JPMorgan Expects $32.9 Billion Junk-Rated Debt Sales This Autumn

Investor demand for higher yields will fuel about $32.9 billion-equivalent of speculative-grade debt sales over next two months.

(Bloomberg) -- Investor demand for higher yields will help fuel about 30 billion euros-equivalent ($32.9 billion) of speculative-grade debt sales over the next two months, estimates by JPMorgan Chase & Co. show.

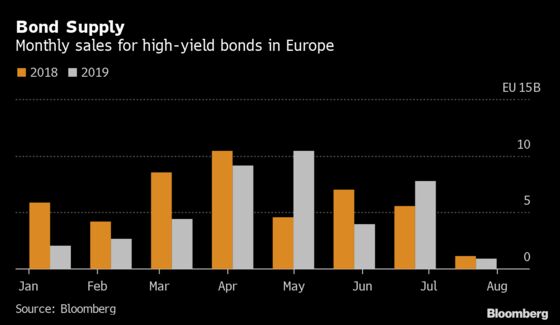

That would help salvage what’s been a luckluster year for high-yield bond and leveraged loan sales in Europe, which are collectively down 23.6 billion euros compared with the same period of 2018, according to data compiled by Bloomberg.

“The technical conditions are as favourable as we have seen over the past few years,” Kevin Foley, JPMorgan’s head of leveraged finance capital markets for EMEA, said in an interview ahead of the lender’s European High Yield & Leveraged Finance Conference on Wednesday.

Arrangers say a surge of appetite for assets paying rich margins could even spur some higher risk financings, which would mark a shift from the cautious approach that’s characterized the market for much of this year. Since the start of January only three bond deals have priced in Europe with at least one CCC rating, the data show, versus nine last year and 18 in 2017.

Cautiously Selective

Jumbo deals expected to launch soon include the buyout of Merlin Entertainments Plc, which could bring bonds and loans worth about 3.3 billion pounds-equivalent. Elsewhere, a potential acquisition of Kantar and a refinancing for Prisa may inject another 3.7 billion euros-equivalent into the market over the next six weeks, according to people familiar with the deals.

But amid the deluge of supply investors will be on the lookout for increased levels of risk given a backdrop characterized by weaker global economic growth and rising defaults.

“We’ve had strong total returns for high-yield in particular this year but where normally every tide lifts a ship, the mentality has shifted this time around and investors are now taking a much more cautious approach to credit selection,” James Turner, head of European leveraged finance at BlackRock International Ltd, said in an interview.

And while the appetite to secure higher yields remains strong, there’s a “heightening need for a cautious outlook,” especially regarding some cyclical names and those in the auto and retail sectors, according to Turner.

“There are near-term financing requirements and investors certainly have the appetite for these kinds of situations,” JPMorgan’s Foley said. “We’d challenge the view that the market is steering clear of cyclical credits. It’s more a matter of the leverage being appropriate and people being adequately compensated for the risk.”

Madelaine Jones, a portfolio manager for Oaktree Capital Management’s high-yield and loan strategies, points out that some investment decisions are being driven by a bet that future central bank support -- coupled with a dearth of buying opportunities -- can override weak fundamentals.

“Time will tell if that is correct,” Jones said. “But in the meantime the fragility of that investor conviction creates opportunities for the nimble manager when the mood music sours.”

To contact the reporter on this story: Laura Benitez in London at lbenitez1@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, Charles Daly

©2019 Bloomberg L.P.