Janus Bond Chief Maroutsos Bets Volatility Is About to Break Out

Janus Bond Chief Maroutsos Bets Volatility Is About to Break Out

(Bloomberg) -- Nick Maroutsos is betting that turbulence is poised to return to the world’s most actively traded currency pair, amid swirling forces like Brexit and Europe’s gloomy growth outlook.

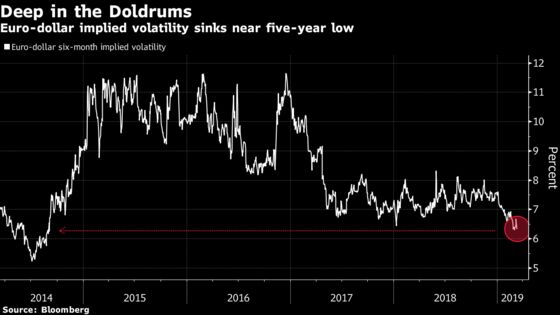

With volatility in the euro-dollar rate close to a five-year low, the time is ripe to put on a “cheap hedge,” said Maroutsos, who took over this month for Bill Gross as lead manager of what’s been renamed the Janus Henderson Absolute Return Income Opportunities Fund. He entered an options trade known as a straddle about three weeks ago, and tailored it to span a six-month stretch. He’s making a similar bet on Treasuries.

The currency position boils down to a belief that tumult is ahead for the euro, which sank last week to the cheapest level in 20 months. Europe’s darkening economic and political picture will weigh on the common currency and force the European Central Bank to introduce more stimulus, Maroutsos predicts. While he says the euro has scope to fall further, the nature of the straddle position means it will also gain if the euro dramatically strengthens.

“You spend a few basis points a month to implement this trade and if vol spikes, our portfolio benefits,” said Maroutsos, who’s Janus Henderson Group LP’s co-head of global bonds. “The ECB is likely going to have to engage in some sort of balance-sheet expansion, and all that’s going to do is point to a more volatile path for the euro.”

Maroutsos has taken over a fund that lost 4.9 percent in the past year, trailing most of its peers, according to data compiled by Bloomberg. With Maroutsos at the helm, it will focus on fixed-income assets, including government debt, corporate bonds and mortgages. A “team entity” will run the $915 million fund, Maroutsos told Bloomberg last week, rather than placing the spotlight on a single manager.

In line with his vision of the fund as a “risk reducer,” the volatility wager is meant to insulate the portfolio from violent currency gyrations. Last week drove home the trade’s value as a hedge: The euro touched as weak as $1.1177 on March 7, a level last seen in 2017, after the ECB lowered growth and inflation forecasts and dialed back policy-tightening expectations. The nosedive was enough to break the euro out of the 3.4-U.S. cent range it had held to this year through March 6, which had it on track for its quietest quarter ever.

Brexit headlines only add to Maroutsos’s conviction that larger swings in the euro are ahead. While the pound would be the natural choice to wager on the outcome of the U.K.’s divorce deal, buying euro volatility is a relatively inexpensive option, in his view.

“It’s obviously going to add to the volatility, and that’s ultimately the end-game,” he said. “We can play uncertainty in Europe and Brexit by buying the euro’s significantly cheaper vol.”

Most Volatile

The pound owns the highest Group-of-10 implied volatility across all tenors after the U.K. Parliament voted to avoid a no-deal split from the European Union on Wednesday, opening the door to delaying Brexit. Meanwhile, six-month implied volatility in the euro languished near its lowest levels since 2014.

Maroutsos is also betting on increased turbulence in the U.S. bond market. Benchmark 10-year Treasury yields posted their smallest monthly trading range since 1979 in February, swinging by just 11.6 basis points. Bank of America Corp.’s MOVE Index, a measure of anticipated swings in Treasuries, is closing in on its 2017 record low.

Against that backdrop, Maroutsos entered into a 1-year straddle on 10-year U.S. yields about two weeks ago as the Federal Reserve’s March meeting approaches and the global growth outlook continues to sour.

“If we’re wrong, we’ve only given up a small portion of our performance,” Maroutsos said. “But if Treasury or euro vol spikes, then it serves as a good hedge to the overall portfolio.”

--With assistance from John Gittelsohn and Molly Smith.

To contact the reporter on this story: Katherine Greifeld in New York at kgreifeld@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Randall Jensen

©2019 Bloomberg L.P.