(Bloomberg Opinion) -- It may be a cliché, but it’s true that the world’s awash in debt. In its quarterly update, the Institute of International Finance said on Tuesday that the world’s debt pile is hovering near a record at $244 trillion, which is more than three times the size of the global economy. Scary numbers, to be sure, but they didn’t stop one of the world’s most indebted and politically unstable countries from selling more than $11 billion of bonds without breaking a sweat.

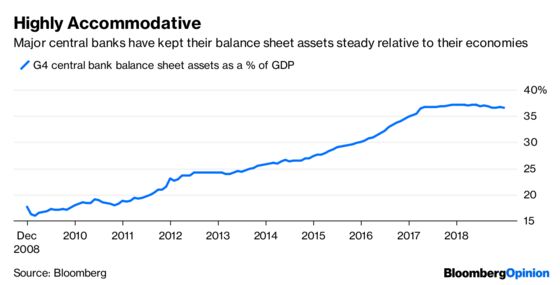

As proof, Italy was set to price 10 billion euros of notes to yield 18 basis points above benchmark rates, less than the 22 basis-point spread they were initially marketed, according to Bloomberg News. A spokesman for Italy’s debt agency confirmed that investors placed orders for 35.5 billion euros of the debt, and while such numbers should be viewed skeptically, the shrinking spread confirms there was high demand despite Italy wrestling with a debt-to-GDP ratio of more than 130 percent — the highest in the euro area after Greece, according to Bloomberg News. So while the world is awash in debt, it’s also awash in excess liquidity resulting from an almost decade’s worth of extraordinary monetary policies by top central banks. The collective balance-sheet assets of the Federal Reserve, European Central Bank, Bank of Japan and Bank of England, which grew steadily from less than 20 percent of their countries’ total GDP in 2011 to as high as 37.2 percent last February, has only eased to 36.6 percent despite the Fed’s efforts to shrink its assets over the last year or so, data compiled by Bloomberg show.

There may be a reckoning some day in the global debt market, but it’s not likely to be in 2019, especially with economists calling for a synchronized global slowdown and central bankers — especially those in the U.S. — sounding less hawkish. That should provide a favorable environment for fixed-income assets. For example, Morgan Stanley on Tuesday became the latest large investment firm to cut its forecast for U.S. Treasury yields. It now sees 10-year yields ending the year at 2.45 percent, compared with its prior call of 2.75 percent and the current market rate of about 2.72 percent.

WHERE THE RISK LIES

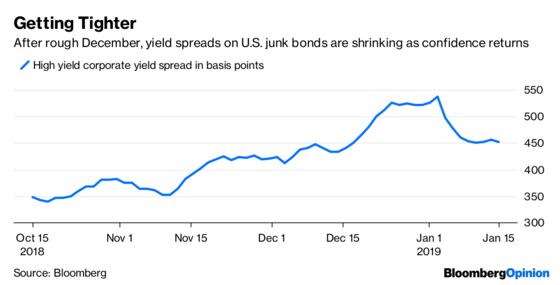

Not all debt is created equally, and any slowdown isn’t likely to benefit lower-quality corporate fixed-income assets, especially those with speculative-grade ratings. Even though the Bloomberg Barclays Global High Yield Index has had a strong start to the year, rallying 2.37 percent through Monday, erasing more than half its 4.06 percent loss in 2018, investors don’t seem sure of further gains. The latest monthly investor survey by Bank of America Merrill Lynch, released on Tuesday, showed that corporate indebtedness was the chief concern among fund managers for the first time since 2009. More specifically, a net 48 percent of fund managers think company balance sheets are overleveraged. There’s little question that creditworthiness has declined. The IIF debt report showed that global nonfinancial corporate debt rose to more than $72 trillion last year, putting it near a record high of 92 percent of GDP. Half the investors in the Bank of America Merrill Lynch survey said they preferred companies use their cash to improve balance sheets and just 13 percent favored a return of cash to shareholders. Nevertheless, credit markets enjoyed a strong showing Tuesday, with yield spreads shrinking for both investment-grade and junk bonds globally.

