India Supercharged Its Economy 30 Years Ago. Covid Unraveled It in Months

Liberalisation fuelled one of the biggest wealth creations in history. India lost many of those advances during the pandemic.

(Bloomberg) -- Thirty years ago, on a summer evening in late July, India liberalized its Soviet-style economy in a transformation that eventually pulled about 300 million out of poverty, fueling one of the biggest wealth creations in history.

Then came the world’s fastest coronavirus surge which left overflowing hospitals turning away the dying and crematorium smoke darkening city skies.

Years, and perhaps decades, of progress have been unwound in months, as many Indians who had clawed their way out of poverty face grim job prospects and carry heavy debt loads wracked up to get themselves and loved ones through the pandemic. The devastation has highlighted just how much poor health care and infrastructure — often neglected in the boom after liberalization — are holding back the nation and its people.

More than 200 million have gone back to earning less than minimum wage, or $5, a day, the Bangalore-based Azim Premji University calculates. The middle class, the engine of the consumer economy, shrank by 32 million in 2020, according to the Pew Research Institute. That means India will be regressing on vital fronts just as its global importance is growing.

This decade, India is expected to become the world’s most populated nation, taking that mantle from China, which for years drove global growth. But the Indian economy is grappling with big threats even as it becomes home to the kind of young, working-age population that drove lengthy booms in other nations.

“We’re talking about a decade of lost opportunities and setback,” said Arvind Subramanian, a fellow at Brown University and a former chief economic advisor to Prime Minister Narendra Modi’s administration. “Unless there are some big reforms and fundamental changes in the way economic policy is done, you’re not going to be anywhere close to what we saw in the boom years. A lot needs to happen in order to get back to the 7%, 8% growth that we desperately need.”

Even before the pandemic, cracks had begun to emerge. Modi came to power in 2014 amid voter frustration over scandals and policy paralysis that had contributed to bad loans at banks and threatened to derail Indian growth. Yet, the economy has faced other hurdles in recent years including Modi’s 2016 cash ban, which roiled the informal sector, and a hurriedly implemented new tax system.

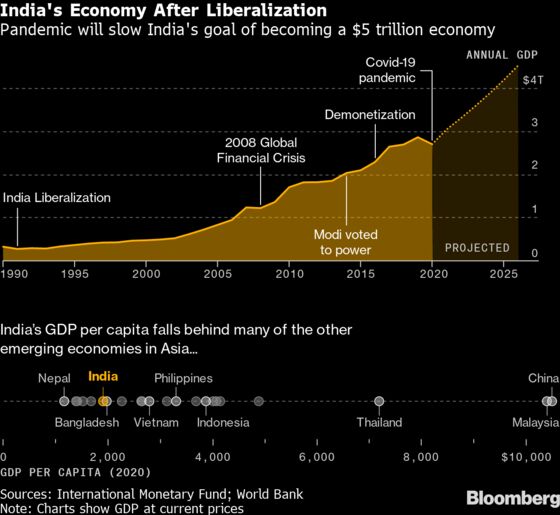

Modi had pledged to turn India into a $5 trillion economy by 2025, but the pandemic is set to push that back by years. The International Monetary Fund expects India to grow 6.9% in the next fiscal year that starts in April 2022, lower than the more than 8% needed long term to reach Modi’s ambitious target and create jobs for the millions entering the work force.

Jim O’Neill, chairman of Chatham House in London — who coined the term BRICs to describe the emerging markets of Brazil, Russia, India and China while serving as a top Goldman Sachs Group Inc. economist — is these days cautious on India, largely because the government hasn’t made many of the long-term structural changes he believes are needed for it to reach its full potential.

When still at Goldman Sachs, O’Neill says he presented a paper to Modi in 2013, before he became prime minister, recommending 10 things that would allow the Indian economy to be 40 times larger by 2050. The list included making substantial improvements to areas like infrastructure, education, introducing better public-private partnerships in areas like healthcare, further liberalizing financial markets and working on environmental issues. Modi hasn’t fully pursued these ideas, O’Neill said.

“India’s got these fantastic demographics, which should have given it the potential to be rising a lot more strongly, possibly at the same kind of double digit rates China enjoyed for a long time,” O’Neill said. Yet “the Indian system seems to quite often smother itself, as we’ve seen sadly a few times during the Covid pandemic,” he said.

A government spokesperson didn’t respond to request for comment, but the Modi administration has in recent weeks acknowledged the need for longer term changes. “If we are looking at getting growth — of 8%-10% — back on a sustainable path, we have to think about not just a current revival,” Sanjeev Sanyal, the government’s principal economic adviser, said at the India Global Forum on June 30. Structural changes are needed and to that end the government is constantly opening up new sectors of the economy, he said.

