JPMorgan Bets $1 Billion of Its Own Cash for Sinclair Deal

JPMorgan Bets $1 Billion of Its Own Cash for Sinclair Deal

(Bloomberg) -- To help pull off the biggest media deal of the year, JPMorgan Chase & Co. embraced a Wall Street practice that fell out of favor after the financial crisis.

The largest U.S. bank agreed to take a $1 billion equity stake using its own money. The check helped Sinclair Broadcast Group Inc. amass the cash it needed for a $9.6 billion purchase from Walt Disney Co. without too much leverage. In exchange, JPMorgan got the promise of juicy returns.

It’s an unusual move for almost any regulated bank, but especially for JPMorgan, which would have deemed such an investment too risky a few years ago, according to people with knowledge of the bank’s strategy, who asked not to be identified discussing internal matters.

JPMorgan’s investment bankers got approval from senior executives about a year ago to invest the bank’s own money to help arrange bespoke financings for a coterie of corporate clients, one of the people said. Since then, the team has deployed the strategy five times, with the investment in the Sinclair deal the largest yet, the person said.

A JPMorgan spokeswoman declined to comment.

The arrangement shows just how competitive the lucrative business of lending to riskier companies has gotten. After the financial crisis, Wall Street firms like JPMorgan cut back on principal investments because of regulations requiring banks to bolster capital and reduce such use of their own money. JPMorgan said in 2013 it would break off its private equity unit, One Equity Partners, to focus on its main businesses. It also sold the investment bank’s Global Special Opportunities Group equity and mezzanine financing portfolio.

Regulators’ Restrictions

Bank regulators also imposed stricter guidelines on lending to riskier companies. Since then, non-banks -- or so-called shadow lenders -- including Ares Management Corp. and KKR & Co. have taken a larger share of the business, edging traditional banks out of the financing process on riskier deals they wouldn’t touch. With interest rates low, private equity firms and other investors launched debt funds that amassed billions of dollars from investors seeking higher yields.

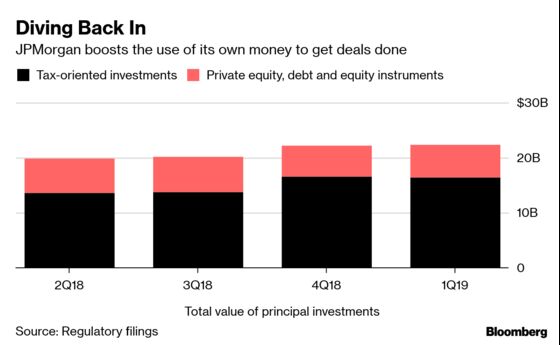

JPMorgan has been gradually stepping up principal investments in recent quarters, according to regulatory filings, as competition between banks and shadow lenders heats up. The value of non-tax-oriented investments in private equity, debt and equity instruments climbed to $6 billion in this year’s first quarter at JPMorgan, up from $5.5 billion at the end of 2017, the first time the bank reported the data since curtailing principal investments. The figures don’t include the $1 billion in the Sinclair deal.

Leg Up

Being able to structure and then put money into longer-term, illiquid investments has given the company a leg up when bidding for financing business because few banks are willing to take them on.

Read more: Shadow banks disrupt leveraged loans in blow to Wall Street

In November, JPMorgan was involved in a similar transaction, contributing preferred equity to help Veritas Capital and Elliott Management with their $5.7 billion buyout of health-care technology company Athenahealth Inc. through an entity called JPMorgan Chase Funding Inc., according to a regulatory filing. The bank used its own money to make the investment, said one of the people with knowledge of the bank’s strategy.

Buffett’s Plan

The pivot comes as companies increasingly rely on debt substitutes like preferred equity or junior capital to reduce the amount of debt they need to raise. Last month, Warren Buffett’s Berkshire Hathaway Inc. disclosed plans to inject $10 billion into Occidental Petroleum Corp. in exchange for preferred stock and warrants to help with the oil company’s unsolicited bid for Anadarko Petroleum Corp.

Goldman Sachs Group Inc. has long been renowned for its stomach in taking on large chunks of capital -- from secured loans to preferred equity -- to help facilitate deals. But it typically makes investments through mezzanine debt and senior loan funds. That’s helped the bank win a top position in underwriting leveraged loans. Barclays Plc and BNP Paribas SA are also considering setting up U.S. funds to better compete on deal financings, people with knowledge of the matter said in April.

JPMorgan doesn’t necessarily plan to hold the stakes forever. It’s gradually placed pieces of capital with sovereign-wealth funds, insurance companies or credit hedge funds, said the person with knowledge of the bank’s strategy. But finding buyers can take months or even years since there aren’t natural markets for many of the instruments.

Leverage in Check

Selling preferred stock to minority non-controlling investors can help a company boost the price it’s able to pay for a takeover target -- and keep leverage in check. In exchange, an investor can collect a higher return than it would from debt and is senior to common shareholders in the capital stack.

The flexibility offered by preferred stock was particularly alluring to Sinclair.

“We have been sensitive to equity-holders’ desire to keep leverage reasonable and so are bringing in a privately placed preferred instrument,” Sinclair Chief Executive Officer Christopher Ripley said on a conference call with analysts after the deal was announced. “We think it offers a lot of flexibility while preserving our overall leverage. It does have the flexibility to be taken out and replaced with other partners.”

--With assistance from Davide Scigliuzzo and Christopher Palmeri.

To contact the reporter on this story: Michelle F. Davis in New York at mdavis194@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Daniel Taub, David Scheer

©2019 Bloomberg L.P.