Inflation Believers Win Big and Defy the Pandemic Market Panic

Inflation Believers Win Big and Defy the Pandemic Market Panic

(Bloomberg) -- Mark Nash snapped up inflation-protected bonds in March, when markets were shaken by fears of recession and deflation that left the securities dirt cheap. Now he and other contrarians are reaping the benefits of record gains in the bonds.

Inflation-linked bonds beat nominal peers by the most in at least 22 years last quarter, despite the lack of an acceleration in consumer prices. The performance is owed mainly to investors seeking protection from price pressures that may emerge from stimulus efforts and a return to economic growth. While not all fund managers agree, Nash, head of fixed income at Merian Global Investors, thinks the market will gain further as governments and central banks prop up economies and prevent deflation.

“Buying inflation protection, which was incredibly cheap then, turned out to be a brilliant idea,” said Nash, whose Strategic Absolute Return Bond Fund has beaten 95% of its peers with a year-to-date return of almost 6%.

Inflation-protection trades paid off as the worst-case scenario of deflation was averted. Still, an acceleration in consumer-price increases is widely considered only a remote possibility. Inflation is not a concern in the current economic crisis, Federal Reserve Bank of San Francisco President Mary Daly and Richmond Fed President Thomas Barkin both said on Tuesday.

The U.S. 10-year breakeven rate, a gauge of market inflation expectation derived from the yield gap between linkers and nominal bonds, has recovered from its 11-year low in March. Yet, at 1.41%, it’s still well below its five-year average and the Fed’s 2% inflation target.

Prior periods of economic stimulus efforts this century were met with predictions of faster inflation that proved to be off the mark. Holders of inflation-linked bonds, whose face value is adjusted to account for the rate of inflation, likely would take losses if that’s the case this time.

Not Convinced

For investors like Elaine Stokes at Loomis Sayles & Co., the prospects for an inflationary rebound are lacking. She’s not detecting any pressure other than what the market has already gleaned from the trough in commodity prices. The labor-market damage from the pandemic is still unfolding, and the lockdown has only entrenched disinflationary trends such as increased power in the hands of consumers, less brick-and-mortar retail, and more renting versus owning.

“The conviction level to be putting a lot of money in inflation-linked securities, we’re struggling with that,” the money manager said. “We’ve seen a lot of money come into the economy back in ‘08-’09 -- it didn’t turn around and give us inflation.”

Praveen Korapaty, chief interest rate strategist at Goldman Sachs, suggested investors who gained from inflation-linked bonds should “take some chips off the table” over the next couple of months amid a resurgence of virus infections in the U.S.

“On a tactical basis, perhaps the inflation outperformance takes a bit of a breather until we get more clarity on this,” Korapaty said in an interview. “It looks like consumers and businesses are freaking out again, seeing the surge in cases, so you might see some pullback” in the reflation trend, he said, though he expects the strategy will hold longer term.

Supply Chains, Shortages

Merian’s Nash, whose fund first bought 10-year U.S. Treasury Inflation Protected Securities and then went “long inflation across the board,” is not alone in betting that consumer prices will pick up in the future.

The main argument for higher inflation is that an environment of ultra-loose monetary policy and fiscal spending, commodity shortages, disrupted supply chains and de-globalization is fertile ground for higher consumer prices.

BlackRock, which has argued that a supply-chain disruption could push up prices, recently increased its allocations to inflation-linked bonds on a strategic basis while cutting back on nominal bonds. Goldman Sachs favors short-dated linkers. BNP Paribas Asset Management also sees more scope for gains in assets that thrive as consumer-price gains accelerate.

This view is buttressed by hints of a faster-than-expected economic turnaround. JPMorgan Chase & Co., whose global composite PMI index has rebounded from 26.2 to 47.7 over the last two months, cut its probability for global recession to 10% from 55% three months ago. Money supply and loan growth surged in the U.S. and Europe thanks to central banks offering attractive terms and governments providing guarantees.

Inflation Solution

And with governments borrowing at a record pace to keep their economies afloat through the pandemic, monetary authorities could face pressure to keep interest rates low. Such action could serve the dual purpose of containing the cost of servicing massive amounts of sovereign debt, while at the same time allowing inflation to erode it.

“Debt rollover will become harder when rates rise,” said BlackRock strategists including Elga Bartsch, head of macro research. “It may eventually have to be dealt with through austerity, default or inflation. Inflation could be seen as the most politically palatable solution.”

The flow of money into linkers is clear. Inflation-protected bond funds globally broke records with $2.5 billion of inflows in the week to June 24, according to EPFR.

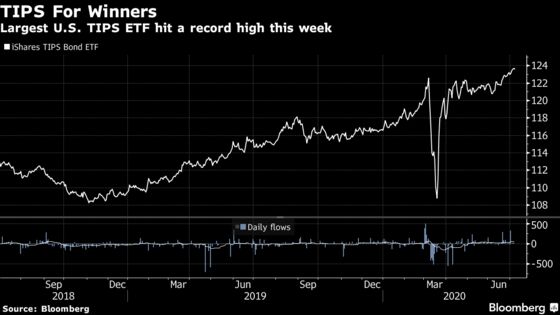

In exchange-traded funds, Schwab’s TIPS flagship swung from the largest ever outflow to its largest inflow this month -- most likely rebalancing of model portfolios, but still a vote of confidence in recovering price pressures. And this week iShares’s TIPS Bond ETF, the asset class’s largest, hit a record high after its longest advance on record. That said, these six straight quarters of gains have also seen a pickup in withdrawals.

The coronavirus is a wild card that complicates decisions around any investments these days, and inflation bonds are no exception.

A second wave of the pandemic won’t necessarily derail the recovery, according to Colin Harte, a portfolio manager at BNP Paribas Asset Management. Experience may help governments and companies manage the situation better. He is looking to add to his long commodity positions as a “sea change” in government policy responses to crises is likely to translate into inflation in the longer term.

“We are in that type of world now where there is a lot of building and reconstruction in the economy after a serious shock, similar to that after the Second World War,” said Harte. “All of that will tend to prove more inflationary than we’ve known in the past 20 plus years.”

©2020 Bloomberg L.P.