Were Those Earnings Really That Good?

Trouble Spots Lurk Beneath Earnings Optimism

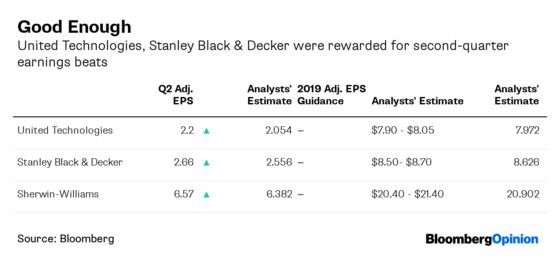

(Bloomberg Opinion) -- Good news comes with baggage for industrial companies this earnings season. United Technologies Corp., Stanley Black & Decker Inc. and Sherwin-Williams Co. all reported better-than-expected second-quarter earnings per share on Tuesday, but each company also gave investors new data points to worry about.

For United Technologies, it was the fact that its aerospace businesses seem to be the only thing driving its improved outlook for sales and earnings in 2019. New equipment orders dropped 12% at Carrier in the period and 6% at the Otis elevator division, echoing reports of damped enthusiasm from industrial distributor Fastenal Co. and indications of an overall stagnation in new U.S. factory orders in June from the Institute for Supply Management. Stanley and Sherwin-Williams both left their full-year adjusted profit guidance unchanged despite notable beats in the second quarter, suggesting a cautious outlook on the rest of the year. Indeed, Stanley modestly reduced its expectation for volume growth amid a weaker outlook for industrial and emerging markets. Sherwin-Williams now expects overall revenue to increase only as much as 4% in 2019, down from an April projection of as much as 7%. Both companies think they can make up ground via price increases, but such sales weakness is troubling because Stanley and Sherwin-Williams can also be good proxies for the housing market and consumer demand.

Despite the mixed results, stocks of all three companies rose Tuesday. Sherwin-Williams hit a new high and was on track for its biggest gain since 2009, while Stanley saw its biggest intraday gain since December. This is partly a reflection of lowered expectations. Industrial companies within the S&P 500 command a price-earnings ratio of about 17.5, a 10% discount to the broader benchmark’s valuation of 19.5 times profit. The average discount over the past five years is closer to 4%. Stanley had been down nearly 2% in the year leading up to Tuesday’s earnings report, owing in part to margin pressure it flagged earlier in the year. United Technologies has missed out on a nearly 4% gain in the S&P 500 after announcing a merger with Raytheon Co. that’s roused pushback from activist investors Bill Ackman and Dan Loeb.

Generally speaking, though, investors appear to be choosing to prioritize the good headlines over the bad. Pentair Plc rose as much as 5.1% on Tuesday, despite relying mostly on tax benefits to beat analysts' second-quarter earnings estimates and cutting its organic growth guidance for the year. The International Monetary Fund further reduced its global growth outlook on Tuesday, saying a projected pickup from 2019’s pace in 2020 is “precarious,” with the principal risk factors being the U.S.’s various trade battles and Brexit. But for now, industrial companies are drawing on every means they have to keep the boom going, whether that’s relying on the still-robust aerospace market, pushing through price increases and cost cuts, or simply wagering a Federal Reserve interest-rate cut will boost investment.

The thing about price increases is they get much trickier to pass along if demand starts to wobble. Stanley is also feeling the pain from the U.S.-China trade war. It now expects a $390 million hit to 2019 earnings from tariffs, currency swings and rising commodity prices, up from $340 million previously. Come 2020, United Technologies’ Carrier and Otis units will be spun off as independent companies, freeing the company from any future underperformance. Currency swings wiped out the modest organic revenue gain at Carrier in the second quarter, leaving it with a 1% decline in overall sales for the first six months of the year, and United Technologies lowered its full-year sales and profit outlook for the division. The flip side of United Technologies’ breakup is that it will be more exposed to an eventual downturn in aerospace markets without those two divisions, something it hopes to offset by expanding its defense business through the Raytheon deal.

This willingness to look past trouble spots will be put to the test later this week when Caterpillar Inc. and 3M Co. report.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.