It's the Iranian Oil Guessing Game. And the Bears Are Winning

It's the Iranian Oil Guessing Game. And the Bears Are Winning

(Bloomberg) -- Oil skeptics have been proved right in downplaying sanctions against Iran.

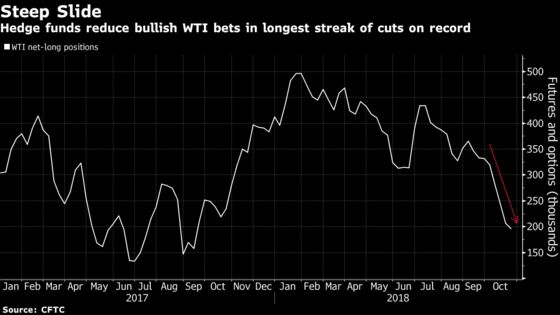

Hedge funds reduced bets on rising West Texas Intermediate crude prices for an eighth straight week, the longest streak of reductions on record, even as curbs on Iranian oil are set to kick in. After sanction fears propelled the benchmark to four-year highs early last month, futures have since plunged almost 20 percent as signs mount that the impact might not be so bad.

“The teeth around these sanctions aren’t as sharp as what may have been telegraphed by the administration going into September and October,” said Chris Kettenmann, chief energy strategist at Macro Risk Advisors LLC. “The other piece of the story is the Saudis would move to fill these volumes into the fourth quarter.”

While it’s still a guessing game how much Iranian oil will be removed from the market, U.S. Secretary of State Michael Pompeo said on Friday that the U.S. will grant eight temporary waivers for countries to keep importing crude from the Middle Eastern nation. And OPEC also is signaling it’s willing to fill any supply gaps--the group’s output jumped to the highest since 2016 in October.

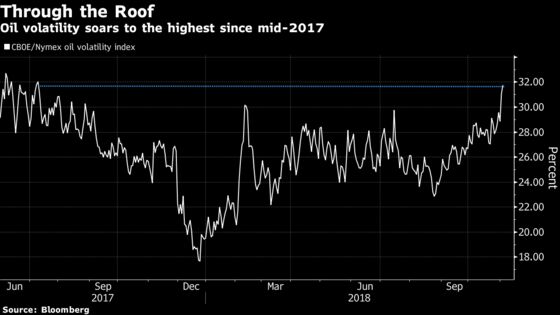

Meanwhile, oil market volatility has spiked to levels last seen in more than a year as investors try to estimate the outcome of the sanctions coming to effect this week.

“You are seeing a real fundamental shift in the market from concern about a shortfall to now real concern about maybe there is too much supply in the market,” Andrew Lebow, senior partner at Commodity Research Group, said Friday. “That was hammered home this week.”

Hedge funds’ net-long position -- the difference between bets on higher prices and wagers on a drop -- in WTI crude slid 5 percent to 196,196 futures and options in the week ended Oct. 30, the lowest level since September 2017, according to the U.S. Commodity Futures Trading Commission. Longs fell 3.7 percent, while shorts edged up to the highest since late last year. Total positioning on WTI is at the lowest since 2014.

Demand growth fears stemming from a U.S.-China trade war have also led investors to shun riskier assets, such as oil.

Even if hedge funds won this round of bets, it’s hard to tell how much Iranian crude production will clock in over the coming months. Output from the nation has dropped a little less than 500,000 barrels a day since the end of February. Natixis analysts say once equity markets stabilize and oil markets digest the loss of Iranian exports, Brent crude should rise toward $81 a barrel in the fourth quarter.

Output likely won’t “drop all that much further,” said Thomas Finlon, director of Energy Analytics Group in Wellington, Florida. “It’s not like the world is flush with oil. It’s maybe a little closer to a balance. We’re a million miles from a glut.”

| OTHER POSITIONS: |

To contact the reporter on this story: Jessica Summers in New York at jsummers24@bloomberg.net

To contact the editors responsible for this story: David Marino at dmarino4@bloomberg.net, Carlos Caminada, Catherine Traywick

©2018 Bloomberg L.P.