Indian Bank That's Risen 1,500% Bets on a Merger to Extend Gains

Indian Bank That’s Risen 1,500% Bets on a Merger to Extend Gains

(Bloomberg) -- IndusInd Bank Ltd., India’s best performing lender in the past decade, is counting on its acquisition of a microfinance firm to help it improve profitability, while shrugging off risks from the country’s spreading shadow bank crisis.

IndusInd’s purchase of Bharat Financial Inclusion Ltd. will help it to “move the needle” on profitability parameters including return on assets and lending margins, Chief Executive Officer Romesh Sobti said. Acquiring the nation’s largest micro financier gives the bank presence in more than 115,000 Indian villages that will increase its cross-sell, lending and low-cost deposit mobilization efforts, Sobti said, in an interview in his office.

To read more about how IndusInd will benefit from Bharat Financial merger

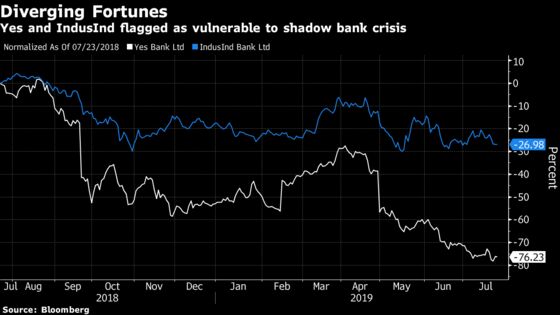

Mumbai-based IndusInd, which has risen 1,500% since Sobti became CEO in 2008, lost some of its sheen after analysts including those at Credit Suisse Group AG and UBS Group AG flagged the lender’s exposure to beleaguered Indian shadow banks including Dewan Housing Finance Ltd. However, higher capital buffers and lower bad loans helped the bank sidestep the fate of rival Yes Bank Ltd., which had lent to the non-banks, and saw its market capitalization halve.

“IndusInd’s exposures are way lower than what is projected in those reports and is backed by adequate collateral,” Sobti said. “We are not expecting any spike in bad loans and are currently focusing on using the doorway offered to rural India through Bharat Financial.”

IndusInd has been more selective in lending to non-bank finance companies off late. The bank’s net bad loan ratio stands at about 1.2% compared with 2.9% at Yes Bank. IndusInd’s return on assets rose to 2.1% in June from 1.9% in the year ago period, filings show.

Still, there’s another risk looming for the bank, according to Morgan Stanley analysts -- Sobti’s retirement in March. The CEO who had quit ABN Amro Bank NV’s local unit to take the top job at IndusInd in February 2008, is credited with the turnaround that led to the surge in it’s shares, making it the best performer on the 10 member Bankex Index. The index climbed 200% in the same period.

“There is no need for concern as the board has been applying its mind to this over last four years,” Sobti said. “By end of 2019 my successor will be in place, and there won’t be any disruption.”

Sobti also shared his views on stressed exposures flagged by analysts and the bank’s lower provision-coverage ratio. Comments in the following Q&A have been edited and condensed:

Stress disclosed by IndusInd and flagged by analysts differ.

Analysts are calculating the stressed exposure based on regulatory filings done by the borrowers. There are several ways in which you can go wrong while reading those numbers as it doesn’t reflect repayments made on the loans. Also, there is a likelihood of misreads as some filings are duplicated. Hence the divergence.

IndusInd’s provision-coverage ratio is lower than peers.

The ratio dropped to 43% after we provided for loans to IL&FS group in the March quarter. We are not expecting any similar large slippages from here on and are sticking to a credit cost guidance of 60 basis points for the year. The provision-coverage ratio will improve in the coming quarters.

To contact the reporters on this story: Suvashree Ghosh in Mumbai at sghosh186@bloomberg.net;Anto Antony in Mumbai at aantony1@bloomberg.net

To contact the editors responsible for this story: Marcus Wright at mwright115@bloomberg.net, Arijit Ghosh, Abhay Singh

©2019 Bloomberg L.P.