Massive India Borrowing Loads Pressure on RBI to Tame Yields

Investor focus turns to key central bank meeting on Friday. Bonds selloff Monday as near-record debt plan surprises market.

(Bloomberg) -- India’s central bank is under pressure to step in to keep yields in check after the government surprised bond markets with a bigger-than-expected borrowing plan.

That puts the burden on Governor Shaktikanta Das to calm bond traders when he meets to decide policy on Friday. He’s already had to assuage them that a recent measure to mop up excess liquidity isn’t a step toward changing the RBI’s accommodative policy and the central bank has rejected bids at two auctions of benchmark debt after investors sought higher yields.

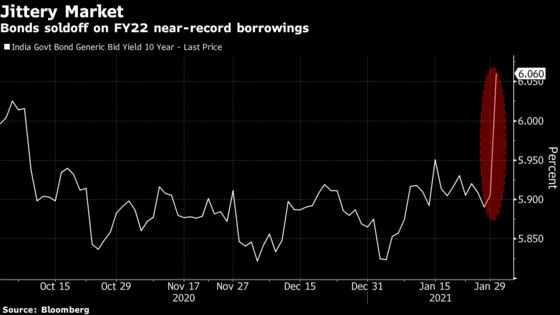

India will borrow a gross 12 trillion rupees ($164 billion) via bonds in the fiscal year beginning April, Finance Minister Nirmala Sitharaman said Monday, higher than the 10.6 trillion rupees estimated in a Bloomberg survey. Bonds sold off on the announcement, with the benchmark 10-year yield extending rise to 6.12% on Tuesday, its highest since Aug. 31.

“The higher borrowing is a concern for the market,” said Anoop Verma, senior vice president at DCB Bank Ltd. in Mumbai. “It will be difficult for the RBI to anchor yields around 6%.”

In contrast, the reaction to the budget from India’s equity market was favorable. Stocks extended gains for a second day as investors cheered the absence of new taxes as well as the government’s plans to spend close to $500 billion over the next fiscal year.

Yet those with an eye on bond markets like Verma want the RBI to outline when and how much debt it will buy. The central bank has been using so-called Open Market Operations off-and-on, as well as discreet secondary market purchases and Operation Twists to keep yields in check.

The battle between bond traders and the central bank played out for most of last year, with the monetary authority practicing what many called implicit yield control -- trying to keep the benchmark 10-year yield around the 6% mark.

However, the act became harder this year as the RBI began unwinding some emergency pandemic measures.

Support Needed

“The big shocker, besides higher borrowings, was the government postponing its fiscal consolidation for the future,” said Arvind Chari, chief investment officer at Quantum Advisors Pvt Ltd. in Mumbai.

Prime Minister Narendra Modi’s government expects fiscal deficit to reach 4.5% of GDP by fiscal year ending 2026, after projecting it at 3.1% by March 2023 in its previous budget. The administration also raised its borrowing plan for the third time in the current fiscal year on Monday. It will now raise 800 billion rupees in addition to its record 13.1 trillion rupees target.

Bond yields stayed elevated even after Economic Affairs Secretary Tarun Bajaj said that the government may borrow less than 12 trillion rupees estimated in the next fiscal year and that 55%-60% of the total borrowing may be completed in the first half. The government and RBI are on the same page on conducting smooth borrowing, he said.

“The market will have to live with the higher borrowing,” said Soumyajit Niyogi, associate director at India Ratings & Research in Mumbai. “Continuous support of the RBI will be required.”

©2021 Bloomberg L.P.