Once the fastest-growing major economy, India saw its biggest ever contraction last year — shrinking more than 7% — after a stringent nationwide lockdown. Just when the economy started showing some momentum, another wave of infections hit the nation. This year, the central bank expects India to grow at 9.5%, sharply lower than the double-digit rebound many had earlier expected. That estimate is heavily boosted by the comparison with the sharp contraction of the previous year, and many economists expect it could be pared even further.

Foreign direct investment surged 19% last year, but even that remains lower as a percentage of GDP compared with countries like Singapore and Vietnam. And a big portion of the foreign investment went to billionaire Mukesh Ambani’s digital platforms.

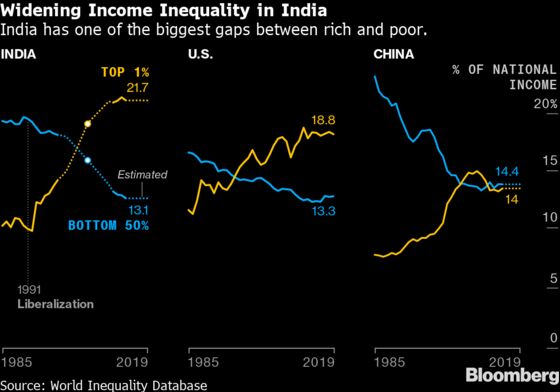

Some experts, including former central bank head Duvvuri Subbarao, have warned of a K-shaped recovery for India, where the rich get richer and poor get poorer. “Growing inequalities are not just a moral issue,” said Subbarao. “They can erode consumption and hurt our long-term growth prospects.”

Two of the richest men in Asia — Ambani and ports magnate Gautam Adani — are Indians, and their net worth has surged as stocks rallied on the back of cheap liquidity worldwide and tax cuts for companies even as economic growth slumped. Meanwhile, overall Indian wealth — or the value of financial and real assets owned by households minus debts — fell by $594 billion, or 4.4%, in 2020, according to Credit Suisse Group AG.

Thirty years ago, India was forced to remake its economy. A mammoth trade deficit and plunging foreign exchange reserves necessitated a loan from the International Monetary Fund. On July 24, 1991, then finance minister, Manmohan Singh, announced major steps to cut tariffs and encourage trade, essentially opening up the economy to the outside world.

In the boom that followed liberalization, growth crossed 8%. Technology giants like Infosys were born and start-ups worth billions are now mushrooming in Bangalore. A new middle class emerged that watched Netflix and shopped online on Amazon. In the south, the Wistron factory won special economic benefits to assemble Apple iPhones. India became the world’s biggest supplier of generic medicines and the Serum Institute of India became the world’s biggest vaccine maker. An Indian exchange now handles the world’s highest number of derivatives contracts.

Yet there were signs that India wasn’t hitting its full potential. Average GDP growth of 6.2% over 30 years has been lower than China’s 9.2% and even lagged Vietnam’s 6.7%. For years, Indians have been living shorter lives and are now earning less on average than people in smaller nations like Bangladesh.

Vast inequities developed. Researchers have found wealthier people in urban areas and from upper castes were taller in India, a sign of development favoring groups that were already advantaged. The percentage of women joining the workforce fell from 30.3% in 1991 to about 21% in 2019, according to data from the International Labor Organization. India’s government spent less than 2% of GDP on healthcare before the pandemic.

“Had the healthcare system not been so neglected for so long, India would have been prepared to face the Covid-19 crisis,” said Jean Dreze, the Belgian-born Indian economist and a lecturer at Delhi University. “Had India built a more robust social security system, the humanitarian toll of the crisis would not have been so catastrophic.”

Unlike the old guard in 1991, Modi has turned the economy more inward, focusing on self-reliance and homegrown companies. Despite championing free trade in global forums, he’s raised tariffs on goods including electronics and medical equipment, partly reflecting global trends.

Some of those decisions came back to haunt India when citizens struggled to import life-saving products like oxygen concentrators during the pandemic. Top scientists wrote to Modi, asking him to reverse protectionist duties imposed on key items needed to study the coronavirus and its variants including the delta one, which now threatens the globe.

After pledging to contribute to global vaccine programs, the Modi government slowed exports of Covid-19 shots, derailing the inoculation program of a World Health Organization-backed initiative.

“India’s ambition of being seen as a major player on the world stage has taken a substantial hit as the pandemic has laid bare the weaknesses in the capacity and competence of its government,” said Eswar Prasad, professor of trade policy at Cornell University.

The key question for global investors now is whether India will get old before Indians get rich. Netflix is counting on India for its next 100 million customers. Bezos is pouring billions of dollars — and even braving Indian courts — to battle India’s richest man Ambani for a slice of the only open retail market with more than a billion people.

“The pandemic has set us back hugely, and we were already on a growth downswing when it happened,” said Indira Rajaraman, an economist and a former member of the Reserve Bank of India’s board. “Going forward it all depends on how cleverly we design the way we come out of these doldrums.”

©2021 Bloomberg L.P.