest income -- revenue from customers’ loan payments minus what the bank pays depositors -- jumped to $14.5 billion in the first quarter, a record aided by the Federal Reserve’s four interest-rate increases in 2018. The bank’s net interest margin jumped to the highest in seven years.

The bank reiterated its forecast for $58 billion of interest income this year, a $3 billion jump from 2018. Fed Chairman Jerome Powell has indicated rates are probably on hold for the foreseeable future, and analysts are predicting the first quarter was probably the last for now to get a boost from monetary policy.

“While we may not have a tailwind of higher rates, we also may not have the same kinds of pressures that we would see” to pay more to depositors, Chief Financial Office Marianne Lake said on a conference call with analysts. “You could argue a patient Fed and lower rates for longer may elongate the cycle.”

NII has been a key driver for revenue in recent quarters across the industry. The first quarter’s 1 percent increase from the fourth quarter was better than the company’s forecast that the figure would be flat.

Return on tangible equity increased to 19 percent, above the 17 percent full-year profitability target the bank set in February. Return on common equity hit 16 percent, the highest since the financial crisis.

Trading revenue dropped 17 percent to $5.5 billion, slightly better than analysts’ estimates of an 18 percent decline. Both equity and fixed-income trading fell.

Co-President Daniel Pinto tempered expectations for trading revenue in February, saying the figure would probably drop by a “high-teens” percentage in the first quarter from last year’s $6.6 billion. He blamed the drop on declines in the currencies and emerging-markets units.

Revenue from equity underwriting fell 23 percent to $265 million, the lowest since the start of 2016, as a 35-day U.S. government shutdown delayed new offerings.

Shares of the company, which gained 8.8 percent this year through Thursday, rose 4 percent to $110.51 at 9:55 a.m. in New York. That was the highest since Dec. 3.

Non-interest expense rose 2 percent to $16.4 billion, the highest since the third quarter of 2013. The bank has been funneling a portion of profits into new technology, branch openings and its equities-trading business. That could lead expenses to jump by more than $2 billion in 2019, JPMorgan said in February.

JPMorgan’s book of what it considers core loans, which doesn’t include lending by the investment bank, expanded 5 percent to $781.1 billion, compared with a 6.7 percent gain last year. The bank had previously warned that loan growth wouldn’t expand as quickly this year as it focuses on high-quality debt.

Other Key Results:

- Net income jumped 5 percent to $9.18 billion, or $2.65 a share, from $8.71 billion, or $2.37, a year earlier. Analysts surveyed by Bloomberg had forecast adjusted earnings of $2.35 a share.

- Revenue on a managed basis increased 5 percent to $29.9 billion, beating the $28.4 billion average estimate of 18 analysts surveyed by Bloomberg.

- Interest expense increased 70 percent to $7.4 billion as higher rates also meant the bank paid more to depositors.

- Even as the bank opens branches in new states, the number of storefronts decreased 2 percent to 5,028.

To contact the reporter on this story: Michelle F. Davis in New York at mdavis194@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Steve Dickson

©2019 Bloomberg L.P.