Banks Balk at Compensation for 'Big Bang' Rate Losses

Lenders are responding to an overhaul that wiped millions of euros off some swaptions portfolios this week.

(Bloomberg) -- JPMorgan Chase & Co., Deutsche Bank AG and Nomura Holdings Inc. are among banks telling clients they won’t compensate them for trades that lose value during the “big bang” transition sweeping through Europe’s interest-rate derivatives market.

Banco Santander SA and BNP Paribas SA also won’t reimburse for losses on so-called swaption trades caused by a change in how the industry prices these deals, according to people familiar with the matter who asked not to be named discussing private information. Swaptions are derivatives that give the owner the right to buy an interest-rate swap in the future.

Lenders are responding to an overhaul that wiped millions of euros off some swaptions portfolios this week and will be closely watched in the U.S., where banks await similar changes due in October.

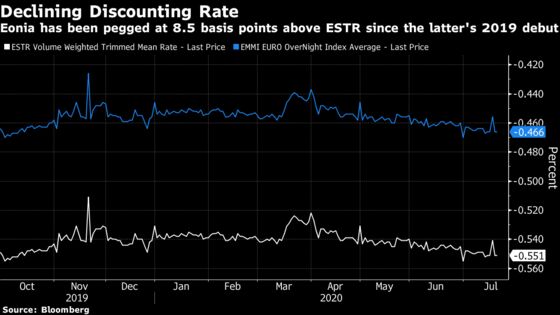

Banks and money managers had been racing to cement gains and avoid losses before the shift from the Eonia benchmark to the new euro short-term rate. The benchmark is used to help value hundreds of billions of euros of swaption contracts.

The firms expressed concern about a recommendation from a European Central Bank-backed committee to make voluntary payments following the switchover on Monday. JPMorgan told clients the process needed to be contractually enforceable, while Nomura said there was no market consensus on how to address the problem. These banks also won’t receive compensation if they have lost out.

Nomura said it was concerned about inconsistencies and “cherry picking,” with participants taking different approaches to voluntary compensation. The bank told clients in a letter that it would keep its policy under review. Nomura spokeswoman Aoife Reynolds confirmed the contents of the letter but declined to comment further.

| What’s at Stake: |

|---|

|

JPMorgan told clients before the switchover it recognized the advantages of compensation, provided this complied with fiduciary and general corporate obligations.

“We remain open to finding a solution that would allow for compensation to be exchanged in a workable way, prior to July 24,” JPMorgan said in a letter, which Patrick Burton, a spokesman for the bank, confirmed was genuine. “If no acceptable solution is reached by that date, we will, as a default position, adhere to the existing terms of the contracts that we have in place with our clients.”

Deutsche Bank will simply honor the terms of the original swaption contracts, according to a person familiar with the matter, who asked not to be named given the sensitivity. The bank knew the compensation program would only work if the majority of those involved took part, and it became clear in the last few weeks that this wouldn’t happen, the person said.

An ECB spokesman declined to comment and referred to the working group’s recommendation, which said market feedback had not produced a preferred option or even a consensus about the scope of swaption contracts to be compensated.

Not everyone is ruling out redress. Bank of America Corp. aims to accommodate payment requests to the extent the lender can recover the funds from counterparties on related market hedges, according to a person familiar with the matter who asked not to be named given the sensitivity.

‘World Peace’

Priya Misra, head of global rates strategy at TD Securities in New York, said she was unsurprised some had declined to pay.

“I think of it like world peace,” she said. “Voluntary compensation needs both sides to agree to work, otherwise the compensating party is worse off. Also it is an OTC market, so who decides if you and your counterparty disagree on the amount?”

Pension funds and insurers are more likely to have in-the-money legacy receiver swaps and therefore gain from the switch, she said, while their counterparties could lose out.

| Read More: |

|---|

|

“If even a few large dealers opt out of compensation, it reduces competitive pressure on others and can ‘allow’ others to opt out,” she said, adding that if banks take the same approach in the much larger U.S. swaption market, it would have a “significant profit and loss impact” for many participants.

Firms won’t decide against compensation lightly, said Suzanna Brunton, a managing associate at Linklaters LLP in Paris. Relevant factors are likely to include the need to treat counterparties consistently and the lack of clarity around how to calculate payments, she said.

What Bloomberg Intelligence Says:

“There is no legal parachute for the dealers on the losing side. Selective compensation is far from ideal as you may end up paying some counterparties but not receiving from others. It may end up being only a limited amount of banks participate, if any.”

-- Tanvir Sandhu, Chief Global Derivatives Strategist

The ECB began phasing in ESTR last October, and the benchmark will fully replace Eonia, which is still linked to more than 100 trillion euros of financial instruments, in early 2022. Regulators prefer ESTR because it’s underpinned by more robust trading, making it a truer reflection of the cost of capital and less susceptible to corruption.

©2020 Bloomberg L.P.