Japan's Sweeping Stock Market Overhaul Seen Sparking M&A Boom

Japan's Sweeping Stock Market Overhaul Seen Sparking M&A Boom

(Bloomberg) -- The biggest overhaul of Japan’s equity market in decades may be set to spur a wave of mergers and acquisitions.

The Tokyo Stock Exchange is considering cutting its number of markets to three from five, creating a “Prime” segment for the biggest and best-governed stocks. It could also slash the number of companies in the country’s bloated benchmark index, which currently has more than 2,100 firms, many of which are small and hard to trade.

If Topix index membership is shrunk to a level on par with the S&P 500 Index in the U.S., that could force passive funds to sell companies that don’t make the grade. Size would become more important than ever for attracting stock investment. And that, in turn, could lead to a spate of M&A by firms looking to get into the gauge.

“The TSE creating this Olympic team will certainly boost the animal spirits of corporate leaders to merge,” said Jesper Koll, senior advisor of WisdomTree Investments Inc. “M&A is the easiest way” to get into the top index when the TSE decides to revamp the market, he said.

Koll said sectors such as machinery, machine tools and brokerages are ripe for consolidation.

A working group at the Financial Services Agency, the market regulator, proposed last month that the exchange should have three markets after the overhaul -- Prime, Standard and Growth. It’s now considering the criteria for each market, including the minimum market value.

It also suggested making a “better index that institutional investors can find useful.”

Next Steps

The FSA will give the Tokyo Stock Exchange a report on market reforms by the end of the year, and the bourse will begin planning the overhaul from the start of next year, Akira Kiyota, chief executive officer of Japan Exchange Group Inc., told reporters in Tokyo on Dec. 17. The TSE would like to have “some form of structure” planned by June or July, he said.

The moves would be the biggest change for investors in Japan’s $6.3 trillion stock market since the Tokyo exchange was reorganized into the first and second sections, the current main and secondary boards, in 1961. The Tokyo and Osaka bourses’ merger in 2013 created duplication among markets, including multiple venues for smaller shares.

“If they decide on a premium segment it will be a disadvantage for small caps and it might trigger more small-cap M&A,” said Julian Mittag, a fund manager at Principal Real Estate Investors in Singapore. “Most companies want to be included in the premium segment.”

Attention will focus on the minimum market capitalization requirement for the Prime market. The TSE’s current first section, which contains the companies in the Topix, allows unlisted firms to list there directly if they have a market value of at least 25 billion yen ($228 million). But there’s a loophole for stocks in the Mothers market of smaller shares. In some cases, they can move to the first section with a market cap of as low as 4 billion yen.

Small, Illiquid

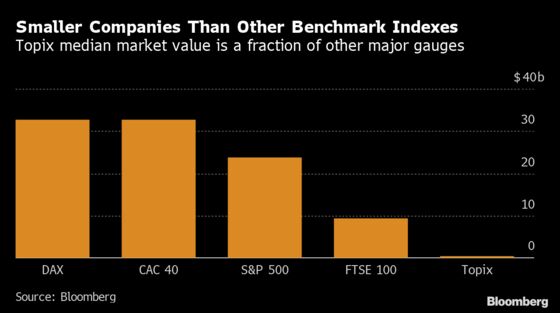

The median market value of companies in the Topix is currently about $454 million, which is tiny compared to the $23.8 billion for firms in the S&P 500. The smallest stock in the Topix has a market cap of just $23 million. Its equivalent in the U.S. gauge is valued at $3.7 billion.

And trading volumes are also much lower. The median number of shares changing hands at Topix companies on Dec. 18 was 84,400, compared with about 2 million for firms in the S&P 500.

The new Prime segment would include listed companies with sufficient market value and liquidity to attract institutional investors, according to the FSA working group’s proposal. The constituents would also have high governance standards, it said. The new index would pick stocks not only from the Prime market but also the Standard segment, it said.

Aside from spurring M&A, investors see the market overhaul as having positive effects for corporate governance.

It’s “quite significant,” said Mark Mobius, who set up Mobius Capital Partners last year after three decades at Franklin Templeton Investments. The key point is the new index will include firms that are not only large and liquid but also have good governance, he said.

Stock Sell-Off

Some stock holders expressed concern the change will send their shares plunging. Any revamp of the Topix could prompt investment giants such as the $1.5 trillion Government Pension Investment Fund, as well the Bank of Japan, to adjust their holdings and investment approaches, potentially causing some companies’ shares to plummet.

“The restructuring when enacted will trigger a wave of rebalancing for funds tracking” the index, said Justin Tang, head of Asian research at United First Partners, an investment and advisory group that specializes in special situations. “There will be a slew of arbitrage opportunities.”

For Keiichi Ito, chief quant analyst at SMBC Nikko Securities Inc. in Tokyo, the key point isn’t the consolidation of market segments: It’s which stocks will be included in the new Topix.

“It’s what happens to the Topix that will impact share prices,” he said. “There will be stocks that won’t be included from Prime while there will be companies that get included from Standard,” he said. “It will be impossible to avoid an impact on individual shares.”

Three Years

Pictet Asset Management Ltd. strategist Takatoshi Itoshima said the Topix change may take longer than other parts of the market structure revamp. “Changing this index will take a lot more work,” he said. “It’ll be a long-term issue.”

Makoto Furukawa, chief portfolio strategist for Mitsubishi UFJ Morgan Stanley Securities Co. in Tokyo, agreed.

“It would be realistic if they took about three years to change the index, step by step,” he said. “It’s likely that they will listen to a variety of opinions and find a direction that won’t have as big an impact.”

Here’s what other analysts are saying about the TSE’s plans:

Foreign Investors Seen Returning

“Foreign investors may turn their attention to Japanese stocks again” following the market reforms, said Shunichi Ashida, a quants analyst at Daiwa Securities Group Inc.

Overseas investors sold a net $8.2 billion in Japanese shares so far this year, even though the Topix has gained 15.8% in 2019 so far.

‘Dark Ages’

“It should drag Japan’s broader market from the dark ages,” said Amir Anvarzadeh, a market strategist at Asymmetric Advisors in Singapore. “Generally, it should make first-section stocks better representative of the market in terms of weighting and importance, and could finally replace the Nikkei 225 Stock Average as the benchmark, which is also very outdated.”

While some investors consider the Topix as Japan’s benchmark gauge, others still use the Nikkei 225.

Long-Short Strategy

For hedging the risks arising from the TSE’s overhaul, “investors would typically engage in a long-short strategy in this instance by buying the stocks they predict will be in the first section against those that will get booted out,” said Tang of United First Partners.

Don’t Expect Radical Change

“I do not expect a radical change in the Topix or in flows because there would be huge pushback from companies,” said Travis Lundy, a special-situations analyst who publishes on Smartkarma. “It may encourage more mergers so small companies become bigger to maintain the value of a listing.”

--With assistance from Zhen Hao Toh and Yilun Guo.

To contact the reporters on this story: Abhishek Vishnoi in Singapore at avishnoi4@bloomberg.net;Min Jeong Lee in Tokyo at mlee754@bloomberg.net;Shoko Oda in Tokyo at soda13@bloomberg.net;Toshiro Hasegawa in Tokyo at thasegawa6@bloomberg.net

To contact the editors responsible for this story: Lianting Tu at ltu4@bloomberg.net, Tom Redmond, Ravil Shirodkar

©2019 Bloomberg L.P.