Investors Lament Anti-Spinoff Sentiment Spurred by 2019’s Flops

Investors Lament Anti-Spinoff Sentiment Spurred by 2019’s Flops

(Bloomberg) -- The poor performance of recent spinoffs is creating an overly negative sentiment around any such deals, fund managers say.

Spinoffs have missed out on the broader market rally during the second half of 2019. But The Edge Consulting Group, a research firm that specializes in spinoffs, said there are still opportunities to go long. On Thursday, investors were pitched situations ranging from U.S. retail to European media stocks at an event hosted by the research firm as a benefit for The Alzheimer’s Association.

“The perception in the market that spinoffs aren’t working is creating opportunities,” The Edge deals analyst Jonathan Morgan said at the New York event. “While data is not the end-all, be-all in spinoffs, we can use this as a tool to identify opportunities.”

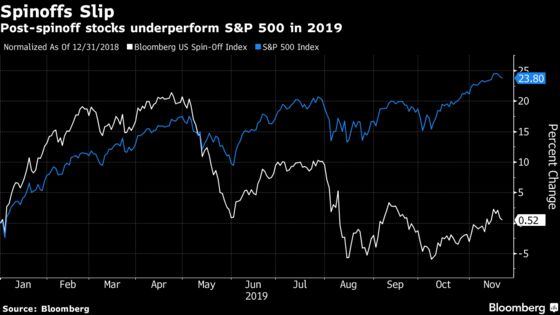

The Bloomberg US Spin-Off Index, which tracks the performance of recent spinoffs, has risen by less than 1% in 2019 while the S&P 500 rallied by 24%.

Fund managers at the conference were also implored to look more closely at Bed Bath and Beyond Inc. by Jonathan Duskin, chief executive officer of activist firm Macellum Capital Management. The stock is currently lower than it was when Macellum launched its activist campaign in March, despite significant changes including a new CEO, a reassembled board, the hiring of Goldman Sachs to sell non-core assets and another firm to sell real estate.

“We’ve already done all the hard work,” he told the room of investors. “Rarely has most of the work been done and the stock hasn’t reflected it.” Duskin says Bed Bath & Beyond has been victim of the broadly negative sentiment toward the space.

Turning to Europe

Sweden’s Modern Times Group MTG AB is worth 60% to 80% more than its current public valuation, Evermore Global Advisors CEO David Marcus said in a separate presentation at the conference. Evermore, which owns about 6% of the gaming and e-sports firm, said that the value of the gaming business plus the company’s net cash is greater than its market cap -- making the e-sports segment free for buyers.

“Once they finish their strategic review, you’ll see asset sales. They don’t need the cash, so it will come back to shareholders either via a monster buyback or a cash dividend.”

Marcus said that companies like MTG fall behind their deserved valuation because investors are shying away from Europe amid trade, credit and geopolitical fears. But private equity and activist investors are moving into Europe more than ever before.

“All the problems that Europe is facing is precisely why you need to drop everything and start doing your homework,” he said. “Cost cuts are actually going to the bottom line, and they weren’t in the past.”

More Separations Ahead

The Edge expects about 20 more U.S. spinoffs over the next year or two despite recent weakness. Its data show that the first year after a spinoff provides weaker returns than subsequent years, creating plenty of chances to take positions at favorable valuations.

“I’ve heard people say that spinoffs don’t work,” The Edge Group CEO Jim Osman said. “What does that mean? This isn’t a golden goose that you can go get and make money. It’s a good ground for looking. What we’ve done over the last 12 years is give an analytical advantage to give a handful of ideas per year.”

To contact the reporter on this story: Drew Singer in New York at dsinger28@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Catherine Larkin, Richard Richtmyer

©2019 Bloomberg L.P.