Investors Want Latin America Debt. Companies Aren't Selling

Investors Want Latin America Debt. Companies Aren't Selling

(Bloomberg) -- Global investors are flush with cash and ready to do deals with Latin America’s corporate issuers. Trouble is, there’s not much debt to buy.

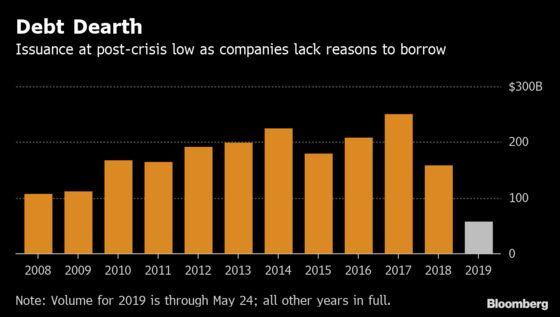

It’s shaping up to be a meager year for issuance in the region, with Itau Unibanco Holding SA forecasting $65 billion to $75 billion of new dollar debt sales. That would be the lowest amount since at least the financial crisis 10 years ago as a lackluster economy cancels out a more benign interest rate environment.

“There’s plenty of funds chasing very few deals,” Baruc Saez, Itau’s head of Latin America investment banking, said in an interview. “The very dovish policy and outlook on rates is very constructive for emerging markets and Latin America in particular.”

Latin America’s economic output is expected to grow just 1.4% this year, held back by slowdowns in Brazil and Mexico, a never ending crisis in Argentina and Venezuela’s collapse. As a result, businesses are reluctant to take on new debt, sticking mostly to the refinancing of upcoming maturities. And more companies are selling debt in local markets, which are brimming with liquidity.

That’s the story this year in Latin America’s largest economy, according to Eduardo Freitas, Citigroup Inc.’s head of debt capital markets for Brazil.

“When we knock on the door of the companies, the executives tell us: ‘I love these yields, these prices are great. But for what will I raise money?’” Freitas said in an interview in Sao Paulo. “With the economy growing so slowly, the companies are not making big investments now. They are waiting.”

In the region’s second-largest economy, Mexican companies are selling less debt as they seek to cut leverage levels amid a cloudy outlook under President Andres Manuel Lopez Obrador.

Petroleos Mexicanos, Latin American’s biggest issuer, may sit out 2019 entirely after selling around $10 billion of debt last year. Saddled with $106.5 billion in borrowings, the Mexican state oil company is focused on bringing down leverage, Pemex’s Chief Executive Octavio Romero has said.

In Argentina, the country’s most prolific issuer has sat on the sideline for the last year as the sky-high sovereign yield made selling bonds prohibitively costly. Gas and oil producer YPF SA has reduced its ratio of net debt to a measure of earnings to around 2.5 times, down about 60% since 2016. Other oil companies, such as Colombia’s Ecopetrol SA, have used cash to pay off dollar debt.

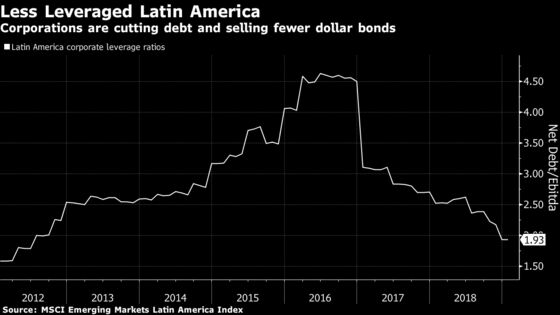

So corporate debt levels have fallen off sharply. At the end of last year, the average net debt-to-Ebitda ratio for the region stood at 1.93, the lowest since 2012, according to the MSCI Emerging Markets Latin America Index.

“There’s just not a ton of mergers and acquisitions or capital expenditure activity to drive the need for debt,” said Jennifer Gorgoll, a portfolio manager at Neuberger Berman Group, which has $323 billion in assets under management. “This year you’re going to see more smaller deals in the $300 to $500 million range.”

In one of the few major M&A deals so far this year, Brazil’s Natura Cosmeticos SA has had a long line of banks to choose from to finance its acquisition of rival Avon Products Inc., demonstrating how much cash is available in the market. In the end, Banco Bradesco SA, Citigroup and Itau were picked to provide $1.6 billion in financing for the deal valued at about $2 billion.

The dearth of sales is creating space for riskier companies to tap markets they may have been shut out of last year. In January, TermoCandelaria Power Ltd., a Colombia-based power plant owner, upped the size of its junk bond sale to $410 million. International Airport Finance, which operates the airport in Ecuador’s capital, Quito, paid a premium -- the coupon rate was 12% -- but was able to place $400 million in notes.

There was little appetite for those types of deals just a year ago, said Mauricio Fernandez, Itau’s vice president for fixed income.

“The new year was a page turner. Suddenly you have investors wanting to put money to work,” he said. “That creates opportunities for these guys.”

Even lower-rated credits are willing to test the market. Avianca Holdings said it plans to go ahead with a sale to refinance $550 million in notes due next year despite a month of upheaval for the region’s second-largest airline.

Similarly, Mexico’s Grupo Televisa was able to complete a deal for $750 million of bonds maturing in 30 years. The company sold the debt despite a rough start to the year that saw its stock tank over 25% after news that it would not spin off core assets as previously planned.

“The international market is there, ready to offer cash,” Citigroup’s Freitas said. “However, in order to see more debt sales and huger sizes, we will need to see a return to growth in the world.”

To contact the reporters on this story: Ezra Fieser in Bogota at efieser@bloomberg.net;Pablo Gonzalez in Buenos Aires at pgonzalez49@bloomberg.net;Justin Villamil in Mexico City at jvillamil18@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, ;Julia Leite at jleite3@bloomberg.net, Robert Jameson

©2019 Bloomberg L.P.