STERLING FAVORS THE BRAVE

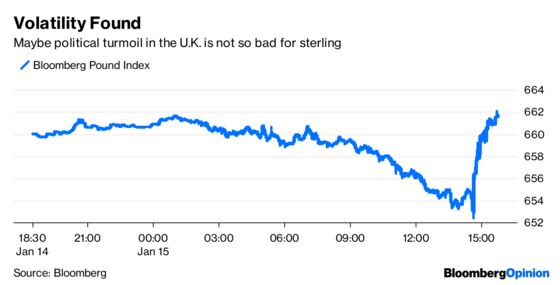

All eyes in the $5 trillion-a-day global foreign-exchange market were on the U.K., where lawmakers soundly defeated Prime Minister Theresa May’s plan to exit the European Union. May’s government will now face a no-confidence vote on Wednesday. And yet the Bloomberg Pound Index, which measures the currency against its major peers, rallied to its third straight gain after earlier falling as much as 1.03 percent in its biggest drop since Dec. 10. Clearly this was a case of sell on the rumor and buy on the news. Even so, the gauge has been stuck in a tight range the last two months, suggesting traders have probably priced in all the negative outcomes. In fact, sterling could even be poised for a bounce given how much it’s been beaten up over the past 18 months. “There’s a case for hiding way from all things U.K. and all things Brexit, but there’s still more upside for sterling than downside from here,” Kit Juckes, a global strategist at Societe Generale SA, wrote in note to clients on Tuesday. “Take away Brexit and 10 percent is the least that sterling would rally.” Juckes doesn’t seem to be the only one who feels like that: The median estimate of economists and strategists surveyed by Bloomberg is for the pound to end the year at $1.36, up from $1.2731 in Tuesday trading.

THE PAST OF LEAST RESISTANCE

To understand just how impressive this year’s global rebound in stocks has been, consider that the MSCI All-Country World Index has had just two down days, and each time the benchmark came back the next day to more than recoup those — including on Tuesday. That jibes with the Bank of America survey, which found that although 60 percent of fund managers said they expect global growth to weaken over the year — the worst outlook since 2008 — they’re primarily foreseeing secular stagnation in 2019, with just 14 percent predicting a global recession, according to Bloomberg News’s Ksenia Galouchko. That seems to prove that last month’s sell-off had gone way too far. The strategists at JPMorgan Chase & Co. figured that in the U.S. alone, stock prices were suggesting investors saw a greater than 60 percent chance of a recession this year. The survey was conducted from Jan. 4 through Jan. 10, with the global version polling 177 participants overseeing $494 billion in assets. “The good news was inflation expectations plunged, allowing investors to discount a new dovish Fed and a bull steepening of yield curve,” and it’s “no surprise that January fund manager survey shows de-risking is over,” the Bank of America strategists wrote in the report.

COMMODITIES START TO STIR

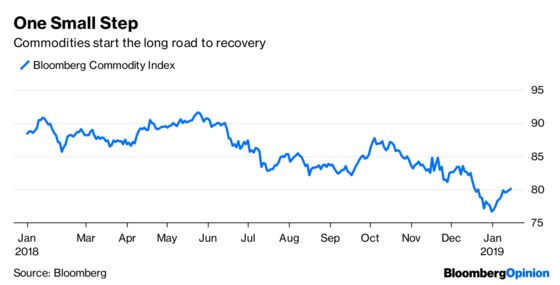

The Bloomberg Commodity Index of 27 raw materials has now rallied in nine of the past 10 trading days. That sounds impressive until you realize that the 4.42 percent rally still leaves the gauge down some 12.5 percent from last year’s high in May. The reason commodities came under pressure last year are well known: the U.S.-China trade war, a collapse in oil prices, concern that global economic growth was slowing. Some of the rebound this year seems to be an acknowledgment that perhaps the outlook isn’t as bad as thought. Yes, the global economy may slow, but many economists expect it to avoid a recession. And even if there is a recession, there’s a feeling it may come and go before anyone really notices — or at least shows up in the data on a real-time basis. “The question we should ask is: Is this a sag or heading toward a recession?” ECB President Mario Draghi told members of the European Parliament in Strasbourg in reference to the euro-area economy. “The answer we give is: No, it’s a slowdown, which is not headed toward a recession. But it could be longer than expected.” And if things really were so bad, gold probably wouldn't be suffering its worst start to a year since 2013.

TEA LEAVES

With the U.S. government shutdown having slowed the flow of economic data, the Fed’s “Beige Book” of economic conditions due to be released on Wednesday will be an important barometer of how the recent political turbulence is affecting the real economy, according to Bloomberg Economics. Those businesses contacted for the anecdote-based survey are likely to note further tightening in labor market conditions — the December jobs report was the best in the current cycle — and should provide some context around strengthening wage pressures, Bloomberg Economics noted in a research note. Comments on business confidence and capital spending plans could shed light on whether the third-quarter slowdown in investment spending was more noise than signal, it added. Also on Wednesday, the National Association of Home Builders is scheduled to release its monthly sentiment index. Despite the recent drop in mortgage rates, the median estimate of economists surveyed by Bloomberg is for a reading of 56, the same as in December, which was the lowest since mid-2015.

DON’T MISS

Stock-Pickers Don’t Know How or What to Sell: Barry Ritholtz

Italy Passes a $34 Billion Vote of Confidence: Marcus Ashworth

China’s Whiplashed Bulls Are Too Nervous to Run: Shuli Ren

Kuroda’s Exuberance in Nagoya Was So 2018: Daniel Moss

Puerto Rico Treads Trump Path to Wipe Out Debt: Brian Chappatta

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.