JPMorgan Catches Distressed Credit Funds Buying Blue-Chip Deals

JPMorgan Catches Distressed Credit Funds Buying Blue-Chip Deals

(Bloomberg) -- Risk premiums on high-grade bonds have become so attractive to investors that even distressed funds are fighting for a piece of the action, says JPMorgan Chase & Co., the top underwriter of primary-market deals this year.

High-yield and macro funds are also placing orders in what’s been a record spurt of issuance in recent weeks, according to Bob LoBue, global head of fixed-income syndicate at the New York-based bank.

“They’re looking for investable assets and it’s more about relative value right now,” LoBue said in an interview. “Most of these investors are long-term buyers even if they’re not traditional.”

Bargain hunters are piling into U.S. credit after one of the worst sell-offs since the financial crisis, betting the balance sheets of America’s safest borrowers will be able to withstand the looming recession. Beyond the surging crossover interest, firms such as Morgan Stanley and Guggenheim Securities also say they’re now bullish investment-grade debt after long being cautious, while BlackRock Inc. sees opportunities amid historically cheap valuations and unlimited support by the Federal Reserve.

Read more: Angelo Gordon went on $500 million credit binge in Fed aid week

Companies have sold almost a quarter-trillion dollars of high-grade bonds over the past two weeks to boost liquidity as the coronavirus outbreak wreaks havoc on the global economy. JPMorgan has been the top underwriter of blue-chip offerings this year, manging about 13.5% of issuance, according to Bloomberg league table data.

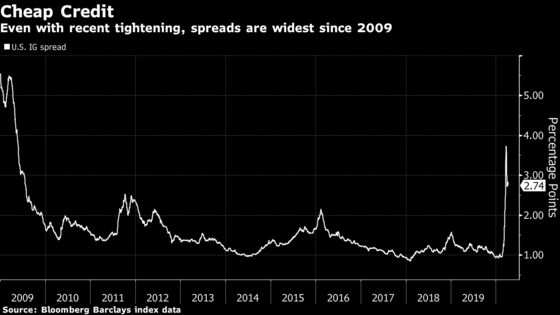

All that money hasn’t been cheap to borrow, with investment-grade spreads near the highest level since 2009. New issue concessions, or the extra yield issuers pay over their existing credit curve to sell a new bond, have averaged 19 basis points this year, versus just 4 for all of 2019.

Last week alone, companies sold more than $117 billion of U.S. high-grade corporate bonds, with many deals well oversubscribed. Oracle Corp.’s $20 billion offering drew as much as $58 billion of orders last week, while T-Mobile US Inc.’s $19 billion sale raked in $75 billion of demand at its peak. Carnival Corp., though technically investment-grade rated, was run off of syndicates’ high-yield desks, and was ultimately upsized to reflect strong investor demand.

Reverse Inquiries

At the onset of the pandemic, U.S. capital markets initially only reopened to the highest-quality investment-grade companies, especially banks and utilities. That’s changed as investors become more comfortable with riskier credits, including more high-yield companies and the first leveraged loan offering in nearly a month.

Money managers are increasingly asking bankers to bring new deals from companies that have an identifiable need for new funds, like those that have upcoming maturities or have recently drawn on bank lines, according to LoBue. Speculative-grade Wynn Resorts Ltd. was planning to borrow under its credit line last month, and is marketing a new high-yield bond offering Tuesday.

“The most important thing to borrowers right now is flexibility and being prudent with the balance sheet,” LoBue said.

©2020 Bloomberg L.P.